Semiconductor Production Equipment (SPE): all big firms have increased revenue forecasts, ~20% growth in 2026, similar or more in 2027

AMAT was the last SPE vendor to report, like others it has revised up its revenue outlook.

Similarly, estimates for the end-market, the semiconductor market, are going up, supported by a strong 1Q earnings season, and strong guidance.

Positive: growth keeps beating expectations. Negative: peak growth in 2026-27, valuations, maybe?

The Semiconductor Production Equipment (SPE) sector is made of 2 different segments:

Wafer-Front End WFE equipment makers. They make equipment to manufacture the wafers inside the Intel, SK Hynix, TSMC fabs : AMAT, ASML, KLA, LAM, Tokyo Electron.

Back-End equipment makers, or Test & Packaging T&P. The equipment are used to test (Advantest, Teradyne) and package the semiconductors (ASMI, ASML, BESI, Hanmi, K&S). The equipment are used by Intel (EMIB), TSMC (CoWoS) and also 3rd party back-end forms: Amkor, ASE, etc.

This report is about the 5 big Wafer Front-End equipment firms: AMAT, ASML, KLA, LAM, Tokyo Electron.

Everybody is revising up

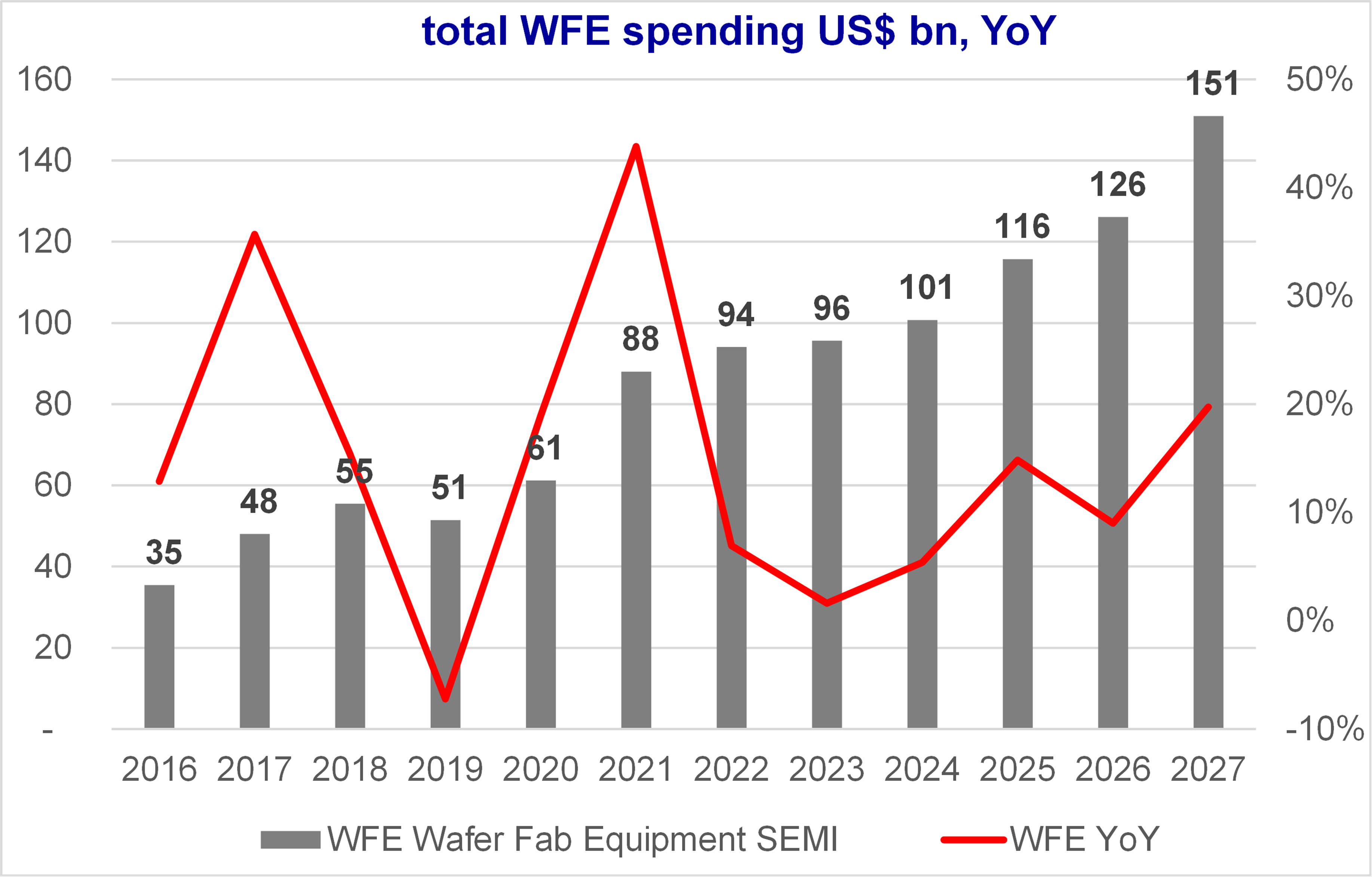

We have a higher industry authority in the SPE sector, so let’s look at its forecasts first.

SEMI.ORG WFE forecasts: modest, boring and wrong

2026: 126bn up 9% YoY

2027: 151bn, up 20% YoY

The latest press releases are here and here.

These numbers are too low, and the 5 big WFE firms have revised up their forecasts and provided higher estimates. The only thing interesting in Semi’s estimates is that 2027 growth is much higher, 2x higher than 2026. Could be true – it’s directionally correct.

This is semi.org data:

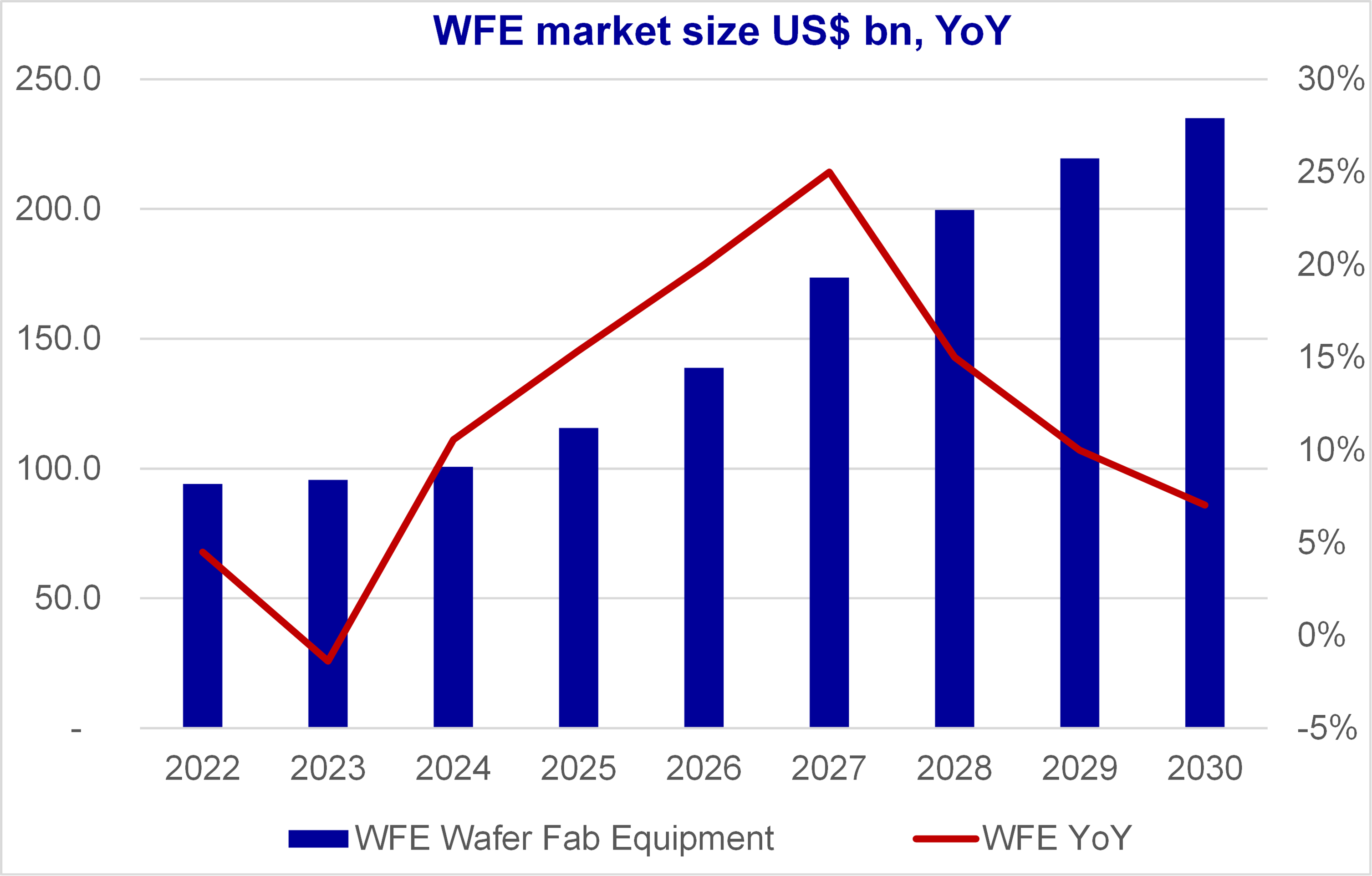

Revenue / market value estimates of the 5 big Wafer Front-End equipment firms

AMAT

Didn’t cite a total WFE dollar figure, but said their own semiconductor equipment business will “grow more than 30% this calendar year.”

2027–28: “I’m having constant conversations with customers, and they’re looking at ‘27 and they’re looking at ‘28.” Described leading-edge foundry-logic, DRAM, and advanced packaging as accounting for “more than 80% of the year-on-year growth in total WFE spending in 2026 and a similar profile in 2027”, “sustained, multi-year revenue and profit growth.”

ASML

No WFE dollar figure cited.

Has increased its 2026 revenue range from EUR 30-40 bn (mid-point 35bn) to EUR 36-40 bn (38bn)

Shipping “at least 60” low-NA EUV systems in 2026, growing to “at least 80” in 2027.

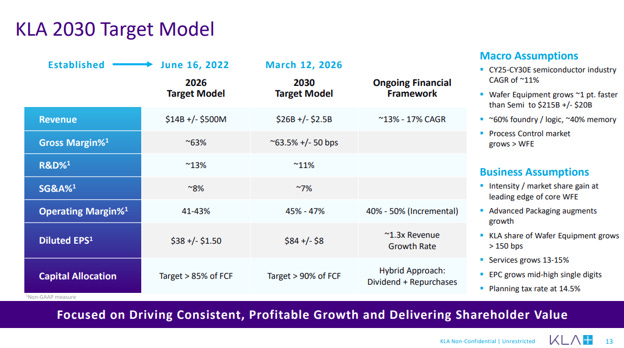

KLA

The 2030 revenue target is based on ~15% growth Cagr. This is based on WFE market at $215B ±$20B.

WFE 2025 baseline ~$120B.

