Is SaaS – Software getting cheap?

De-rating, but not cheap. Hyperscalers and some Fintech more interesting.

In this report, I want to think about SaaS-Software versus Hyperscalers. Which group is getting cheapest and is attractive? Is the steep Software correction justified by SaaSpocalypse? I add FinTech and eComm as well.

The overall market’s direction says that it’s not time to buy anything. However, we still can think about the merits, risk/reward, valuations/growth of different sectors.

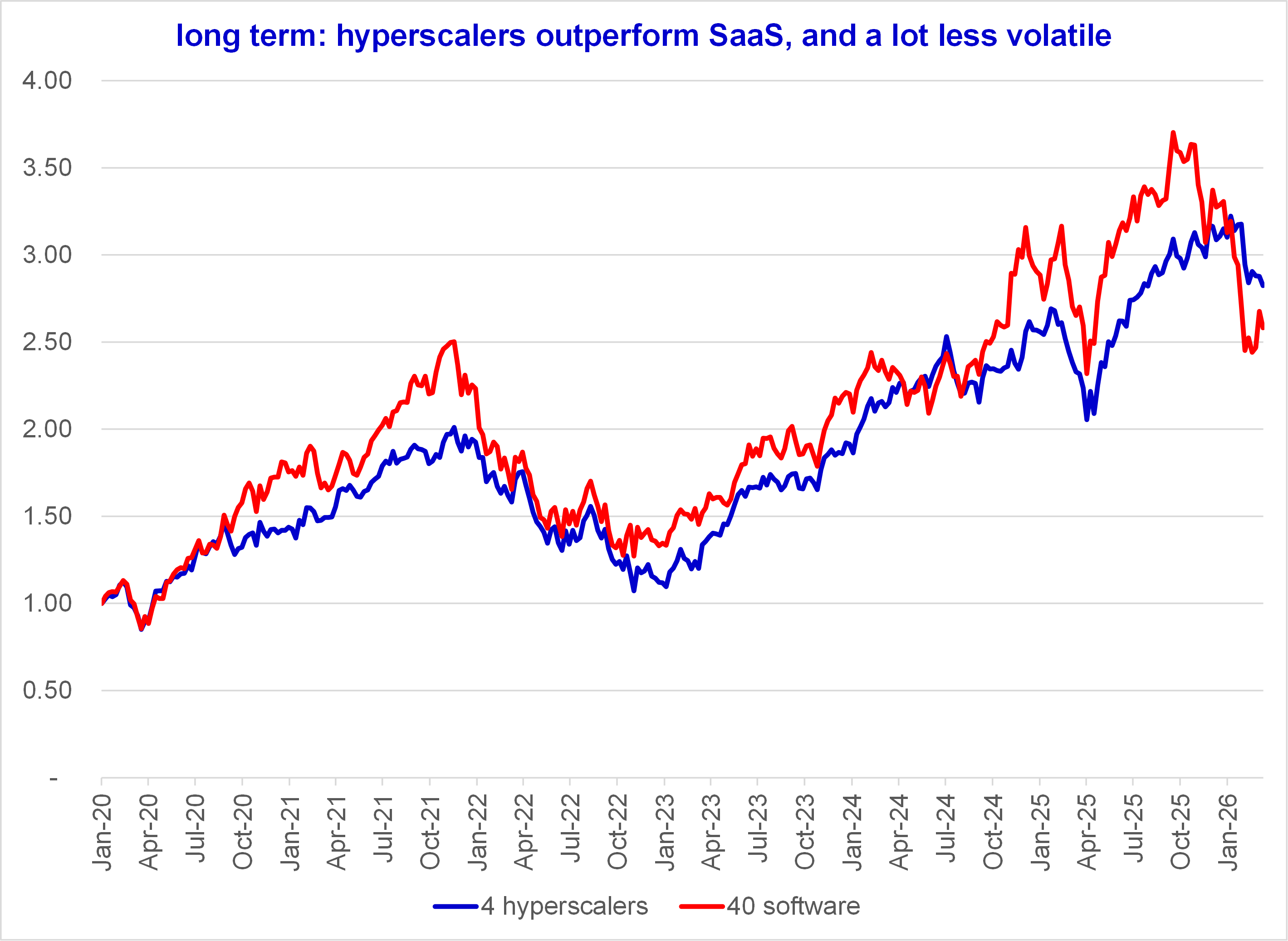

Conclusions 1) SaaS-Software has derated to a level consistent with earnings growth – this is not a discount 2) Hyperscalers tend to outperform with lower volatility 3) a couple of FinTechs are interesting.

Today, it is very hard to quantify SaaSpocalypse or the impact of 3rd party AI Agents on a specific SaaS provider. It’s hard because it is very new, because SaaS firms will develop their own AI Agents and countermeasures, because Enterprise Software is a system more than a toolbox (ie. architecture, workflows, scalability, security, audit & compliance, etc).

