Hyperscalers: What is Consensus forecasting? Good or bad? how much Capex can they spend?

The conundrum is: how to value stocks with high earnings growth (17%) but increasing fixed costs and slim free cash flow?

This note explains what Consensus is forecasting for hyperscalers over 2026-28, ie the impact of large AI capex. Slightly higher revenue growth, large operating margins expansion, even higher increase in cash flow from operations. Despite a sharp increase in depreciations, hyperscalers will generate ~17% net income Cagr.

The point of debate is capex. Is capex growth slowing down after 2026, is 2026 the peak year for capex/revenue? My view is that capex growth will slowdown but a lot less than Consensus expects.

The conundrum is: how to value stocks with high earnings growth (17%) but increasing fixed costs and slim free cash flow?

On Monday, I reviewed hyperscalers financials to measure the impact of higher Capex (driven by AI) on revenues / profits. 1) operating margins and cash from ops are increasing, 2) free cash flow is largely positive 3) the concern is declining asset turns prefiguring lower valuations. https://techstock01.substack.com/p/hyperscalers-is-ai-capex-too-high

Today: Consensus forecasts to 2028, are they credible, good or bad? Yes credible, yes good, but Capex is probably underestimated. Its gonna be a balance of higher growth, expanding margins versus thin free cash flow.

Next this week: valuations, hyperscalers versus Software (IGV), versus FinTech (FINX)

Next next: on the 2 dumb & popular theories: GPU depreciation time versus annual new GPU launch cadence, Software will be dummified away by AI code automation.

What is Consensus forecasting?

All data below is either reported (to Dec 2025), either Consensus from LSEG aka Refinitif. All firms have a Dec year-end, except Microsoft with a June year-end. 2025 means FY 25 for all firms.

Revenue growth over 2026-28: slightly higher than previous years

Past 4 years revenue Cagr 13.3%

Next 3 years revenue Cagr 14.2% so that’s a small acceleration

Small acceleration for AMZN

a significant acceleration for GOOG and I think that’s the only thing noticeable here

Small slowdown for META and MSFT.

As we’re going to think about AI revenue growth or how AI accelerates growth or expands margins, we have to remember this:

The core revenue growth of the hyperscalers might be slowing down significantly. Certainly, Amazon’s eCommerce won’t increase at 20% Cagr. Most likely, core Microsoft products like Windows PC / Server, Office 365 won’t increase at 20% Cagr.

We have to think about AI revenues as incremental revenues, i.e. new products that provide a higher level of functionality, automation and productivity. As such, we should think about AI’s future growth as an analog to Cloud revenues.

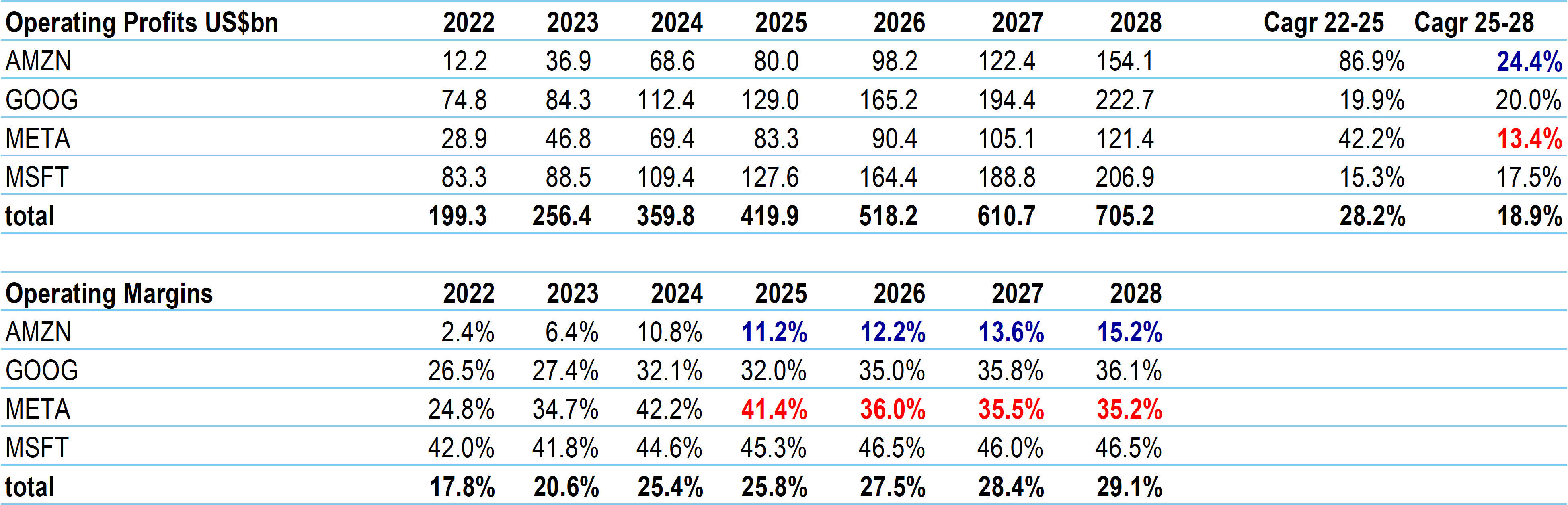

Important #1: large operating margins expansion despite Depreciation increasing

Consensus forecasts that:

Amazon OPM will continue on its stunning expansion trajectory. Margins to increase by 400bpd. Best performer. How possible? eCommerce or total Commerce (only store, physical, 3rd party) revenues are growing at ~8% and generate ~6% OPM. AWS revenues are growing at ~20% and generate ~35% OPM.

Google is 2nd best performer. Margins to increase by 400bps but from a much higher level than Amazon. Google’s revenues are made of core services (search, ads, youtube) at 85% of revenues and operating margins are increasing steadily (2022 33%, 2025 41%) and Cloud at 15% of revenues, growing faster but margins dilutive – becoming less margins dilutive (2002 -7%, 2025 24%).

and Microsoft: slightly up

Meta: large decline. Why is that? Because Depreciation is increasing faster than for others (see in Depreciation section below).