2026 now “expected to exceed $140 billion” — increased from the $135–140B

2027: “today we expect the 2027 year-over-year growth rate to be higher than 2026.” CFO Bren Higgins: “there’s no question ‘27 is going to be a massive buildup.”

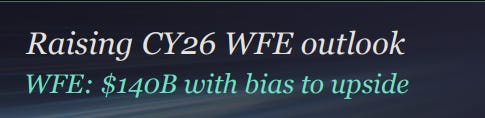

LAM

2026 WFE $135bn (January guidance), now increased to “$140 billion with a bias to the upside.”

From $116bn in 2025, $140bn means up 20% YoY

2027: “WFE is going to be nicely growing next year”, the firm declined to give a specific number but “firmly” positive.

Lam flagged ~$40B in NAND conversion spending needed over the next few years, with the majority now pulled forward to before end of 2027.

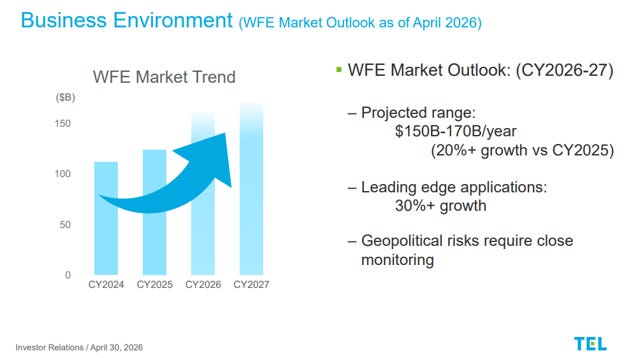

Tokyo Electron

Tokyo Electron is the most bullish with WFE for both CY2026 and CY2027 in the range of “$150–170 billion per year”. CEO Kawai on the $170B upper end: “I think $170 billion level of WFE market is achievable when I look at current customers’ investment plan.” Let’s assume this means:

2026 WFE $150bn, that’s 30% YoY

2027 WFE $170bn, that’s 13% YoY

The “range” is 20%+ growth versus 2025, that must be 2-year Cagr

My conclusion is:

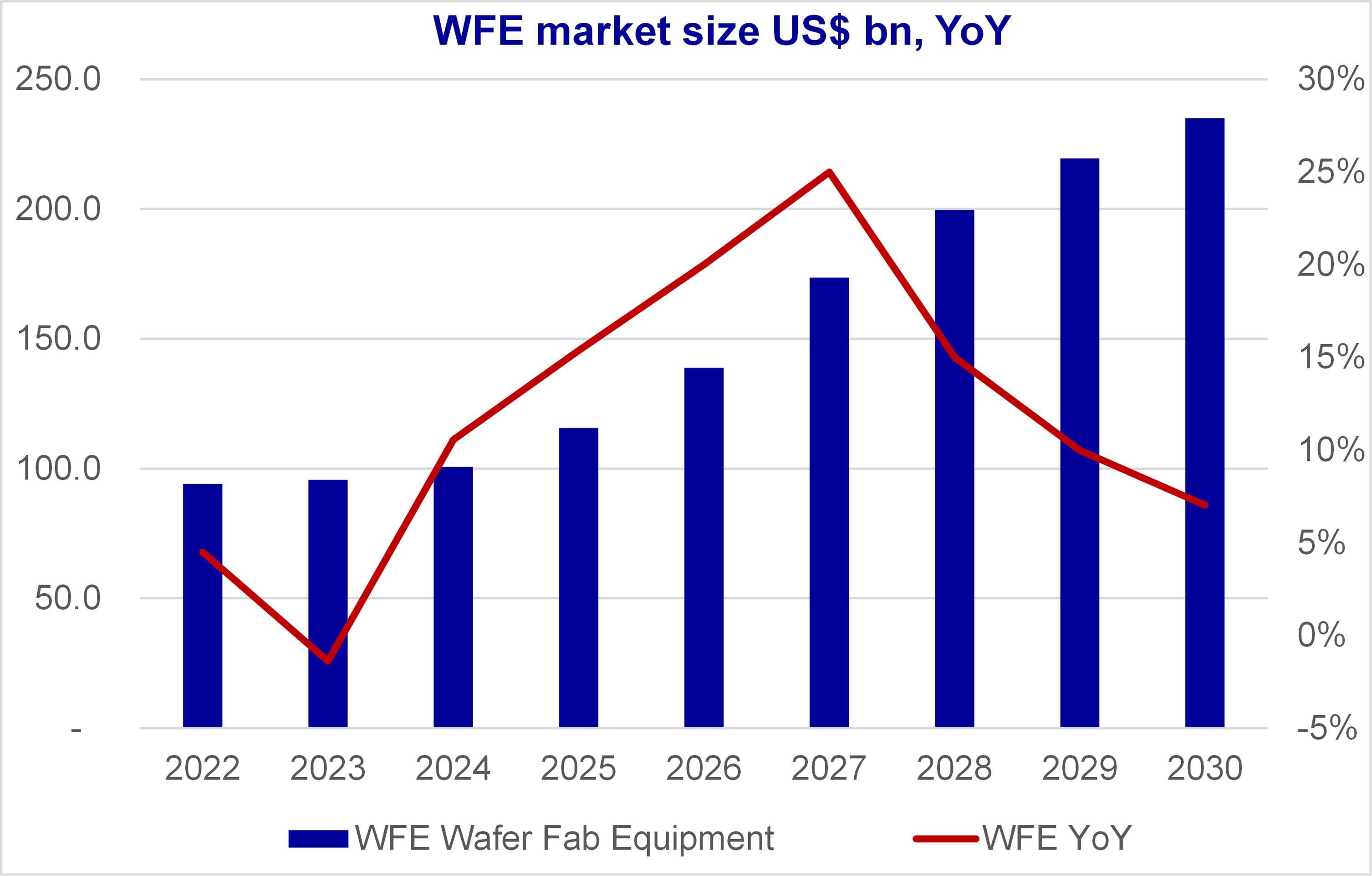

We take all this, we remember ASML and KLA 2030 estimates, we add the semiconductor market value (I’ll get back to this in a few days), and we have a range of WFE spending i.e. revenues of AMAT, ASML, KLA, LAM, Tokyo Electron, plus a few smaller firms, that looks like this:

You could say that it’s great, so much growth

You could also say that peak growth in 2027 is not good for stock prices – especially after the huge rally of the past month / year

But if you think this, you also have to remember that 2030 is very far away and nobody has an incentive to provide targets that they can’t reach.