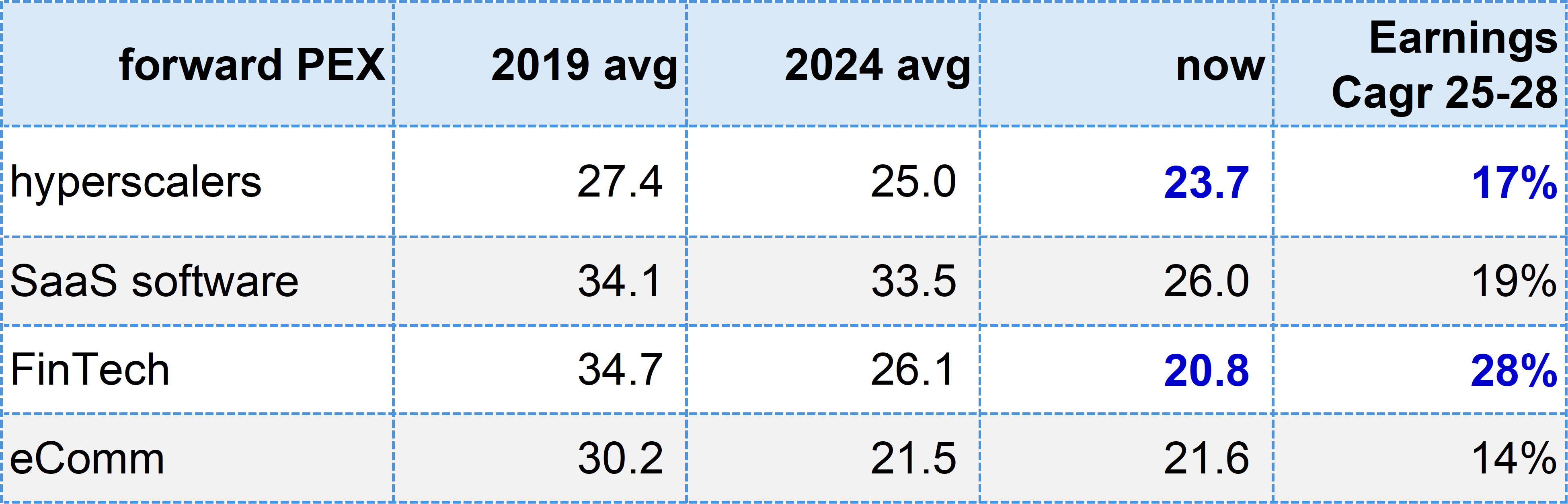

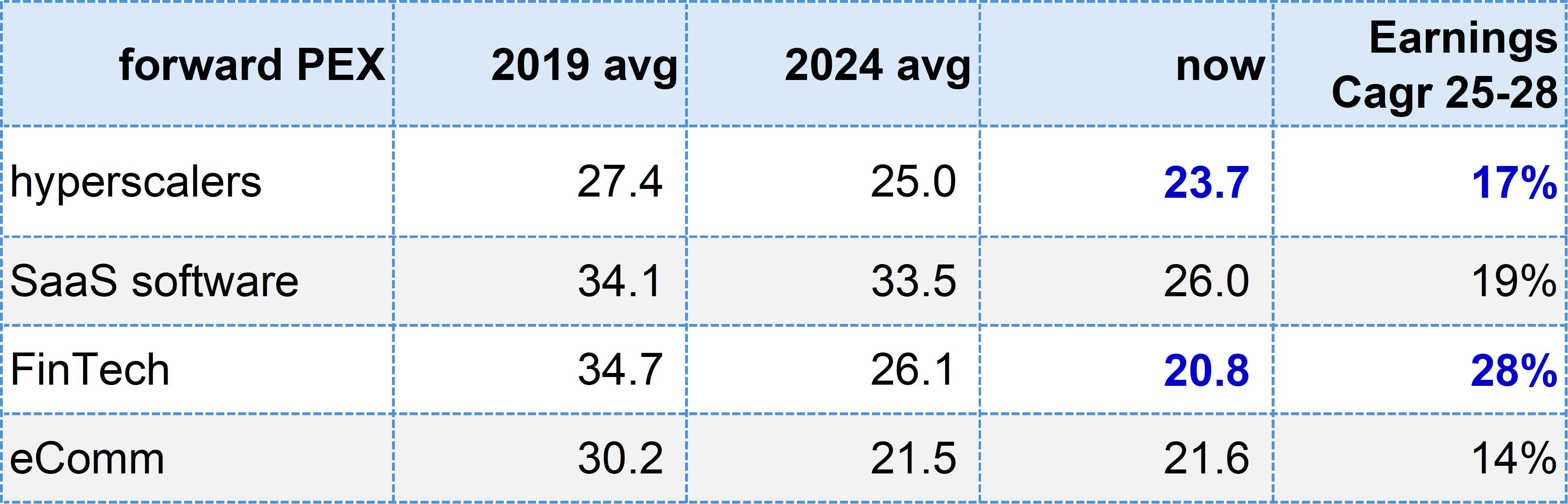

In this absence of clear quantification, what is definitely happening is valuations compression. The valuations premium of SaaS-Software (PEx 33x for ~20% growth) is almost gone. SaaS was trading at a 6-8x premium to Hyperscalers for similar growth (33x versus 25x, similar ~20% earnings growth). The SaaSpocalypse scare has this merit: SaaS premium is largely gone.

