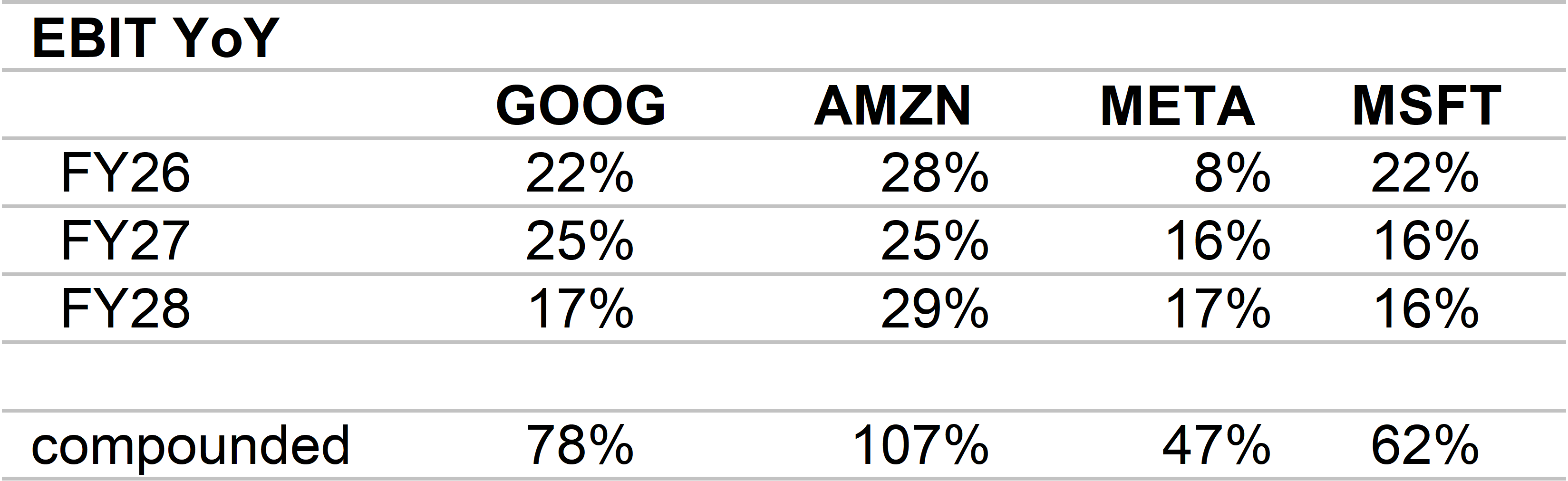

Hyperscalers: Consensus revisions and Valuations post earnings

Best growth stocks: GOOG and AMZN, which are also the highest valuations at 27x next year.

Alphabet aka Google: some room for Consensus to increase, Cloud growth * margins expansion are accelerating. Valuations are reasonable at 27x next year EPS for 18% EBIT Cagr over ’25-28.

Amazon: highest growth at 27% EBIT Cagr over ’25-28, same valuations as GOOG: 27x next year. Relative to GOOG, you probably apply a valuation discount to eCommerce, similar for Cloud growth and I’m not sure there’s a case for AMZN to trade on higher multiple than GOOG.

There is a large disconnect versus Walmart or Caterpillar trading at higher valuations (36-40x) for lower growth. Or AMAT, ASML trading at ~32x for lower growth.

Meta commands the lowest growth forecasts, and the lowest valuations. Low growth really reflects confusing strategy, changing narratives, high Capex but lower visible growth. We could argue that low valuations are attractive – but I think we need to see a growth inflection first.

Microsoft is probably the best “value” stock: 21x next year earnings, 18% EBIT CAGR but we need to see Cloud margins improving. The latest Capex guidance ($110bn increased to 190bn) puts that into doubts for ’26-27.

The table below shows EBIT (Operating Profit), growth and revisions.

I prefer EBIT rather than EPS because below EBIT we have very large “non-cash” investment gains (ie GOOG investments in Anthropic, Space X) and large fluctuations in tax rates (ie META). Let’s look at the core business.

Growth means: EBIT growth YoY.

Revision means: by how much have forecasts increased (or declined) in the last month? This compares EBIT before earnings and after earnings, reflecting how much “good news” (or “bad news”) the companies have given us.

You’ll also find valuation charts.