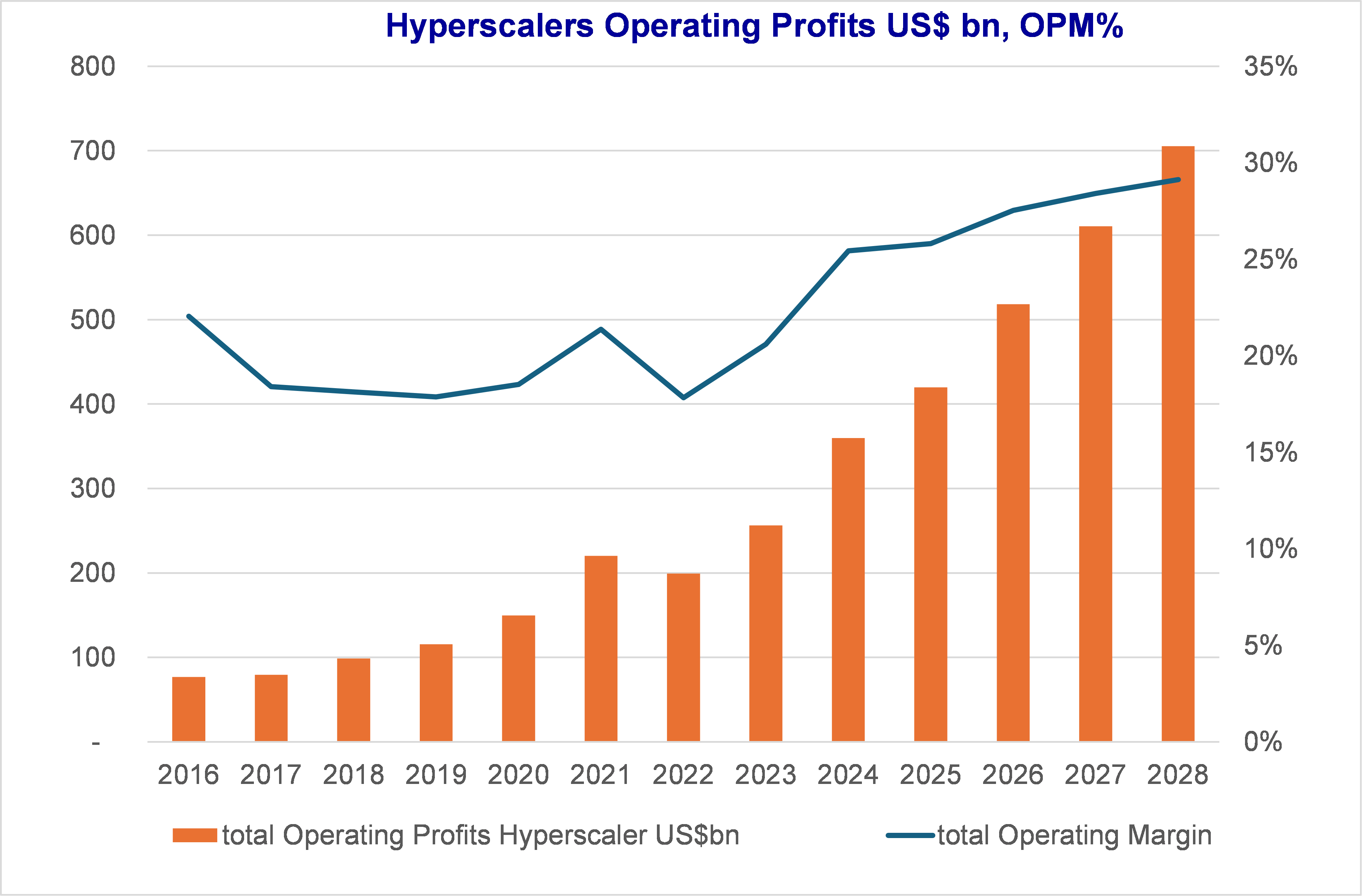

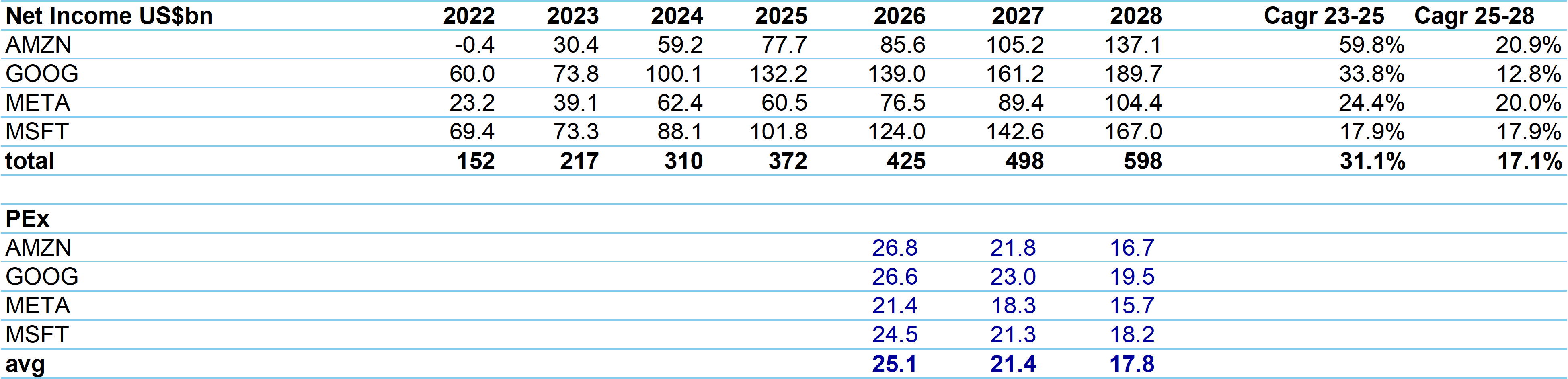

In aggregate, hyperscalers’ OPM will increase from 25.8% in 2025 to 29.1% in 2028. 330 bps in OPM expansion is a big big number considering:

