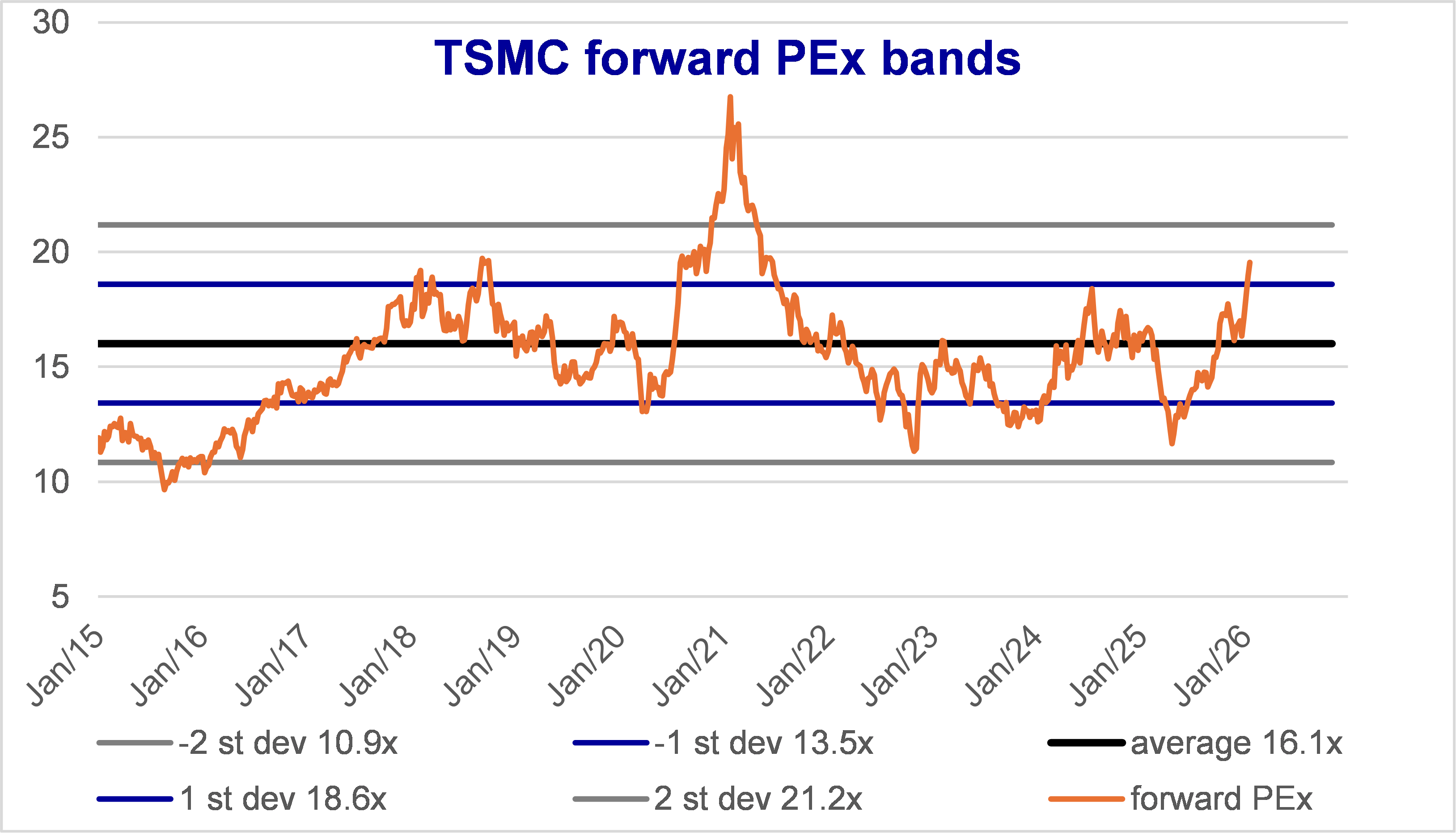

TSMC: consensus revised up, but modestly. Stock at reasonable valuations

Don’t worry, be invested

Last week, TSMC revised up long-term guidance. Long-Term US$-revenue Cagr 20% -> 25%, AI growth 45% -> 50% Cagr, bottom gross margin 53% -> 56%. Compared to this, Consensus has revised up modestly. How much upside?