In summary, there are 2 big positives and 2 negatives to watch carefully

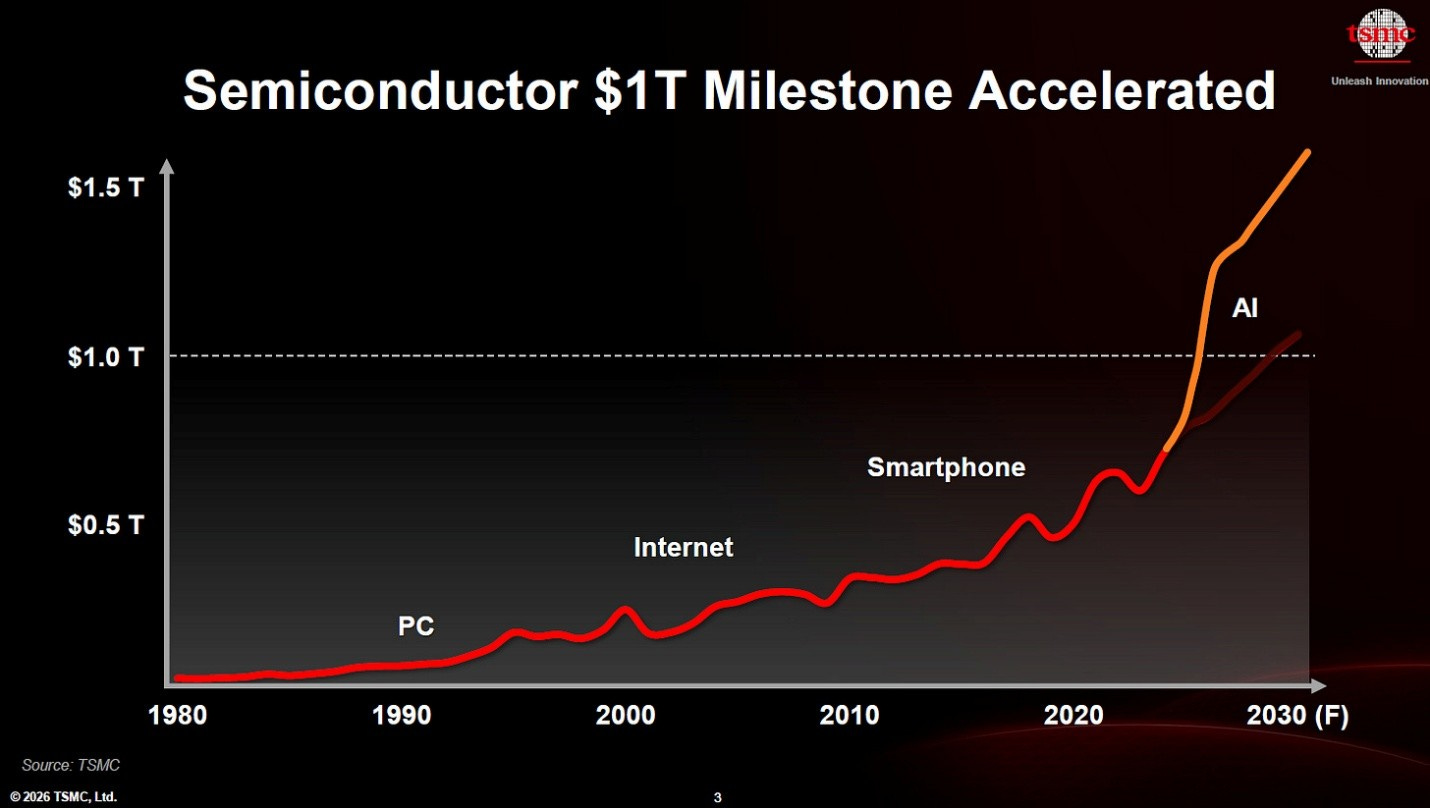

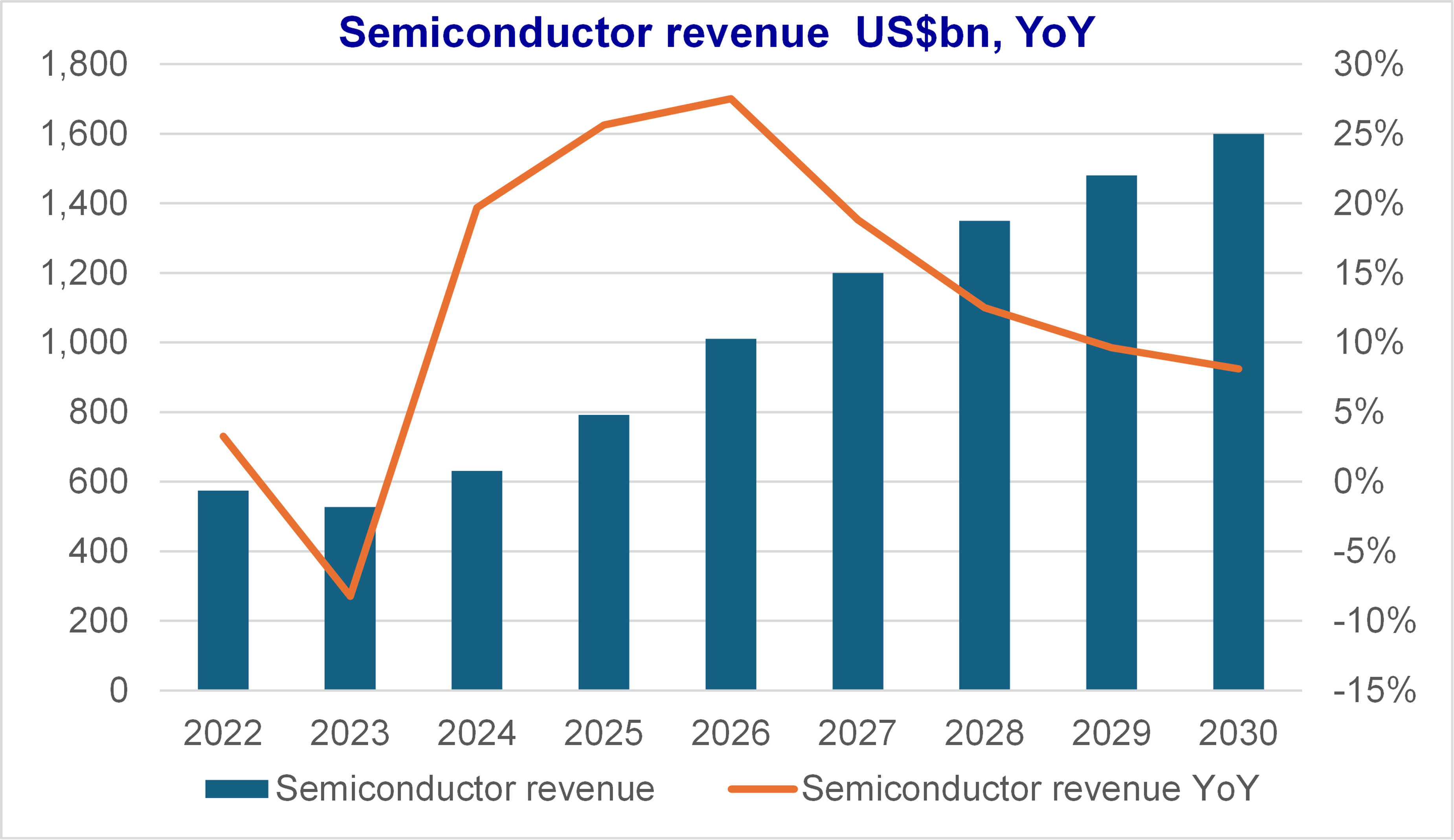

Positive 1: the end-demand estimates keep increasing. That means estimates of the size of the semiconductor market keep going up. Yesterday, TSMC said $1.5 trillion by 2030.

You can read Jeff’s summary here, here.

This means something like this, my estimates to get to $1.6 trillion by 2030.

PAYWALL BELOW