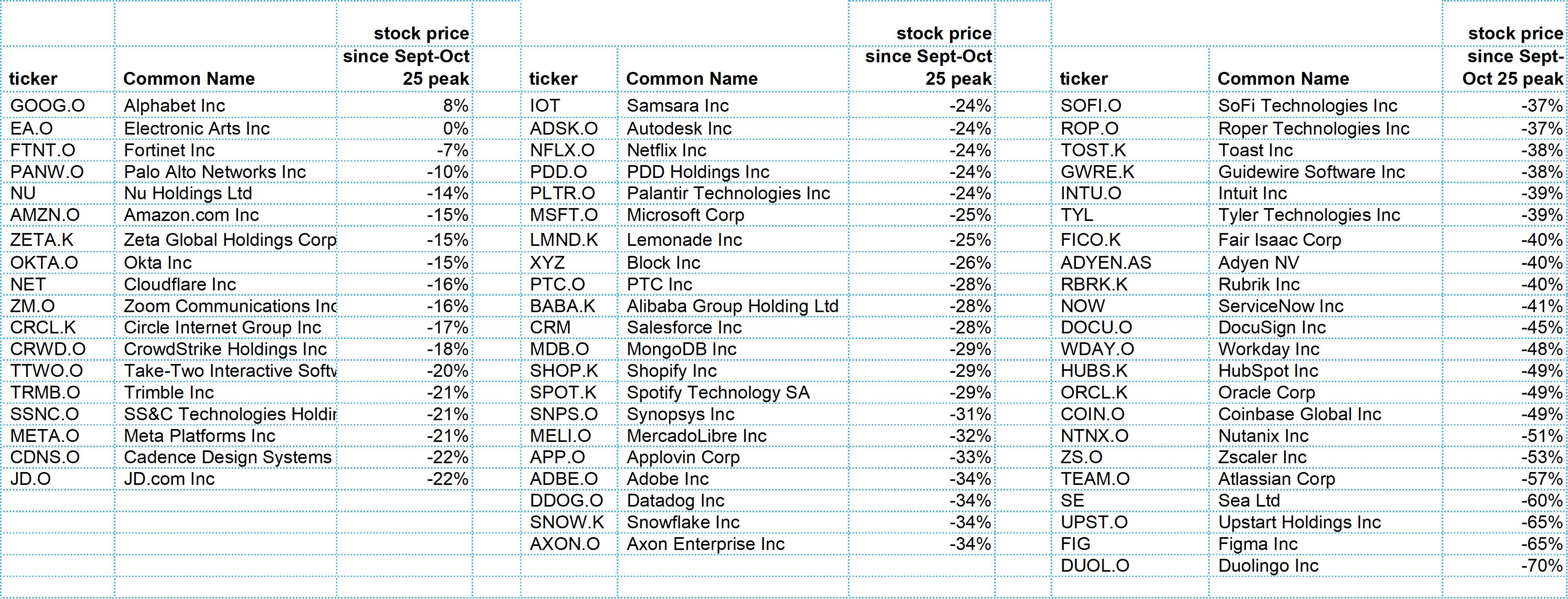

You can look at specific SaaS (and FinTech) names that are down 40-60% (list below, details at the end) and I guess that many will rebound.

My bias is to look at companies with real EBIT, real cash flows, lower volatility, ok valuations versus growth. For longer-horizon investors, I find it easier to buy Hyperscalers (better valuations/growth, less volatile) and a few profitable & growing FinTech names (Nu, SoFi). But again, today is not the day. Separate note coming.

Stock correction from the peak of Sept / Oct ’25 to Friday 13 March ’26:

Steepest correction: SaaS-Software aka IGV ETF or the SaaSpocalypse as you’ve read about. Same for Fintech, some of that driven by the crypto marketplaces (COIN).

eComm: almost as bad as SaaS and FinTech.

Hyperscalers: less bad. Almost ok, given the overall market.

If you want to look at the valuations, growth per stock, that’s the last table at the end. Stock performance from Sept / Oct ’25 peak to last Friday here:

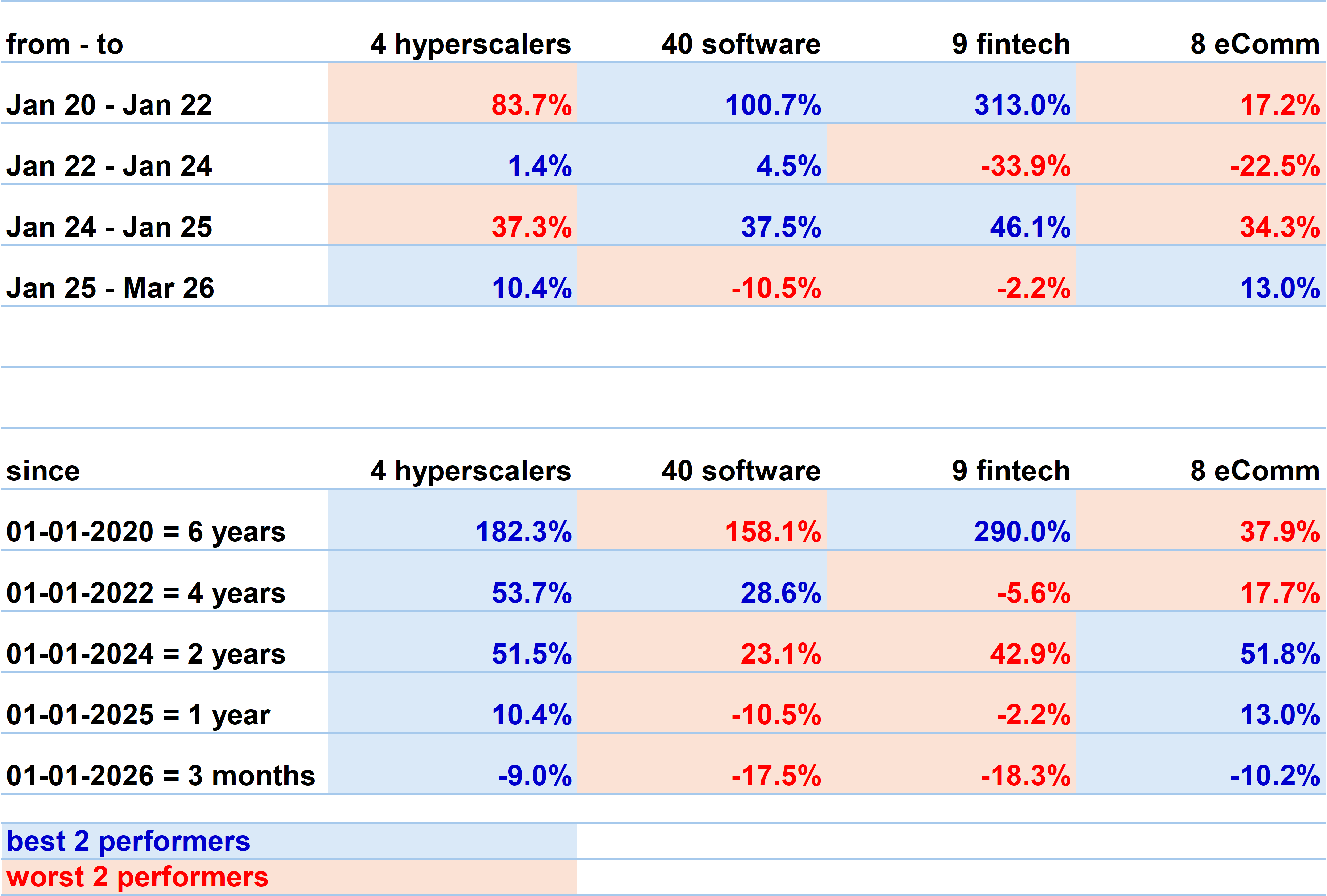

Most people I talk to – and most research I read – sort of assumes that newer sectors have higher growth, hence outperform. (Hyperscale is “old”, SaaS is not new, FinTech is new, some eComm in Emerging Markets is new Mercado Libre or Sea).

