TSMC 2Q25: a number of very positive messages, plus a major contradiction on 4Q25 revenue

NT$ appreciation has a very large impact on revenue / margins but TSMC beats consensus in 2Q, 3Q guidance is in-line. FX impact is large, but other factors (higher utilization, cost control) partially neutralize it.

This will be controversial: management increase 2025 US$-revenue growth from mid-20 to 30%. Yet, this implies that 4Q25 US$-revenue growth will collapse (2Q 44% YoY, 3Q 37%, 4Q 9%) and NT$-revenue growth will be negative in 4Q (chart below). Do I believe this?

At the same time, mngt gives a long list of very positive messages on AI demand, N2 ramp, full utilization of EUV nodes. My take: TSMC had to increase 2025 guidance, but they do their “very conservative” thing. This could lead to a little bit of stock price weakness.

Comments on the contradiction between 2025 revenue guidance and the very bullish management’s statements

We know 1-2Q25. We have an official guidance for 3Q (US$-revenue $32.4bn) and for 2025 (30% YoY US$ growth). So we can calculate 4Q. The only assumption below (chart and table below) is FX 1US = 29NT, same as 3Q guidance.

This is what “30% YoY US$-revenue growth” implies: a very large decline in growth in 4Q.

At the same time, management gives very bullish statements:

“AI demand is very strong. Haven’t seen this kind of demand for a long time.

7nm and below capacity is very tight.

Our capacity is very very tight. Cycle time is 4 months. There is no way you can pull in anything.

TSMC is working hard to close the gap between supply / demand. Unprecedented capacity expansion”

What can we conclude:

TSMC management is being its usual very conservative self – remember for ex:

TSMC gives a “53% and above” gross margin target when they deliver 58%. Then management stress “and above”. But they won’t commit to more than 53%.

3 months ago, revenue guidance was “close to mid-20% YoY” and now its 30%. Given 4-5 month production time, plus 6 months firm orders, management definitely knew 3 months back that growth was 30%. But they maintained a low guidance.

Capacity is full, capacity addition is at its max and growth will indeed slowdown a lot in 4Q: no room to make more wafers. That’s possible but in that case, revenue should not decline QoQ in 4Q (table above).

Capacity is full, TSMC is “working very hard to close the gap between supply / demand” does not contradict a very positive demand outlook.

How do we get to 4Q revenue flat QoQ? with 2025 US$-revenue growth at 33.5%. Table below. That looks like a worst case scenario.

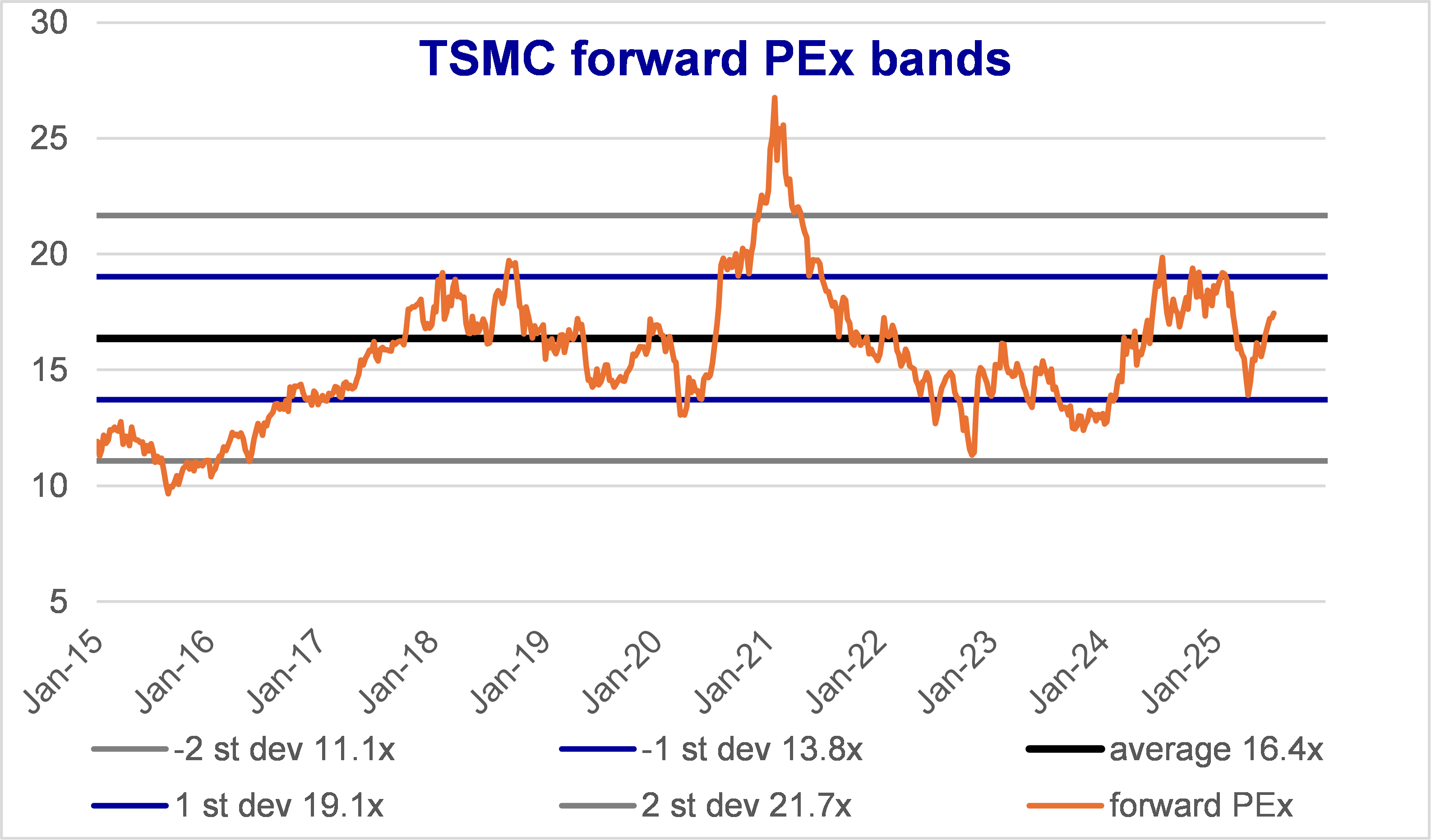

What you’re missing below the paywall:

2Q25: large negative FX impact, yet TSMC beats Consensus

3Q25: large negative FX impact to continue, more visible on margins, yet TSMC guidance is in-line with Consensus

Mechanics of NT$ appreciation

Outlook for N2 is very strong

TSMC GigaFab management

Reiteration of the dilutive impact of overseas fabs

Consensus expectations, valuations