The size of these firms

OPM is already high in 2025 at 25.8%

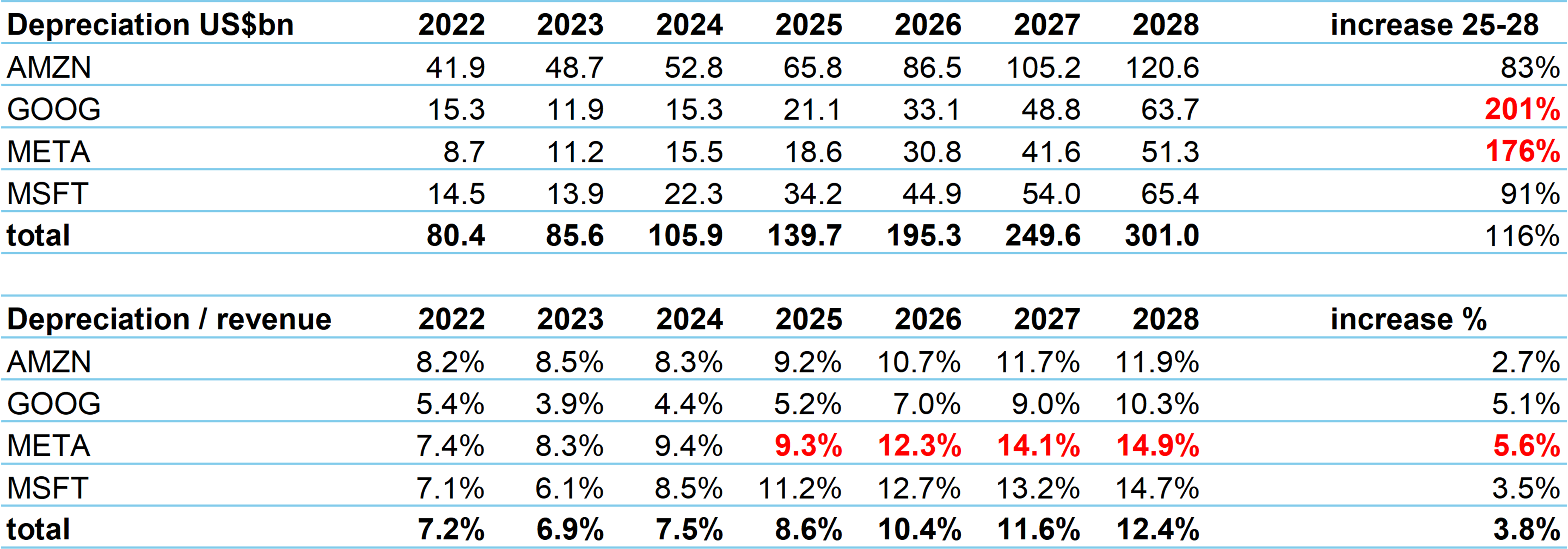

Depreciation

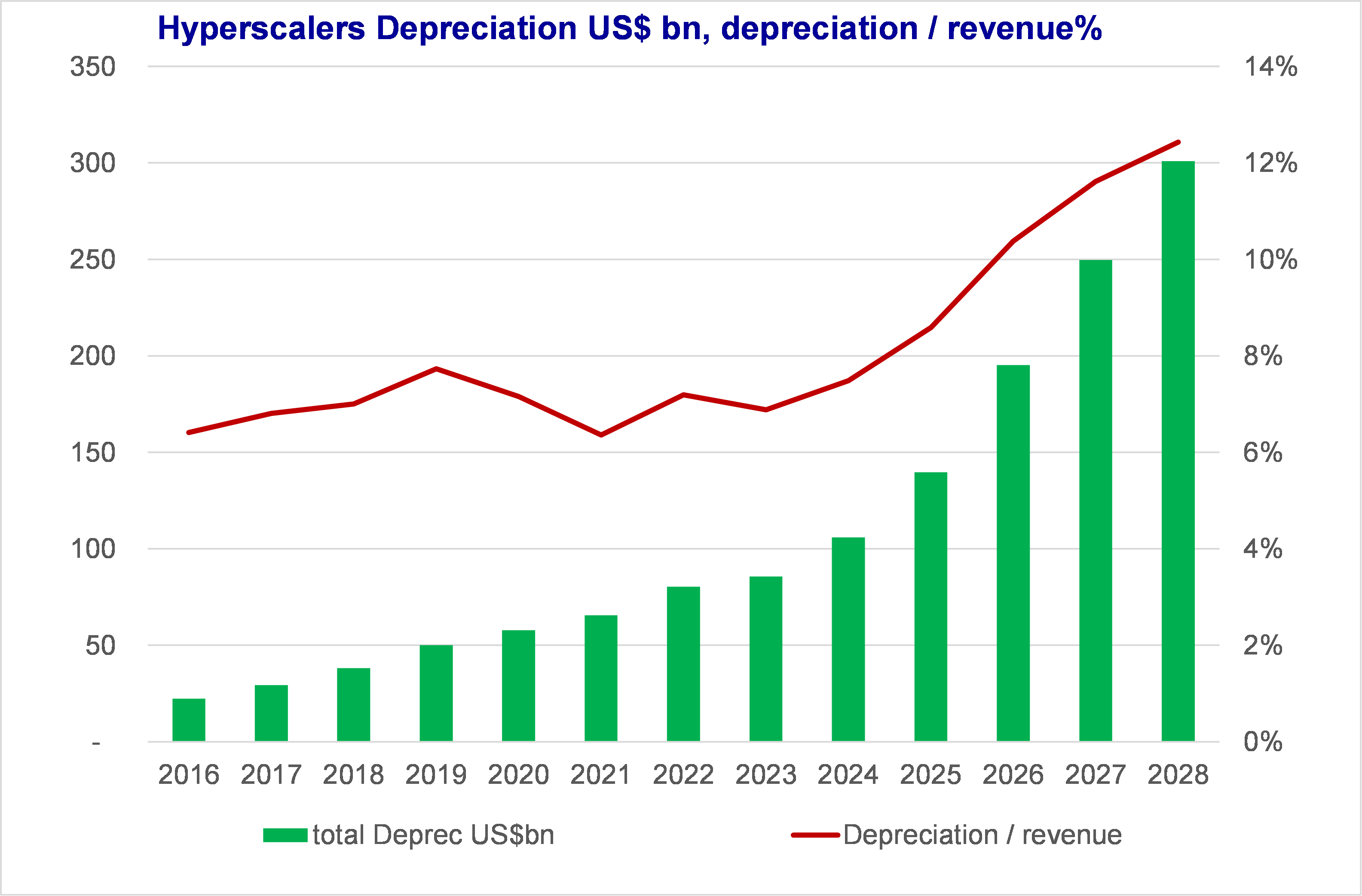

The OPM expansion is even more significant as Depreciation will increase from 8.6% of revenues in 2025 to 12.4% in 2028. The mechanics of this are:

Much higher Capex with AI investments

Longer depreciation period, let’s say on average increased from 4.5 years to 6 years

Higher capex * longer depreciation => still very big increase in Depreciation nevertheless

Revenue growth mitigates the Depreciation $-increase into a smaller %-increase

Note that Meta will see the largest increase in Depreciation / Revenue, explaining the wobbling OPM above.

Note that Google is not doing much better than Meta but it’s revenue growth will accelerate more, ie a smaller impact in %-revenue terms.

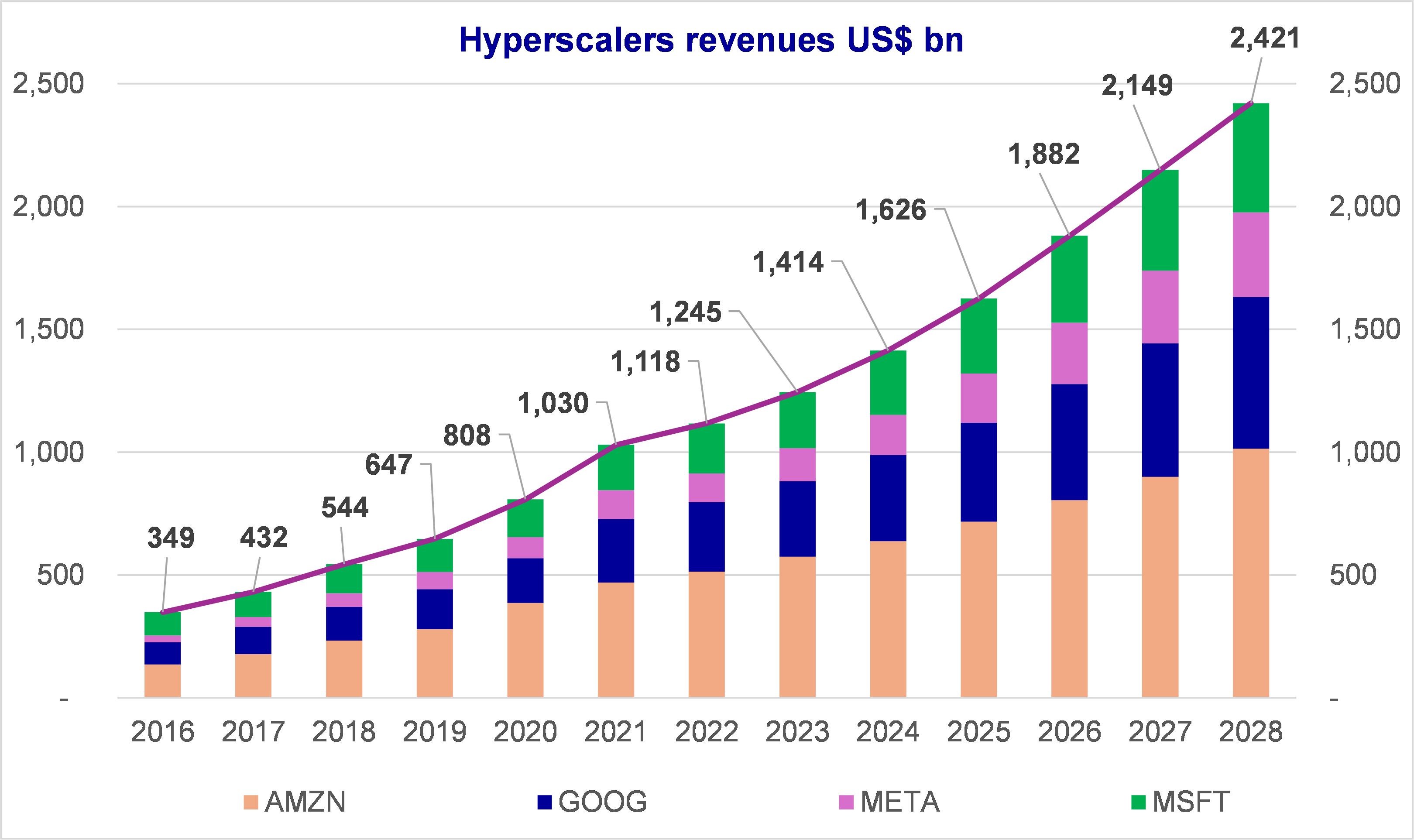

Amazon and Microsoft have smaller increases, and that’s because of a bigger base. For Amazon there is the large base of box-moving PP&E (eCommerce logistics). For Microsoft, well it’s just a much bigger Cloud (in Calendar ’25: MSFT $190bn, AWS 129bn, GOOG 59bn).

