Semiconductor market value. TSMC said $1.5tn by 2030. WSTS says $1.9tn in 2027.

We’ll reach $2.5 trillion by 2030?

Estimates of the Semiconductors value keep going up – quickly. Memory as prices double and triple in 2026, plus (secondary) volume growth (HBM, RDIMM). Logic because unit demand is going up (AI), plus (secondary) cost increase.

You’ve been told during the last earnings season: Agentic / Inference demand is going ballistic. The key question is not “is there demand” but can token cost decline fast enough for the Capex to have a nice ROI?

For the Semi industry to reach $2.5tn by 2030, how much AI Capex and revenues do we need by 2030?

Revising up

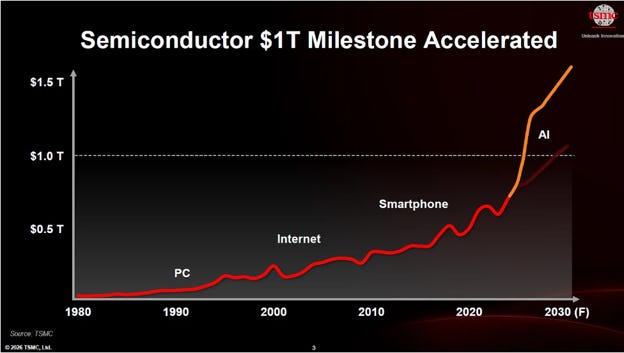

Long long time ago, Mc Kinsey said that the Semi market will reach $1 trillion by 2030. Today, this forecast is irrelevant: it was published in 2022, the main driver was Automotive / Industrial, it was before AI, before HBM, before EUV explosive costs (i.e. TSMC 5nm wafer price was $17k. Tomorrow, 2nm price ~30k).

I only mention this because people still refer to it. For ex, TSMC in its May ’26 Tech Conference in HsinChu said: $1 trillion is too low, it’s $1.5 trillion. That’s the context of this slide below.

One month later… Memory contracts (HBM4, RDIMM / MRDIMM) for 2026 and 2027 are settled. Nvidia and AMD have reported and

Nvidia CFO Colette Kress increased the “revenue visibility figure” from $500B over 2025–2026, to ~$1 trillion through 2027.

Jensen went to Taipei – everybody is in Taipei, it’s Computex time and dropped $150bn:

“Taiwan is incredible at technology manufacturing. This is the epicenter of the ecosystem... 4 years ago, 5 years ago, Nvidia was spending about 10, 15 billion dollars a year in Taiwan. Now we’re spending 100, going to 150 billion dollars in Taiwan each year”

AMD Lisa Su went to Taiwan and AMD also has 2-3 years visibility:

“we have very good visibility now into the deployments that are on track for 2027. And when I say good visibility, it’s visibility down to which data centers are the GPU going to be installed in”, “we’re now talking about ‘27 CPU demand, we’re talking about ‘28 CPU demand. And so that allows us to just plan much better as we go forward.”

“If AI were a nine-inning baseball game, we’re probably only in the third inning... the global artificial intelligence boom remains in its early stages”, she said.

I am just saying that demand estimates are flying higher every day – what does it mean for total Semi industry value?

I wrote yesterday on TrendForce Memory value forecasts, going to $1.3 trillion in 2027.