It’s less a question of Consensus upside than 1) valuations are reasonable 2) TSMC is the simplest trade in terms of monopoly with pricing power. 2nd best is still Micron.

Don’t worry, be invested. Tomorrow: Intel’s results. Buckle up – one way or the other.

TSMC has a few unusual characteristics

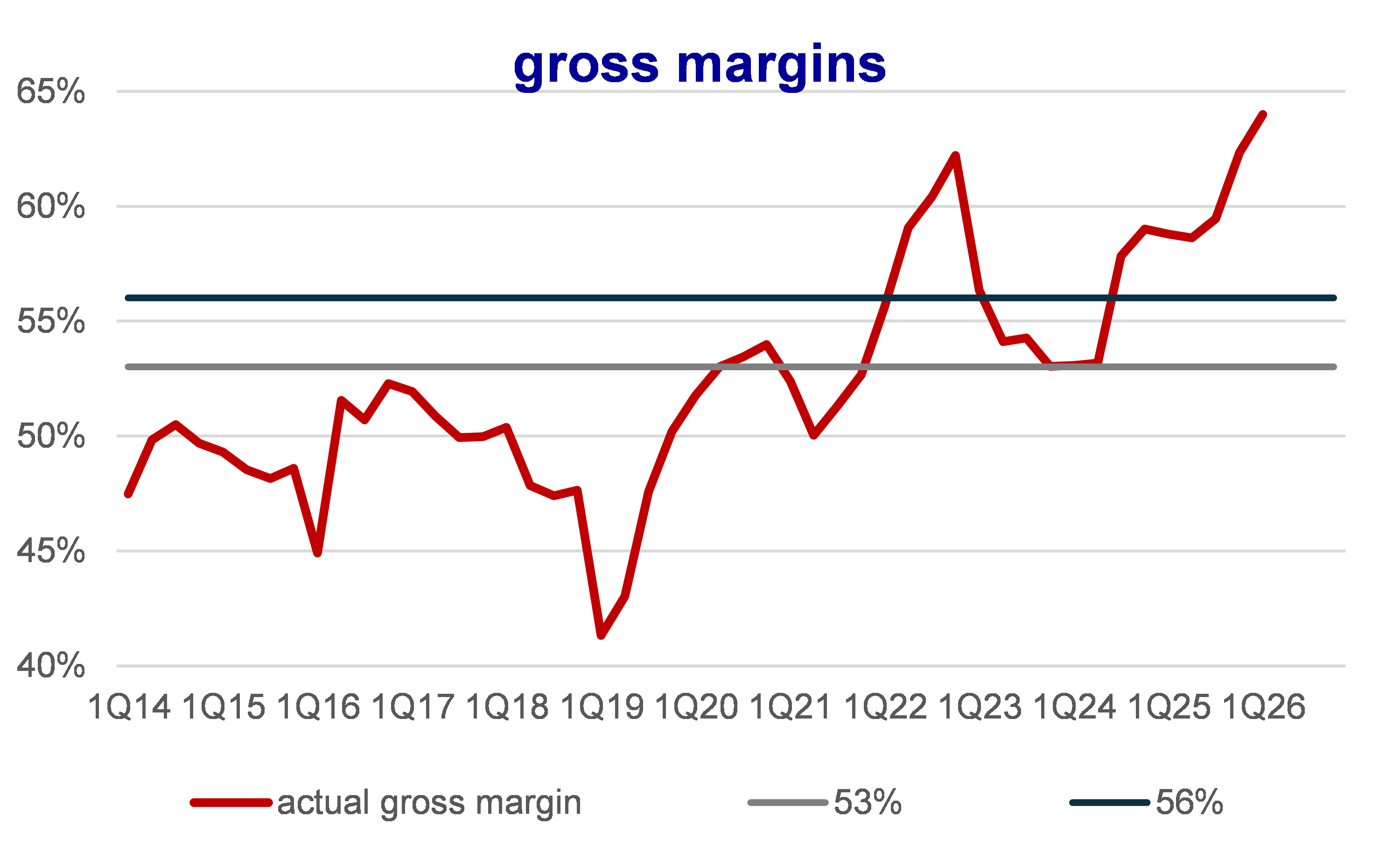

The tone of official communication is always conservative. If the CEO says that 2026 revenue growth is ~30%, it means that he’s darn sure. This conservatism sometimes doesn’t make sense: CFO increased bottom gross margins guidance from 53% to 56%. You could say ‘how is this possible?’ when 2025 gross margin was 60%, 1Q26 guidance 64%?