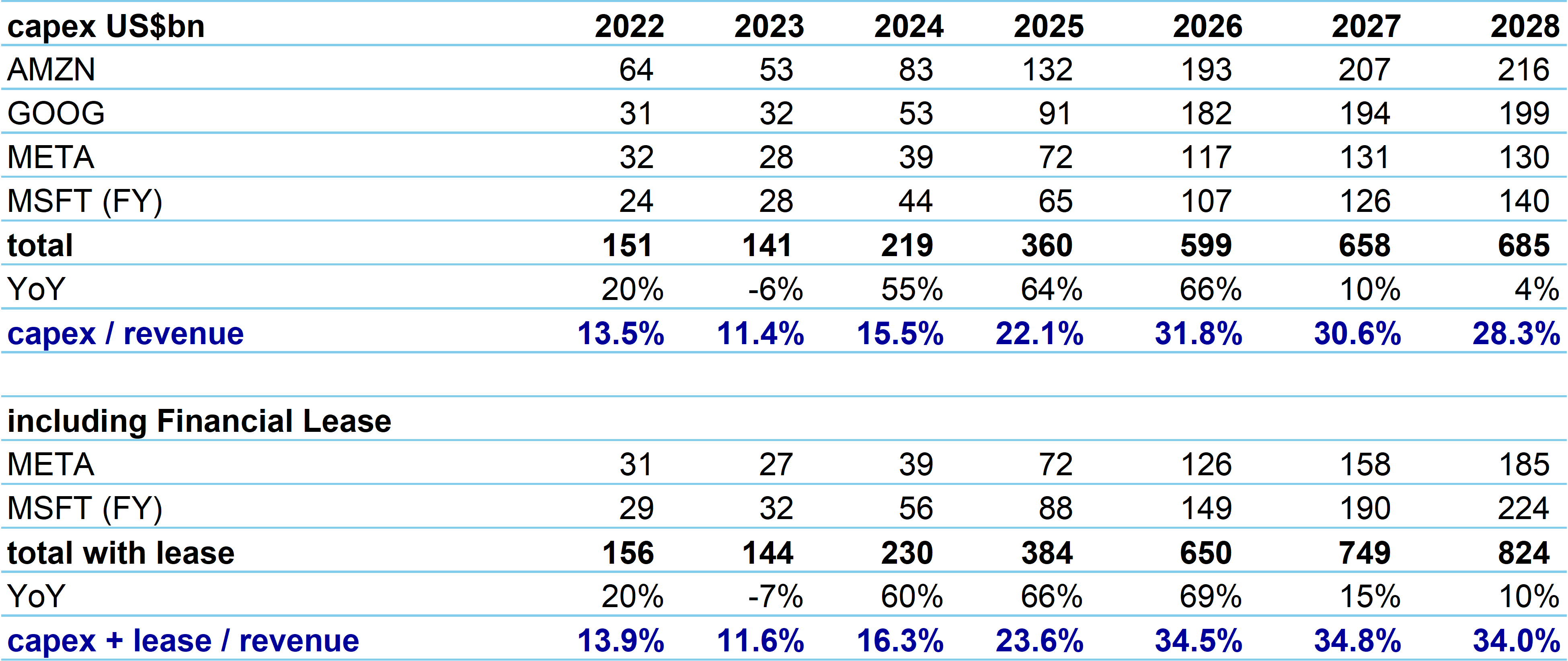

How much Capex?

First, we have a technical bug to highlight.

Capex is a cash flow item: money spent on equipment that you own on your balance sheet.

However, Meta and Microsoft also lease equipment (financial lease, hence financial expenses instead of depreciation). They report that number as “total Capex”: Capex + Financial Lease. This is closer to the actual money spent (and going to Nvidia for example) but this is not what we should consider impacting margins and free cash flows.

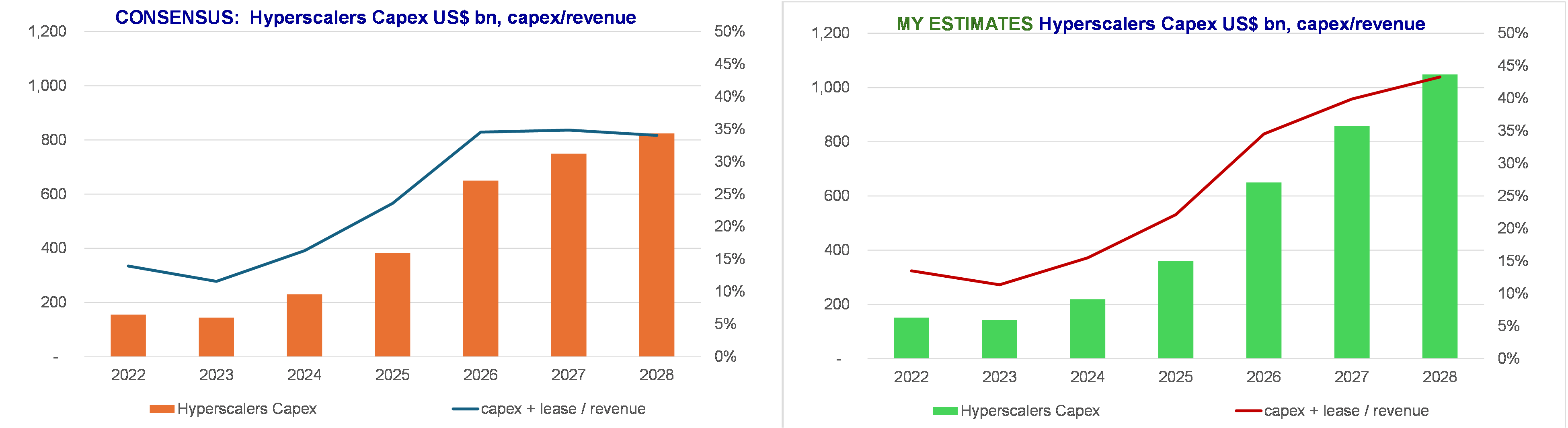

I mention this because the table below shows 2026 total Capex = $599bn. You might remember reading that 2026 Capex is $650bn. $650 includes Financial Lease.

Note the blue lines above (capex / revenue and capex + lease / revenue), I’ll get back to this.