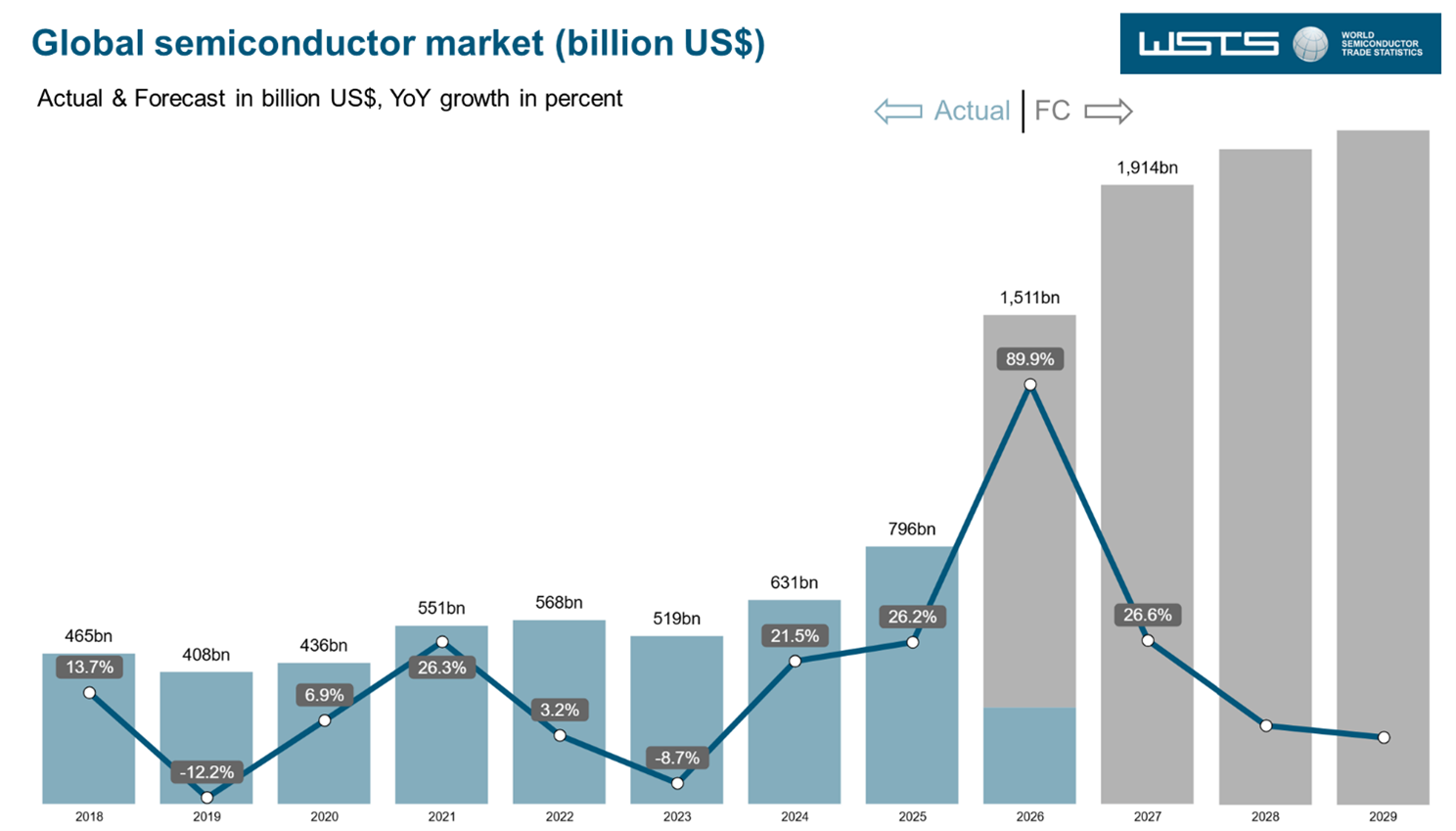

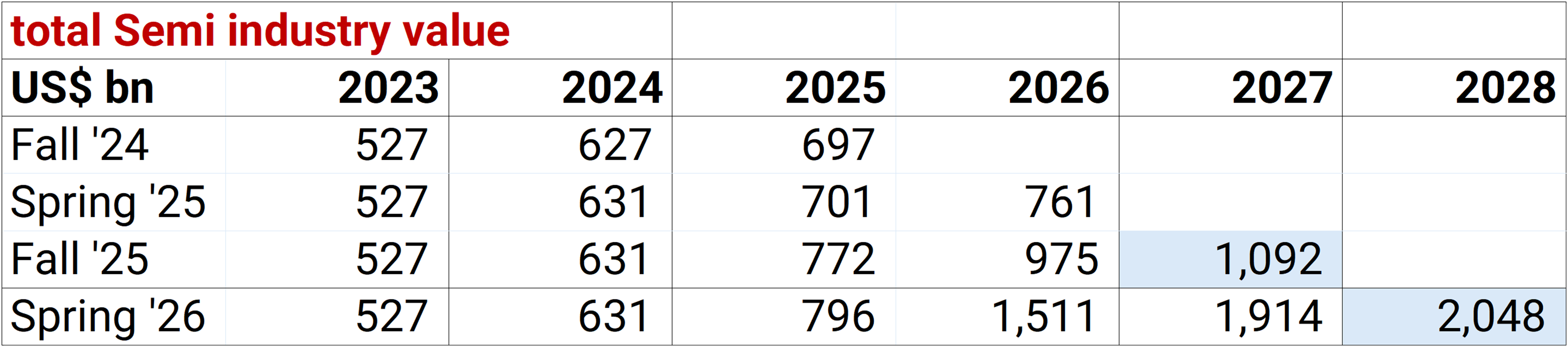

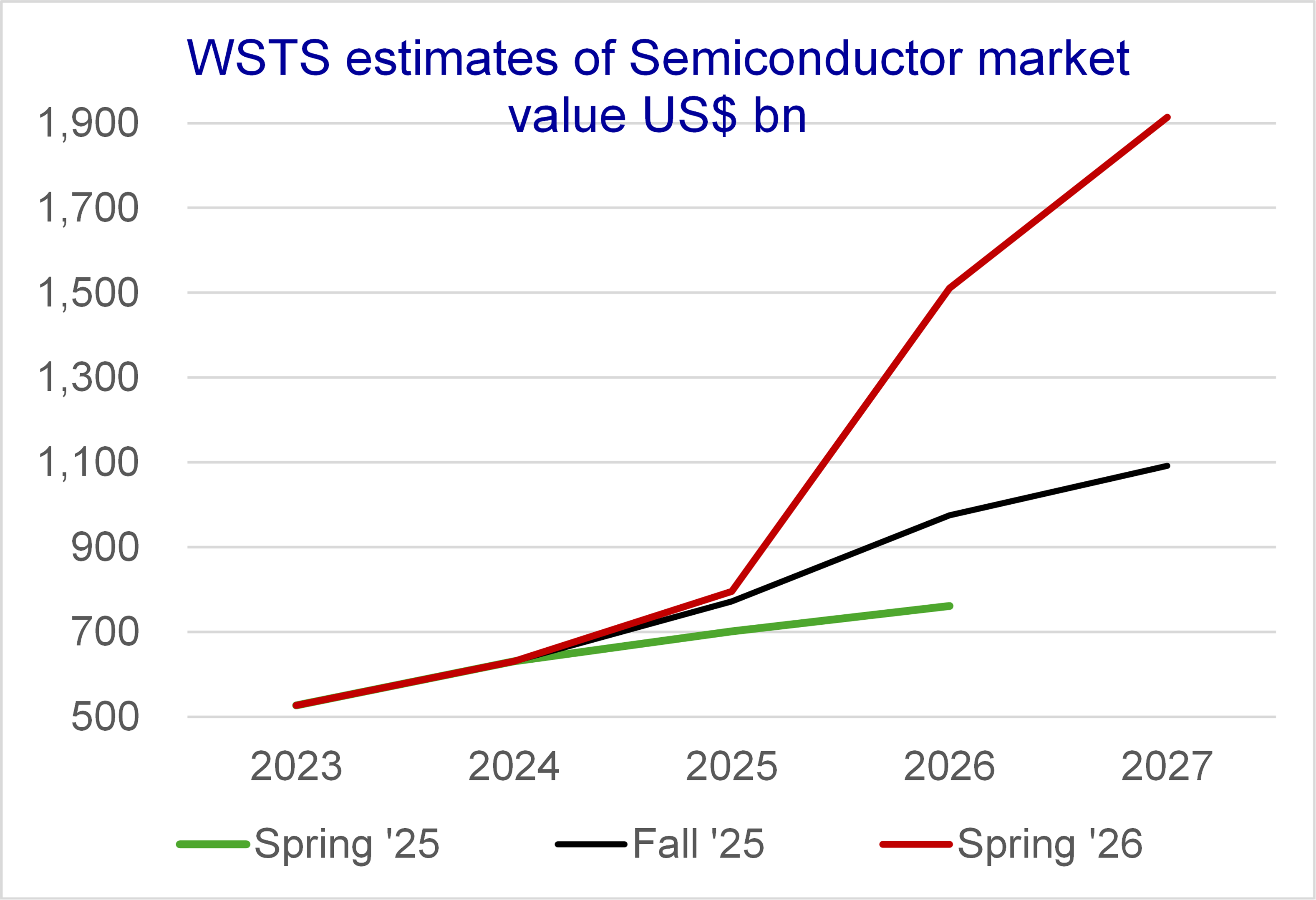

I was going back to my spreadsheet on total Semi industry value but WSTS conveniently published their forecasts.

The numbers in blue cells are not published by WSTS, it’s me extrapolating based on WSTS’s charts.

Zooming in:

Sorry TSMC, it’s not $1.5tn by 2030, it’s $1.5tn in 2026. I guess we could guestimate $2.5tn by 2030.