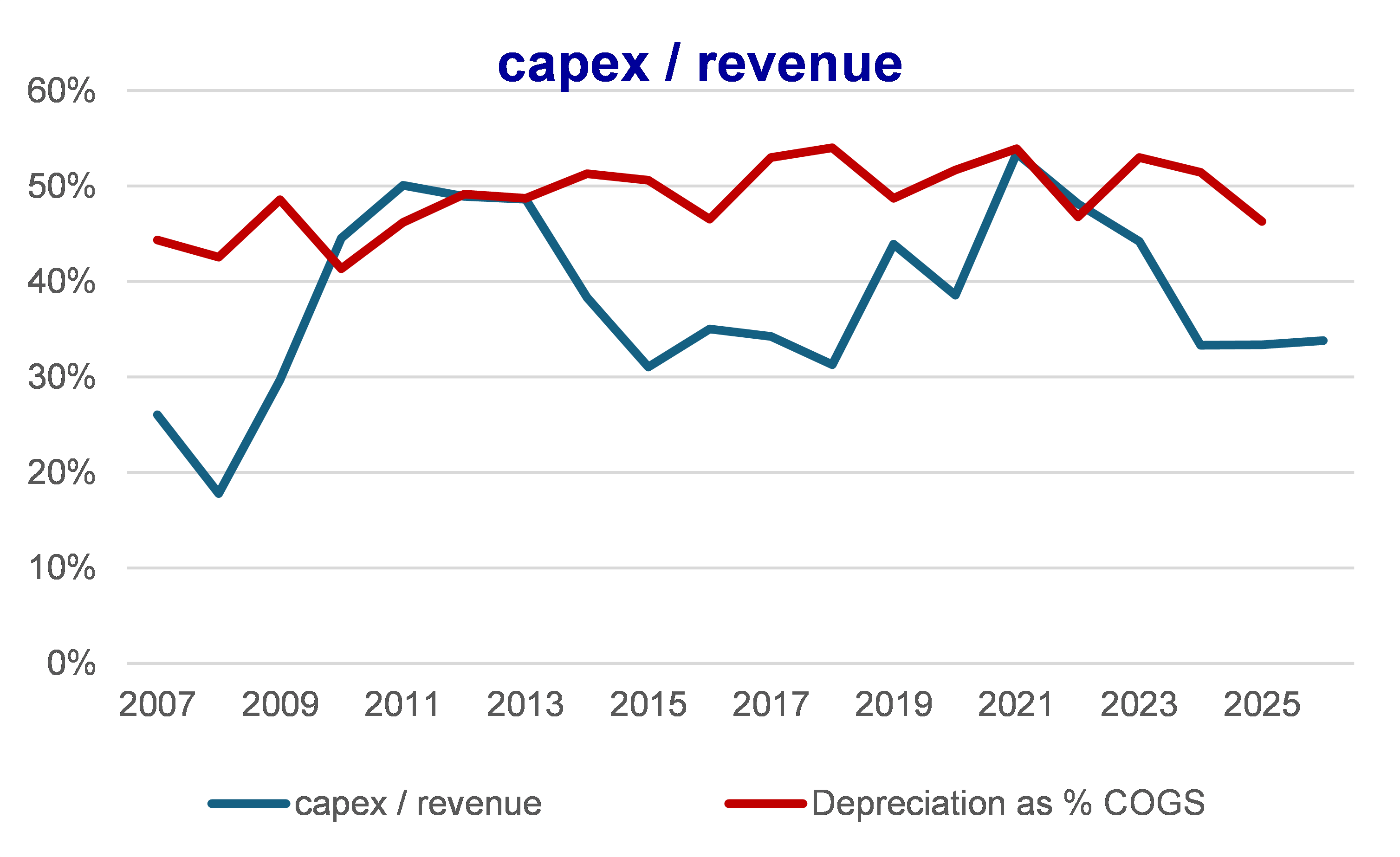

That’s because (2nd characteristic) TSMC has a sophisticated risk-planning mechanism where they stress-test every possible downside scenario. TSMC also has a fleet of industry analysts that look at every segment of end-demand. Why do that? The core reason is that Capex intensity is high at 40%. This means that to make $1 in revenue, TSMC needs to spend $0.40 on equipment. High Capex becomes high Depreciation burden, which accounts for 50% of Cost of Goods Sold.

This implies 2 things:

A bad technological decision – ie investing in the ‘wrong’ equipment or ‘wrong’ manufacturing process will haunt you for the next 5-7 years (that’s the depreciation period). If the manufacturing process was poorly designed, yield rates will be low, high depreciation will kill margins: that’s Intel over the past 5 years.

If there is an economic downturn, utilization will drop, fixed costs and depreciation will remain, and margins will drop drastically.

In short: bad investment choices will prove very expensive (again think about Intel).

Each quarterly earnings, TSMC’s CFO manages to repeat the “6 factors that determine profitability”: 1) ‘leadership technology’ means best yield rates, that in turn become 2) pricing power, 3) utilization, 4) cost control, 5) product mix and 6) FX.