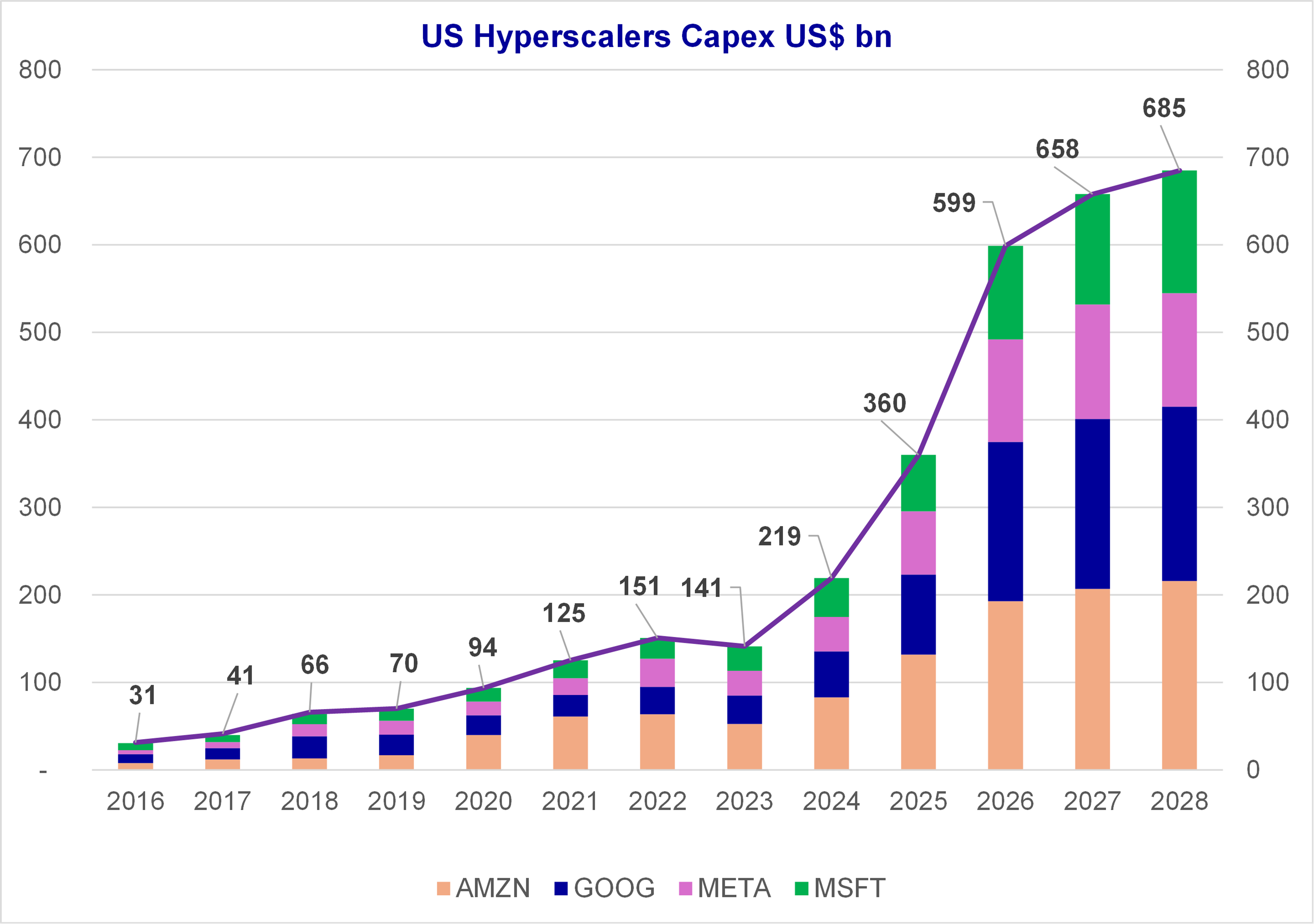

So, this is what we’re looking at for total Capex:

As you can see, Consensus forecasts that Capex is reaching a sort of plateau, or increasing very slowly from 2027 – after 3 years of explosive growth in 2024-25-26.

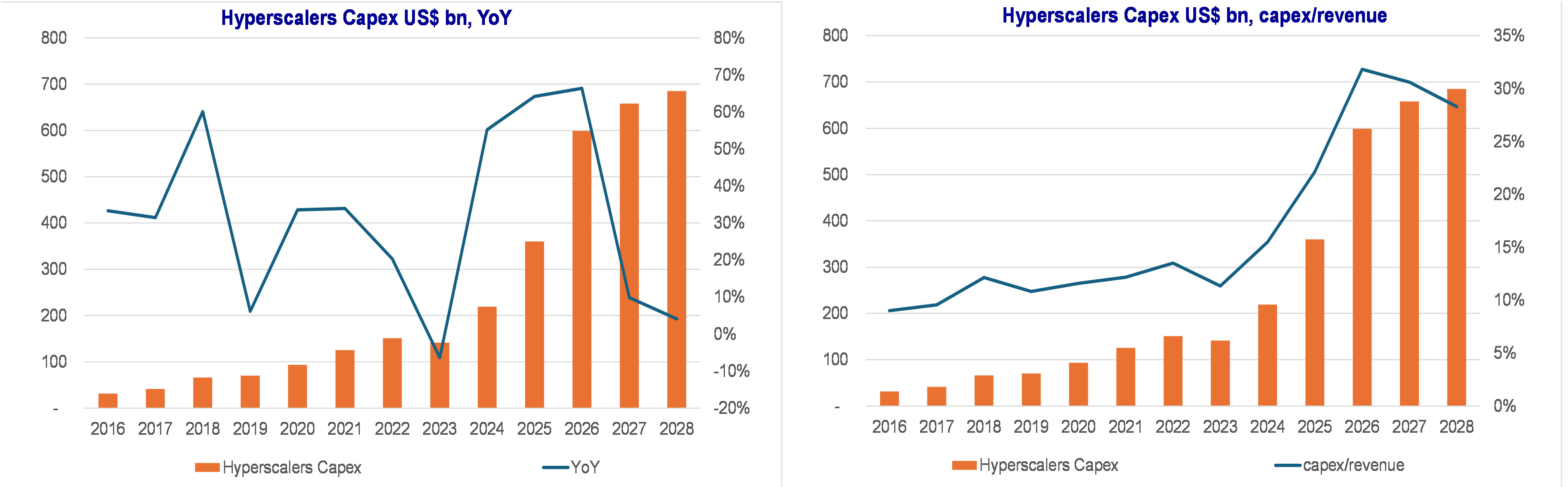

2 charts below:

Capex growth slows down to 10% and below from 2027

Capex intensity (capex / revenue) peaks in 2026 at 32% and either declines slowly or is flat (blue lines in table above). In any case, Consensus cannot conceive that asset-light hyperscalers are becoming aluminium smelting or semicon foundry type of companies: low PP&E turns, high capex/revenue. That’s what I explained on Monday 9 March 26 here: https://techstock01.substack.com/p/hyperscalers-is-ai-capex-too-high

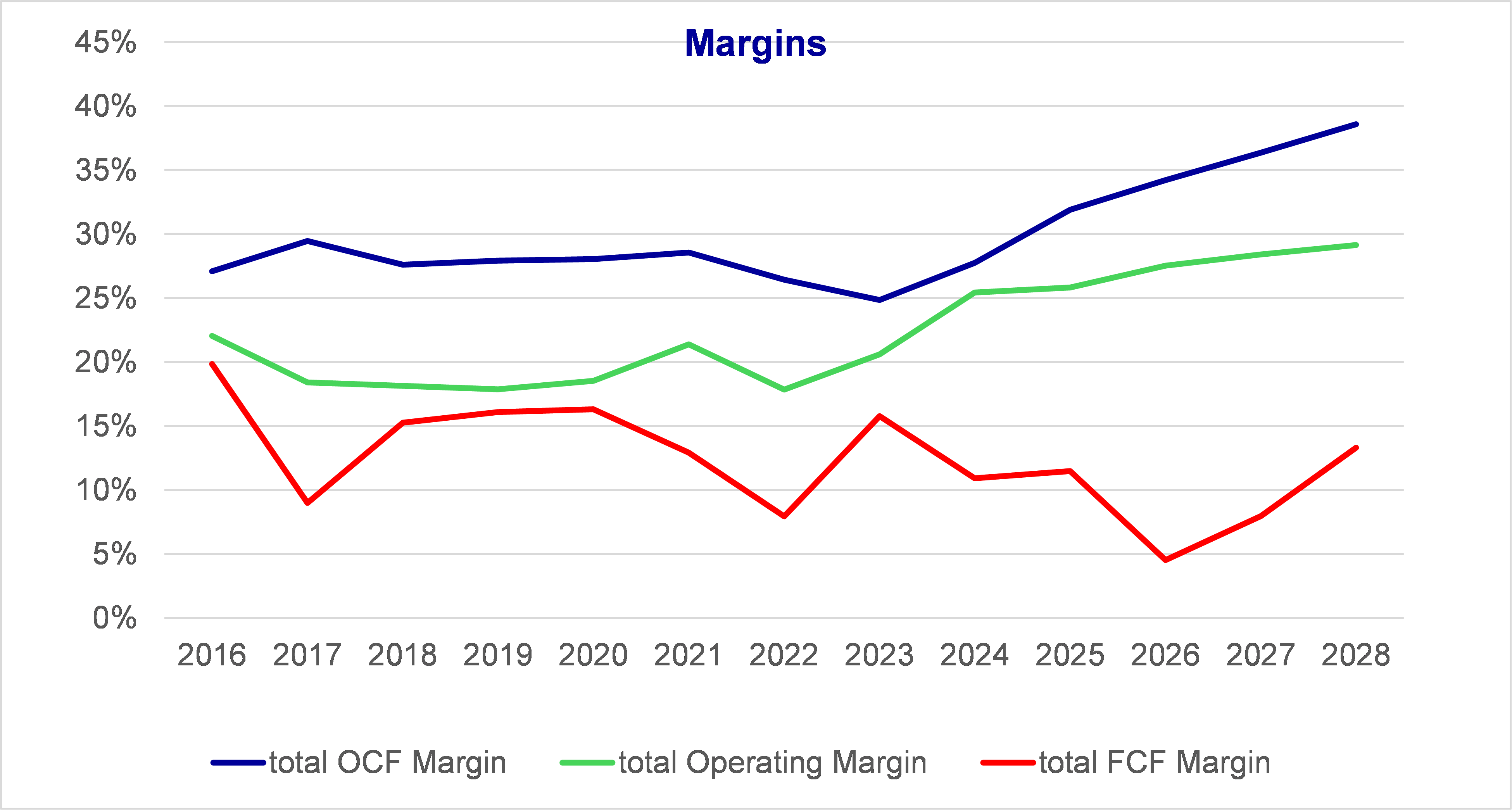

Putting all this together: this is perfect!