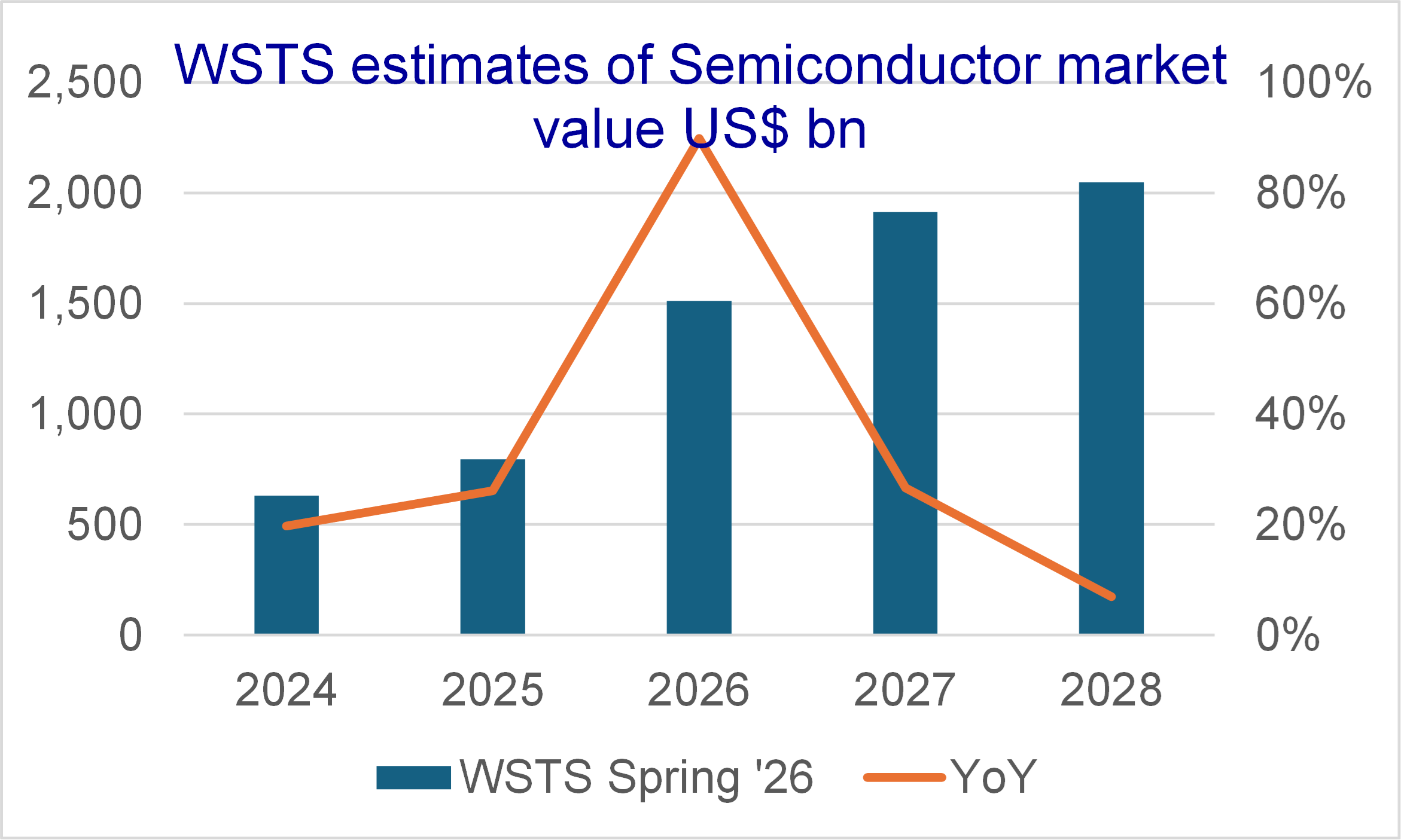

In terms of revisions, and to visualize the steepness of estimates increase, WSTS (total Semi) and TrendForce (Memory only) are similarly ballistic. Here are the last 3 forecasts from WSTS:

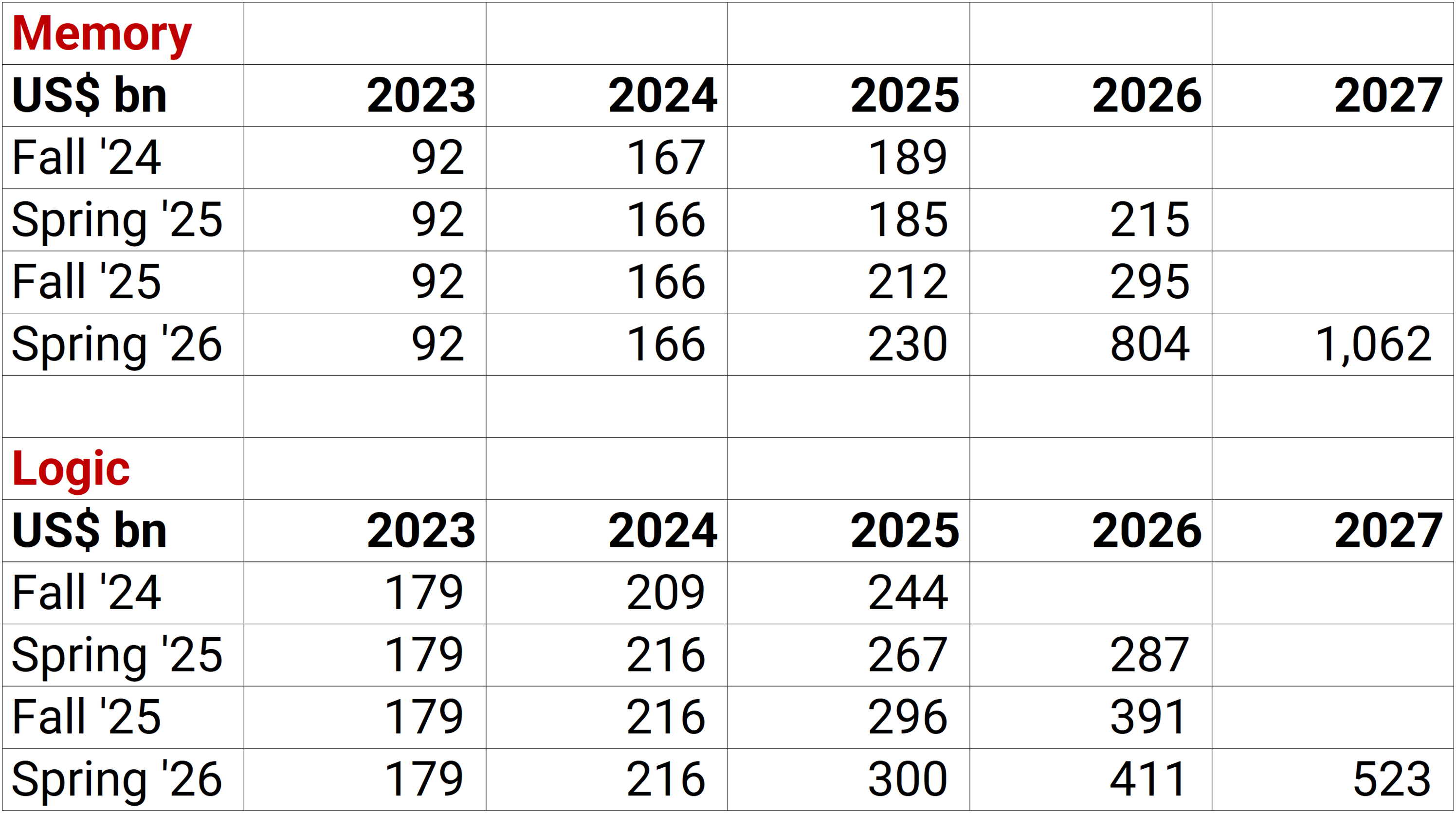

Looking at the details of WSTS forecasts (table below):

Similar to TrendForce, the biggest growth is Memory

WSTS is a bit lower than TrendFroce but it’s in the ballpark. 2026 $804b versus 889b. 2027 $1.1tn versus 1.3tn.