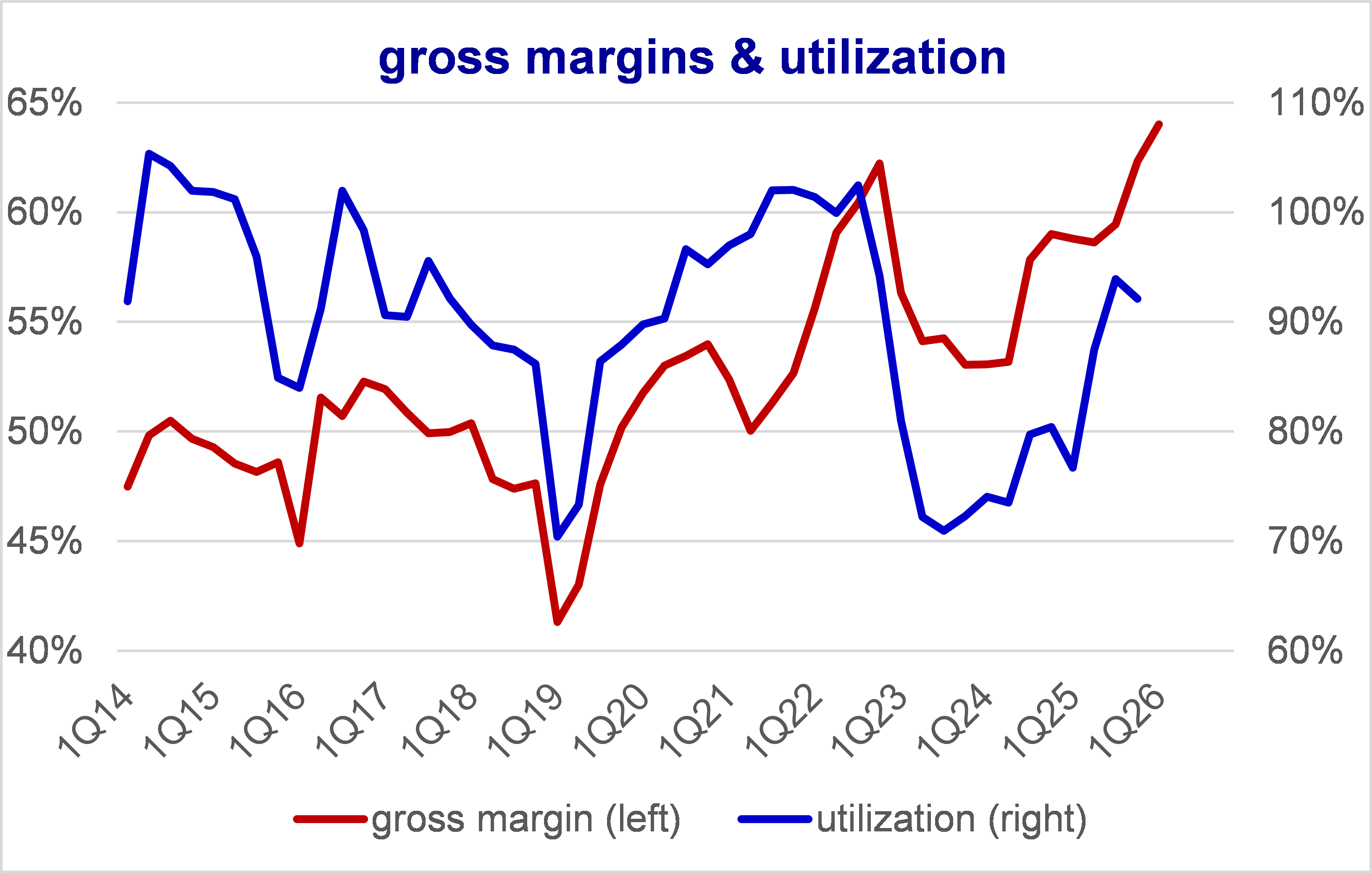

Yes, but in the short term, in a cyclical sense, gross margin is very highly correlated with utilization – which means with end-demand trends (AI strong, smartphone weak) and with the macro-economic cycle. Chart below.

In the long-term, or in a structural sense, the direction of gross margins reflects both 1) the quality of R&D and engineering: cost control, yield rates, all kinds of ‘productivity’ and 2) market structure: TSMC is an EUV monopoly and has increased wafer price very nicely since 7nm started. The CFO calls all these factors ‘leadership technology’.

You can see this clearly in the chart below:

In 2023-24, utilization dropped sharply from ~100% to 70% (blue line). That was the post Covid inventory bubble in Auto, Industrial, PC, Smartphone, etc. Also, TSMC built a bit too much 7nm capacity in 2019-21.

Given the magnitude of the decline in utilization, gross margins should have declined more (red line). But didn’t, because wafer price / gross margins on the new stuff (EUV 7-5-3nm) is super high.

In this chart, you can see both the cyclical (end-demand slowdown, utilization down, margins down) and the structural (monopoly pricing power, margins reach higher troughs and peaks).