Putting all the pieces together:

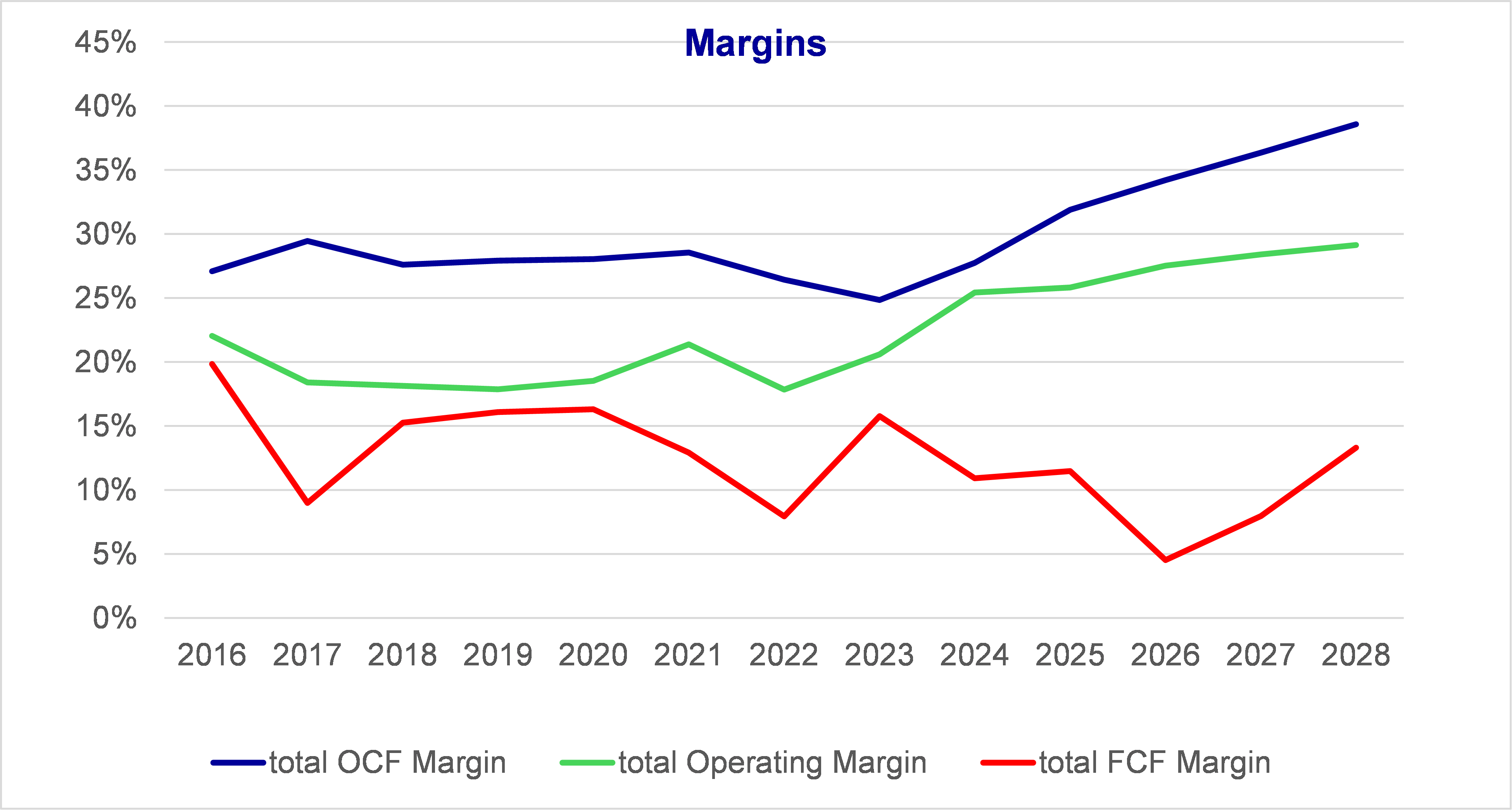

Despite higher Depreciation, Operating Margins go up

Operating Cash Flow OCF increases even more (as we add back higher Depreciation to Operating Profit, to simplify)

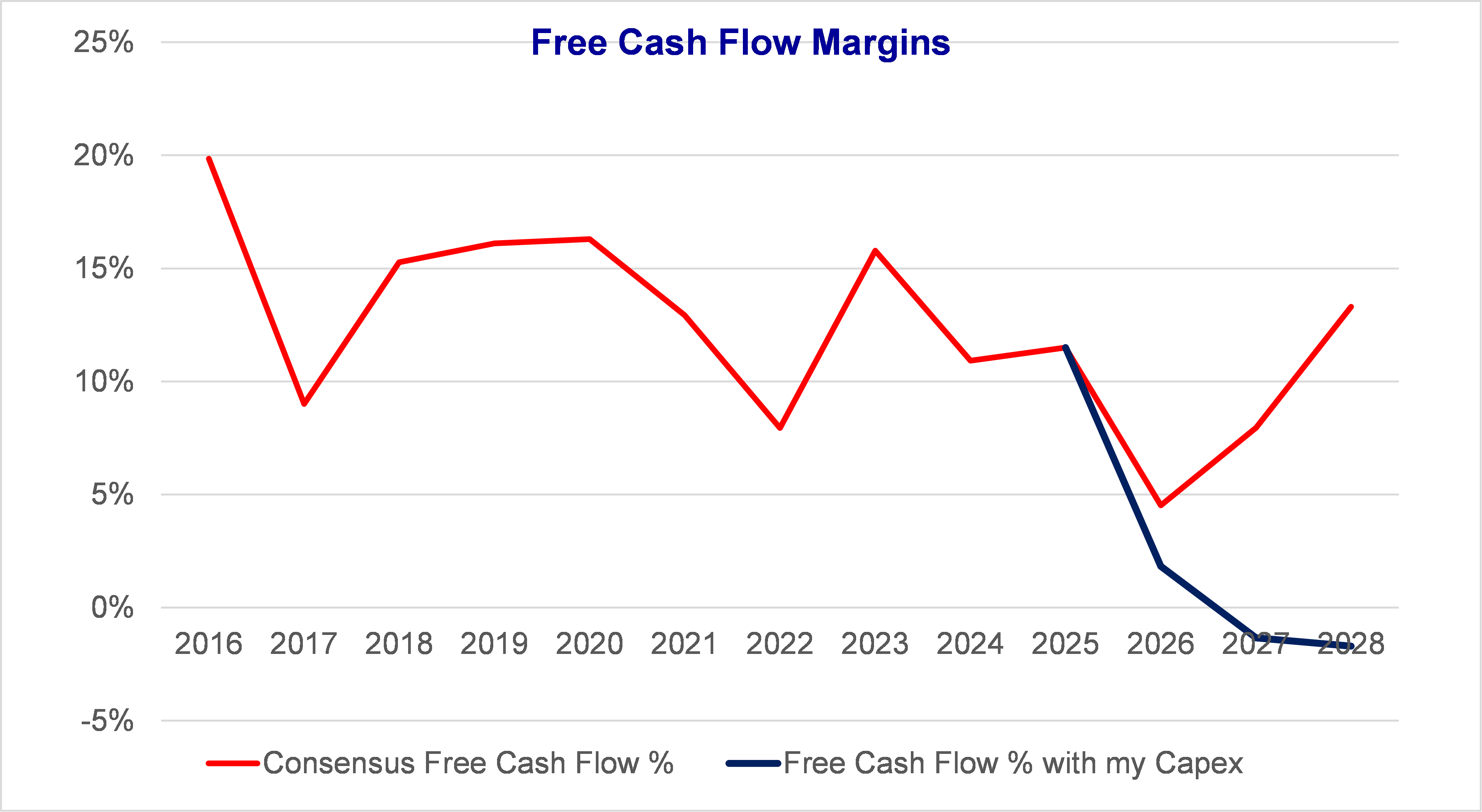

Capex plateaus from 2026, Free Cash Flows recover to ~13% of revenues in 2028. Note that even in the Capex boom years (2024-25-26), Free Cash Flows remain nicely positive.