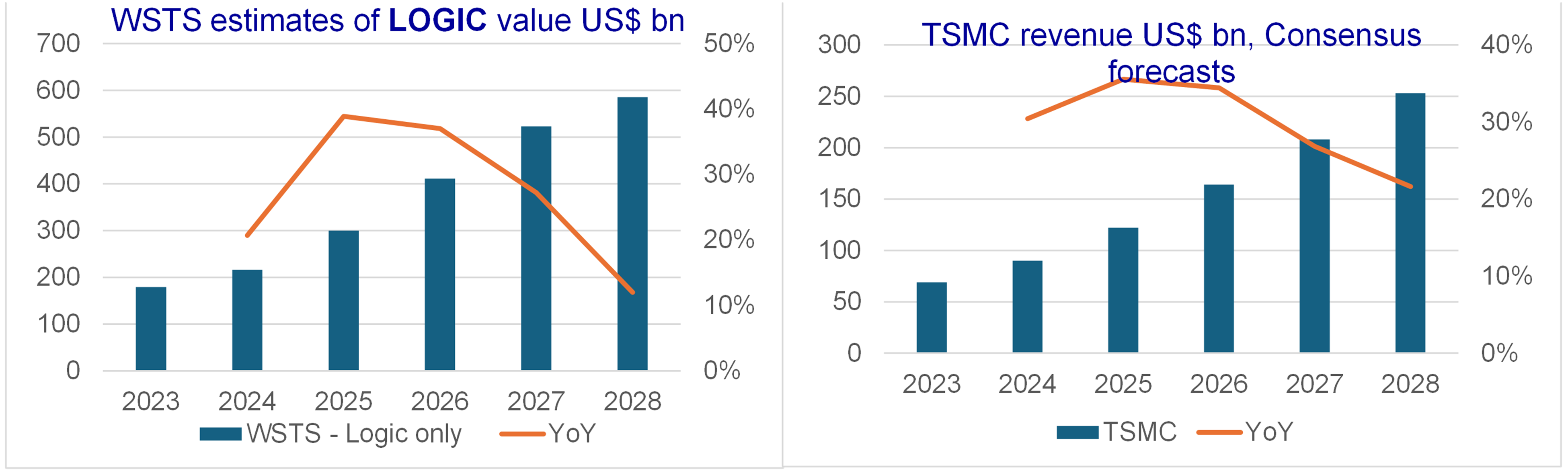

For Logic, growth is lower because the main driver is unit growth, and secondary driver is cost increase (cost because 3nm -> 2nm -> 1.6nm wafer price goes up ~20% by generation – but that not a price increase).