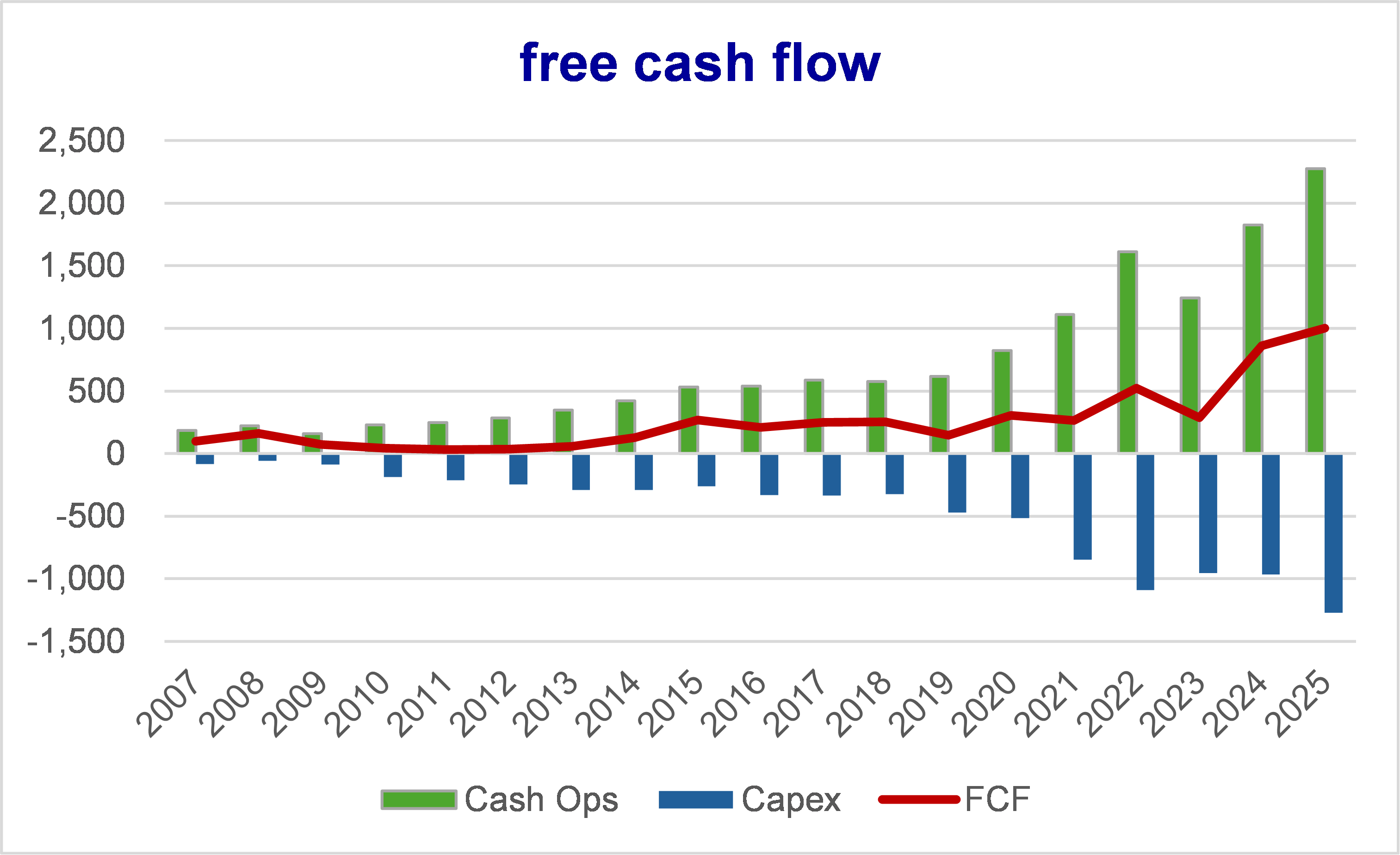

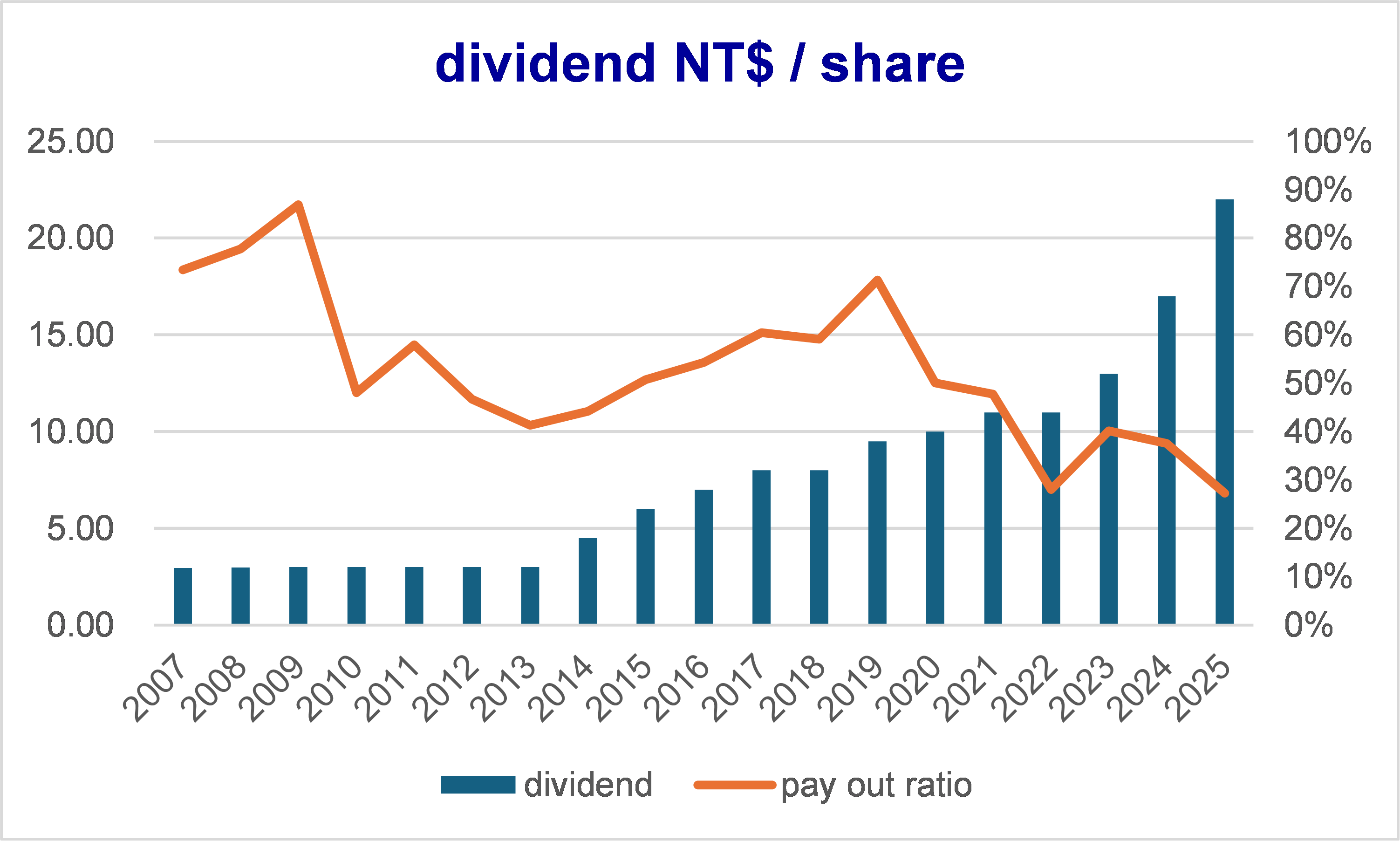

3rd characteristics, and the other reason to do complex stress-test: TSMC does not want to never ever be cash flow negative, TSMC doesn’t want to never ever have to cut dividend.

Over the past 19 years, TSMC has never been free cash negative. Dividends have never been cut. Quite an achievement.

Last bit of the 3rd characteristic, as I’m not a sell-side analyst any longer I can tell you, TSMC doesn’t want to answer cry-babies whining investors. Gross margins could drop to 60% and we told you 56%, right?

Still, it doesn’t mean that management makes no mistakes. Like the rest of the industry, TSMC does not see macro events coming, including inventory overbuilt (2023), slowdown in PC, Smartphone demand (2019), etc. Also, TSMC has historically over-built capacity 2 times (28nm in 2006-08 and 7nm in 2019-21).

We have to remember all that when thinking about :

1) TSMC guidance: it’s a conservative outlook

2) Reasons why Consensus stays just below a conservative outlook

PAYWALL