What’s not to like here?

Final step regarding Consensus: this is net income forecasts and subsequently Price / Earnings ratios: 17% earnings growth Cagr, 21x next year earnings, PEG of 1.25.

This looks like perfect forecasts – or perfect outcomes. Increasing Capex generates higher margins (operating and operating cash), free cash flow recovers, firms make a lot of profits. Growth is consistent with valuations.

Important #2: I don’t believe that capex growth will decline that quickly from 2027

I think that Consensus forecasts are in the ballpark (revenue growth, OPM expansion, sharp increase in Depreciation, Operating Cash Flow expanding faster than Operating Margins, Free Cash Flows always positive). I have done the reverse engineering on consensus to understand the calculations / assumptions and it’s all plausible, reasonable.

You should not look at Consensus as precise forecasts but as directional indicators. I think these indicators are directionally correct:

Revenue growth will increase a bit to 2028 (few new AI-products, more after 2028)

operating margins will increase a lot (ask Gemini: “what did Zuckerberg and Pichai say about AI increasing ad effectiveness?” )

Net-net large growth in operating profits

The Depreciation calculations are consistent (I have checked).

The Operating Cash Flow and Free Cash Flows calculations are consistent (I have checked).

But…

If you’ve looked at this for the past 3 years, you know that Consensus has consistently – and severely – underestimated Capex. That means underestimated / misunderstood why hyperscalers are investing so much on AI.

Indeed, that’s been over the past 3 years the core discomfort of many investors: a lot of Capex now, hope of higher profits later but when don’t know how to quantify that

The only possible answer to this is that hyperscalers are spending a lot more than Consensus expects because hyperscalers believe that AI’s future revenues / margins will be a lot higher than Consensus expects.

Either:

Hyperscalers are correct: AI will support new products, new companies, new wonderful things that will be very profitable and they need to keep spending. And you buy the stocks.

Hyperscalers are wrong, they’re over-investing on AI and ROI won’t be as good as they expect. And you short the stocks.

Important #3: capex growth will decline anyways

The 2 charts below show:

Left: Consensus Capex forecasts (including financial lease) and capex / revenue

Right: my estimates for the same

With my much higher capex, Free Cash Flow FCF becomes slightly negative at -1% -2% in 2027-28. The chart below shows Consensus forecasts in red, already mentioned above, and my FCF in dark blue.

I think that slightly negative FCF is tolerable for a couple of years. Debt levels are low. More off-balance sheet financing is possible with the likes of Oracle, Blue Owl, Blackrock, Crusoe Energy, and the independent Data Centers (Nebius, Core Weave). Other use of cash (dividends, buy backs) are smallish or... flexible.

On the other hand, I also do not think that the hyperscalers’ managements and shareholders have any appetite for prolonged negative Free Cash Flow, nor for high gearing levels.

What’s important here:

Capex growth will slow down, but not as fast as Consensus hopes. Nevertheless, slower growth. You have to worry about the impact on valuations for Nvidia, Broadcom, AMD, or any stock trading above 30x and facing slowing growth. Micron and TSMC are a lot cheaper.

Capex intensity will keep going up steeply till 2028. This will bring a lot of worries and discomfort for many investors = the usual concerns regarding unknown future revenues, margins, ROI, why so much money is spent?

Why higher Capex? 2 reasons:

The next 3 generations of chips (Nvidia Vera Rubin 2026, Rubin Ultra 2027, Feynman 2028 and for AMD MI450 2026, MI500 2027, MI550? 2028) will bring considerable increase in computing loads (bigger models, more data) and considerable decline in the cost per token. If you aren’t sure, ask Gemini “can you find Nvidia Jensen Huang quote regarding considerable decline in the cost computing per token”