We can compare WSTS Logic and TSMC Consensus forecasts. It is “consistent”, with WSTS is lower and a bit too low, as it should be 1) TSMC will grow faster than many other Semi firms 2) TSMC analysts have a better grasp on capacity increase than WSTS on total demand.

So that’s fine. Again, it’s in the ballpark.

Let’s say it’s gonna happen. Let’s say we hit $ 2 trillion Semiconductor revenues in 2028 and $2.5 tn in 2030.

Where is all that money going?

You’ve been told during the last earnings season, Agentic / Inference demand is going ballistic. I’m not going to copy tons of excerpts from transcripts. Just this from Microsoft, Satya Nadella:

“A new app platform is being born. You can think of agents as the new apps” “We are at the beginning of one of the most consequential platform shifts that will change the entire tech stack as agents proliferate and become the dominant workload.”

Remember the overall conclusions:

Inference demand is now bigger than Training demand — Broadcom was most explicit; Nvidia, AMD, and Intel all confirmed the shift. Agentic AI is driving a CPU renaissance — Intel and AMD both raised CPU TAMs.

“Agents are the new apps” Microsoft said it most cleanly. Amazon, Google, and Nvidia said it in different words. Every hyperscaler is building an agent deployment platform.

Inference cost reduction is the key unlock — Amazon, Google (TPU 8i), Nvidia (Vera Rubin at 35x better inference) and Microsoft (40% inference throughput improvement) are all racing on cost-per-token.

Important conclusion 1:

AI Capex is accelerating and the issue is not demand, not applications, it is the cost curve of token generation. It got to become 50x or 100x cheaper. My gut-feeling is that we are the the way to get there in a few years.

Nvidia’s 35x increase in Inference thruput (with Vera Rubin) means from one Gen to the next Gen of GPU.

Microsoft’s “40% improvement in inference throughput for our most used models across Copilot, driven by our software and hardware optimization work” means using the same existing stack.

Important conclusion 2: Hyperscaler’s revenues need to double, operating profits need to double by 2030