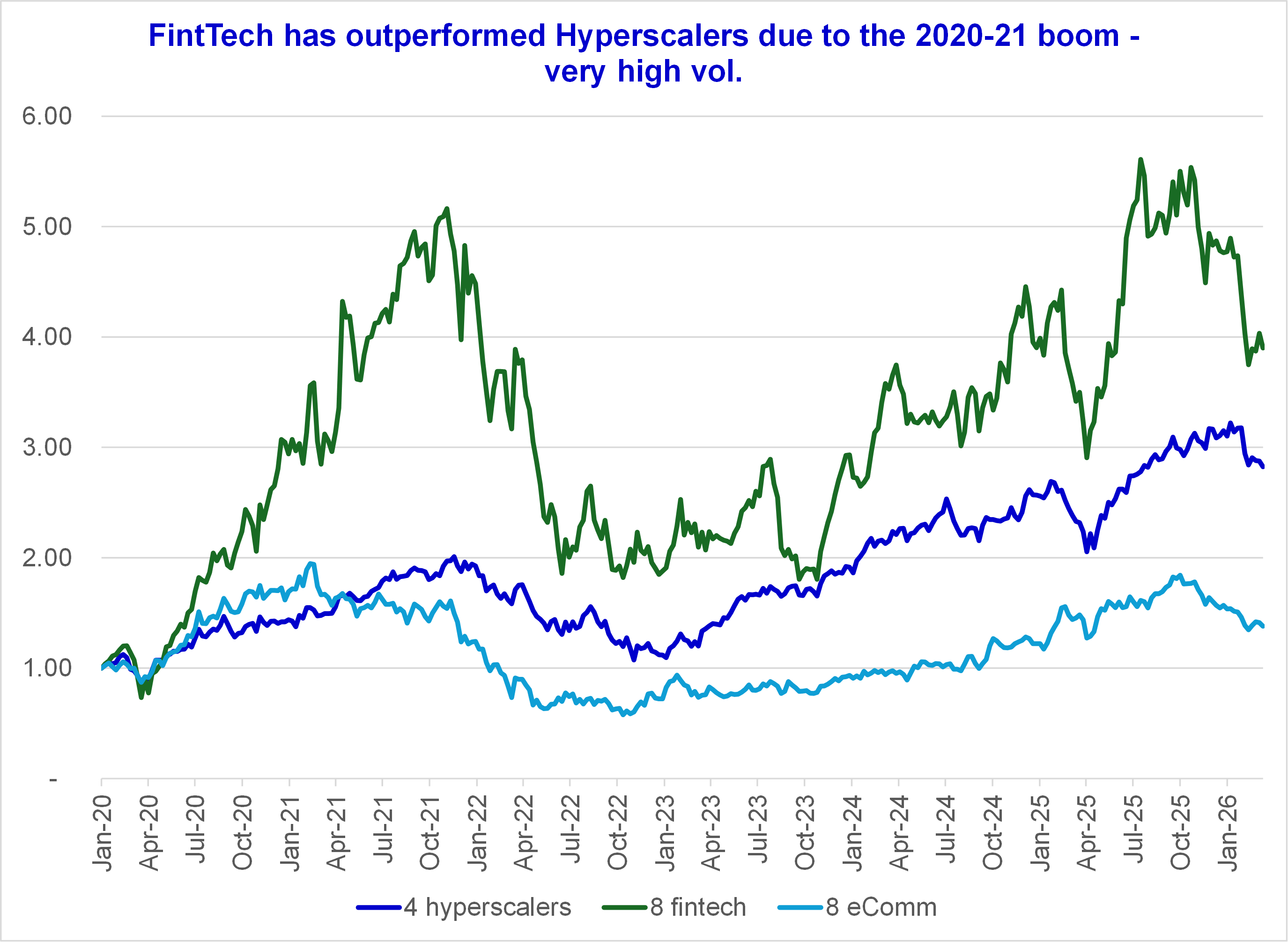

But no. Over different time frames, up to last Friday 13 March ’26, Hyperscalers consistently outperform. Not absolutely outperform, as Fintech or eComm had 1-2 periods of best outperformance. But if you’re a risk-adverse and lazy investor (i.e. that’s me), Hyperscalers have delivered the most consistent outperformance for the lowest volatility.

Stock performance by sector

Valuations versus growth (Consensus from Refinitiv / LSEG), major conclusions:

SaaS-Software is down the most but that’s derating from elevated valuations. Today, SaaS is still more expensive than Hyperscalers for similar growth. Not great. Besides, Hyperscalers have outperfortmed SaaS with lower volatility. Personally, that’s what I want.

FinTech is the only sector where growth > PE, i.e. PEG below 1x. If consensus is right, 28% growth trading at 21x looks pretty good. Finding the best stocks in this segment looks appealing. The chart below shows that FinTechers have outperformed Hyperscalers: that’s due to the 2020-22 massive outperformance, see table above. Besides, not the massive volatility of FinTech.

eCommerce? I struggle to find something positive to say: lowest earnings growth at high valuations, worst underperformance…

************************* PAYWALL