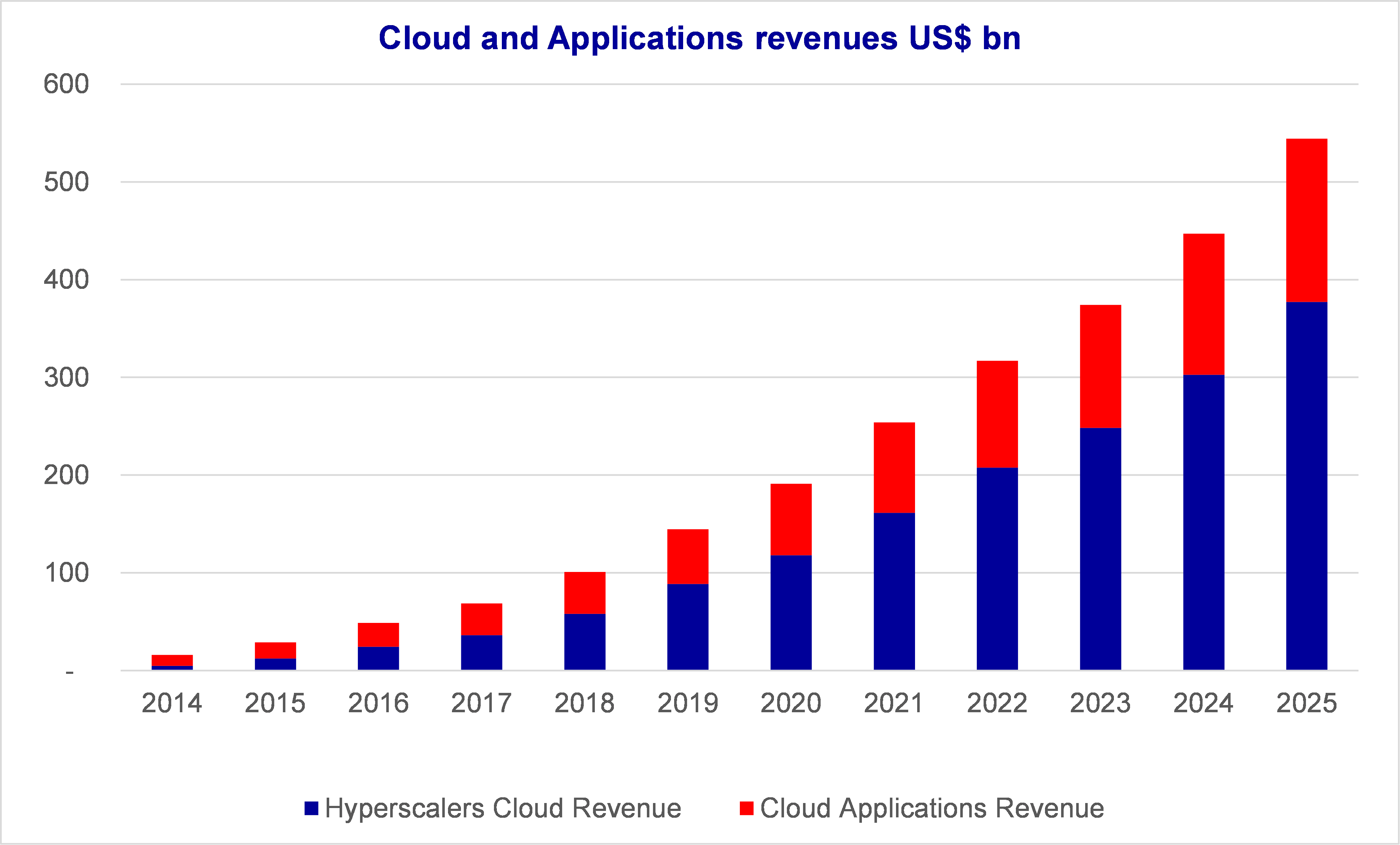

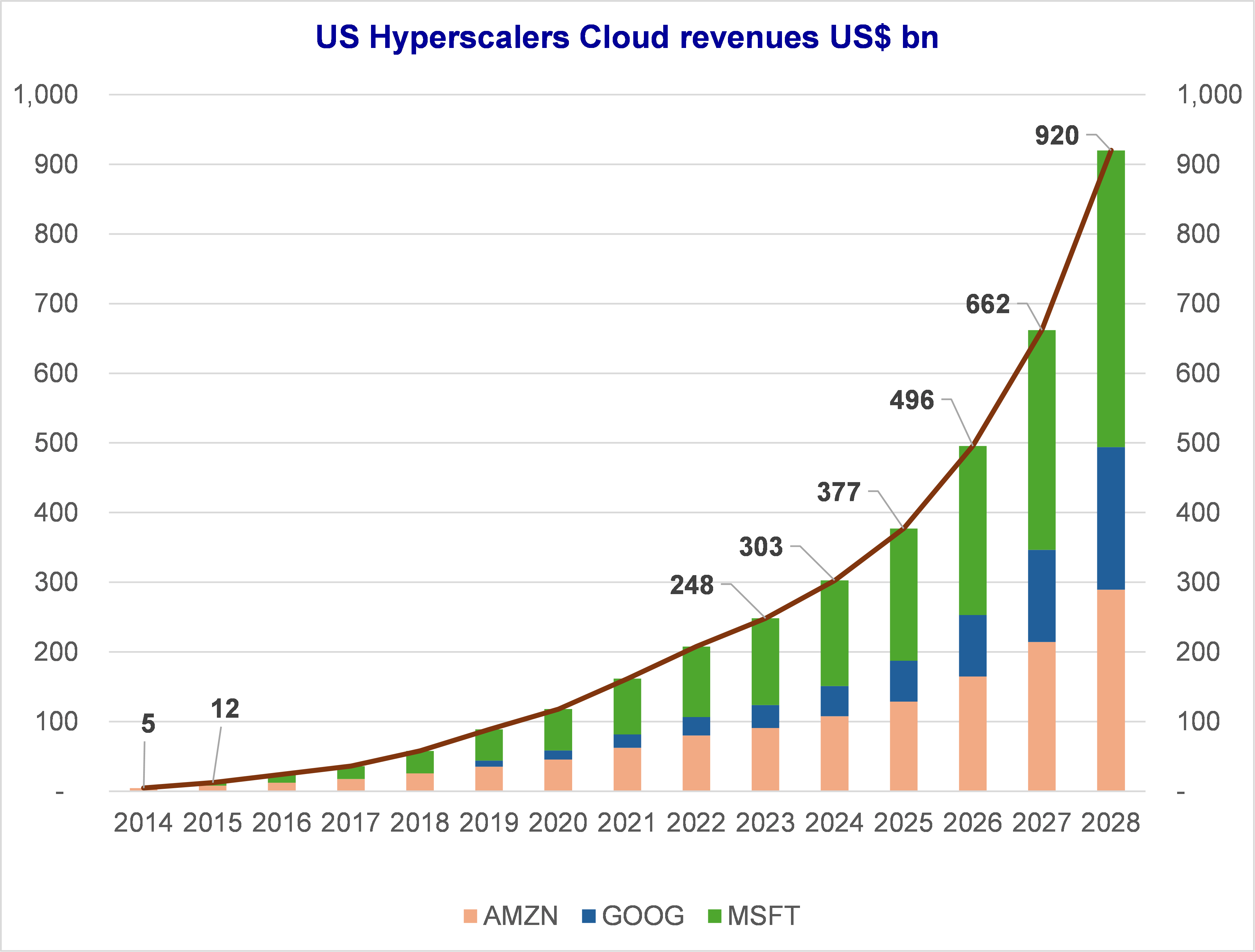

I can’t prove it to you, but my busy imagination says that AI tools will reaccelerate Cloud revenue growth in the ~35% Cagr range for the next 5 years. You can have a look above at the 3rd figure in this note. This means this kinda growth to 2028, chart below.

Then eventually the exponential development stage of AI models and applications will decline in the capex mix, much cheaper inference will become dominant, that’s where revenues should grow faster than capex. Maybe from 2028-29.

I am sure that you find this very interesting but it doesn’t change the way that you view the world. Either you’re onboard with Consensus – or with my even more bullish view – and you buy the stocks at the right valuations, soon. Or you still think that it makes no sense and you stay away.

The key here is to recognize that Software-led hypergrowth has already happened multiple times in Tech history:

From no enterprise software to $900bn revenue in 2025 (data from Gartner here, thru Statistica)

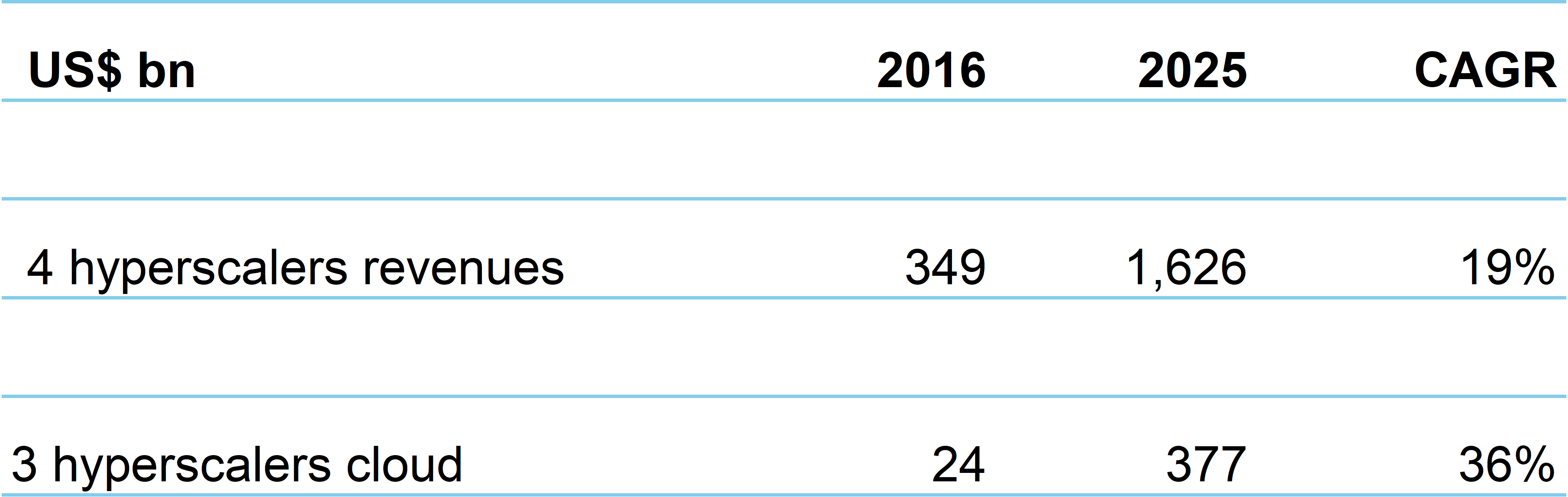

From no internet to hyperscalers $1.6tn revenue in 2025

From no cloud to hyperscalers’ cloud $377bn revenue in 2025

On top of which the Cloud-based app / content companies are built, another $166bn in revenues in 2025 (CRM, NOW, SNOW, DDOG, SPOT, NFLX, SHOP, etc etc)

AI will add another layer of Cloud revenues for hyperscalers, and a new generation of application companies (ex Palantir).

This chart below, and several charts above, highlight the hard choice that investors are facing. AI is back to 2015 on this chart below. Hyper growth is coming but you got to be patient, and you got to understand why software is eating the world. This piece is fun to read today - its 15 years old and yet, change a few words (software = AI, private market valuations = private debt) and you’ve got a good description of today.