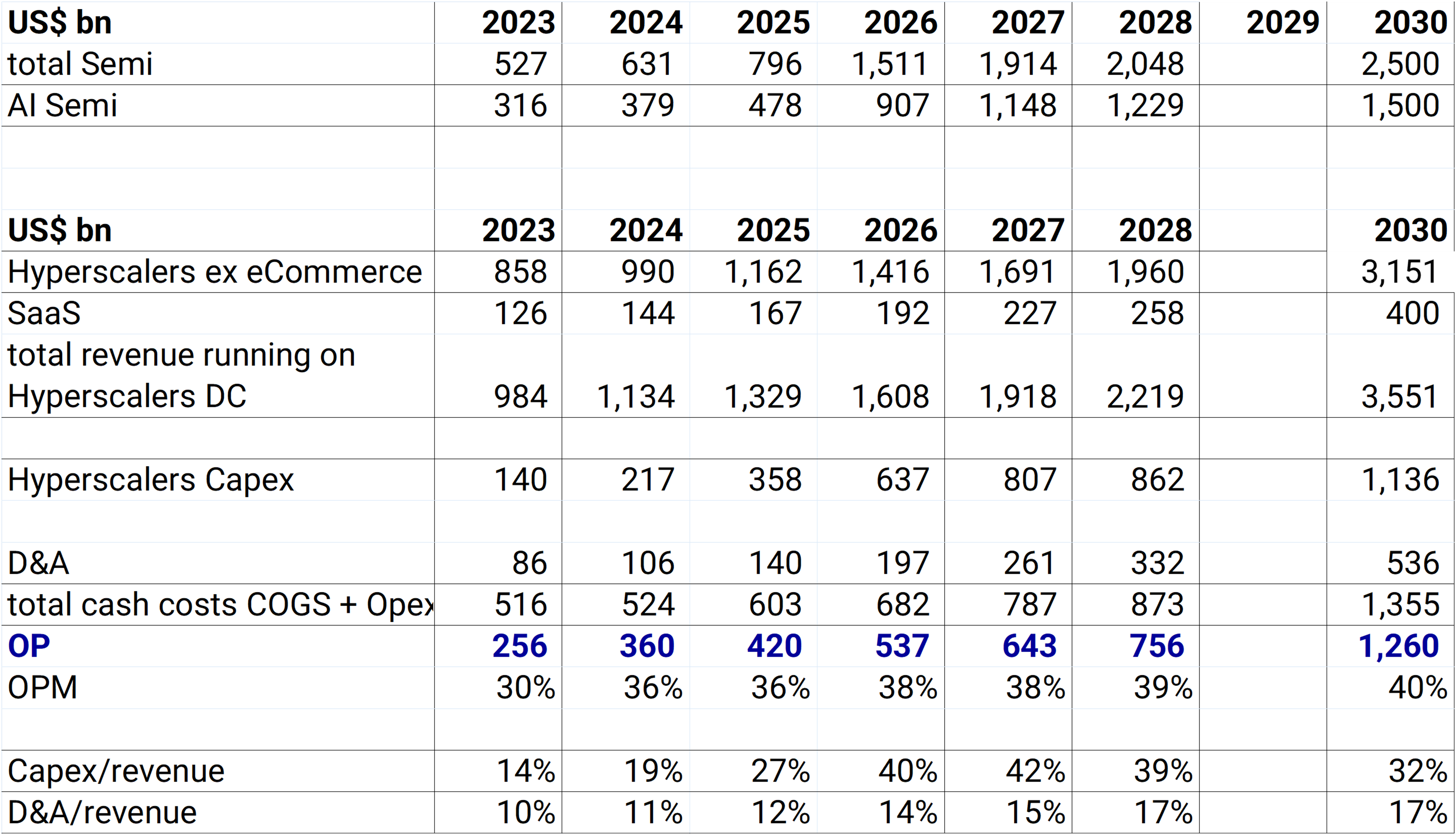

If we assume that 55-60% of Semi spending is on AI:

$1.2 trillion in 2028, $1.5tr in 2030 for AI Semi

If we assume that Semis are ½ to 2/3rd of Capex:

$1.9 trillion in 2028, $2.3tn by 2030 for Capex

50% of total Capex is by hyperscalers =

$950bn Capex in 2028, Consensus is at 860bn

$1.1tr Capex in 2030

Hyperscalers want to maintain their cost structure – actually margins are increasing as Cloud revenues are increasing. But we should have some max burden for D&A/revenue (let’s say ~30%) and Capex/revenue (let’s say below 20%).

Then what does it mean for Hyperscalers revenues, profits – and by implication for the future AI application industry?

It means that from 2026 to 2030, Hyperscaler’s revenues must more than double, operating profits must more than double to absorb that Capex and Semi value.

This is not a FORECAST. I do not know if it will happen. What I am saying is: for the Semi market to reach $2,5tn in 2030, Hyperscaler’s revenues and operating profits must more than double.

Before you conclude that revenue / profits cannot double over the next 4 years, remember that Hyperscalers operating profits have doubled over the past 4 years.

If you’d had the courage to read all this, here is Conclusion 3:

Semiconductors will outgrow Hyperscalers and AI SaaS for another ~2 ~3 years

Within Semi, Memory outgrows Logic in 2026-27

There will be an inflection point in ~2028 when Hyperscalers and AI SaaS will outgrow Semiconductors – big musical chair rotation