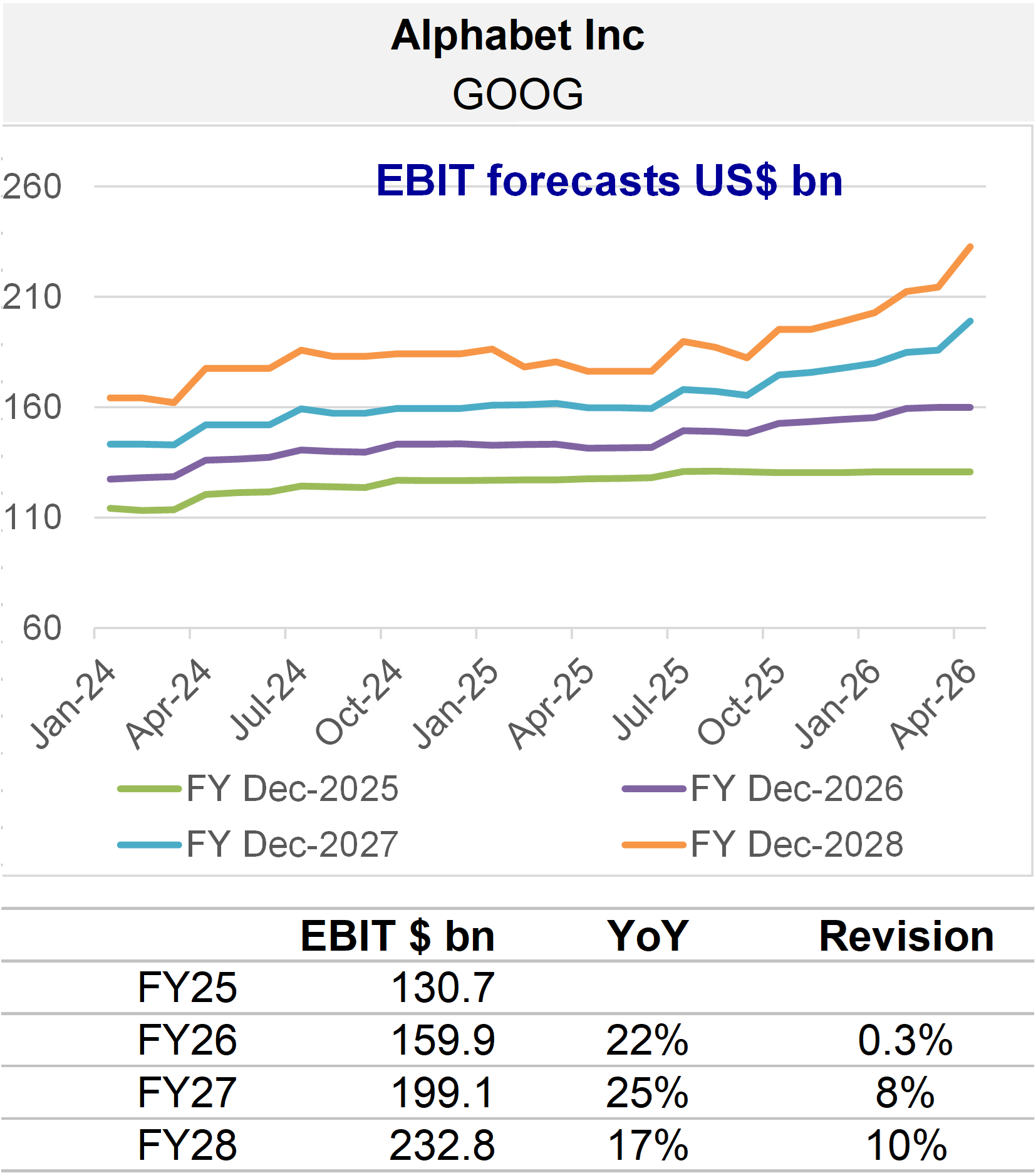

Alphabet – GOOG

EBIT Growth

2026: 22% YoY

2027: 25%

2028: 17%

That’s a lot of growth. It means that EBIT will increase by ~80% from 2025 to 2028. I think that’s in the ballpark – but could be higher for 2028.

These high forecasts mean that Consensus has acknowledged the acceleration in Cloud growth and Margins. Also means that there is low “AI Capex trust” issue for Google. The company spends a lot, delivers higher growth, Consensus understands.

Revisions

2026: 0.3% Reason 1) we have seen Cloud growth and Margins accelerate for several quarters, so that’s in the forecasts already and Reason 2) the company does a good job explaining why D&A, Opex, R&D do increase a bit faster than revenues but no drama, it’s mostly timing differences.

2027: 8%

2028: 10%

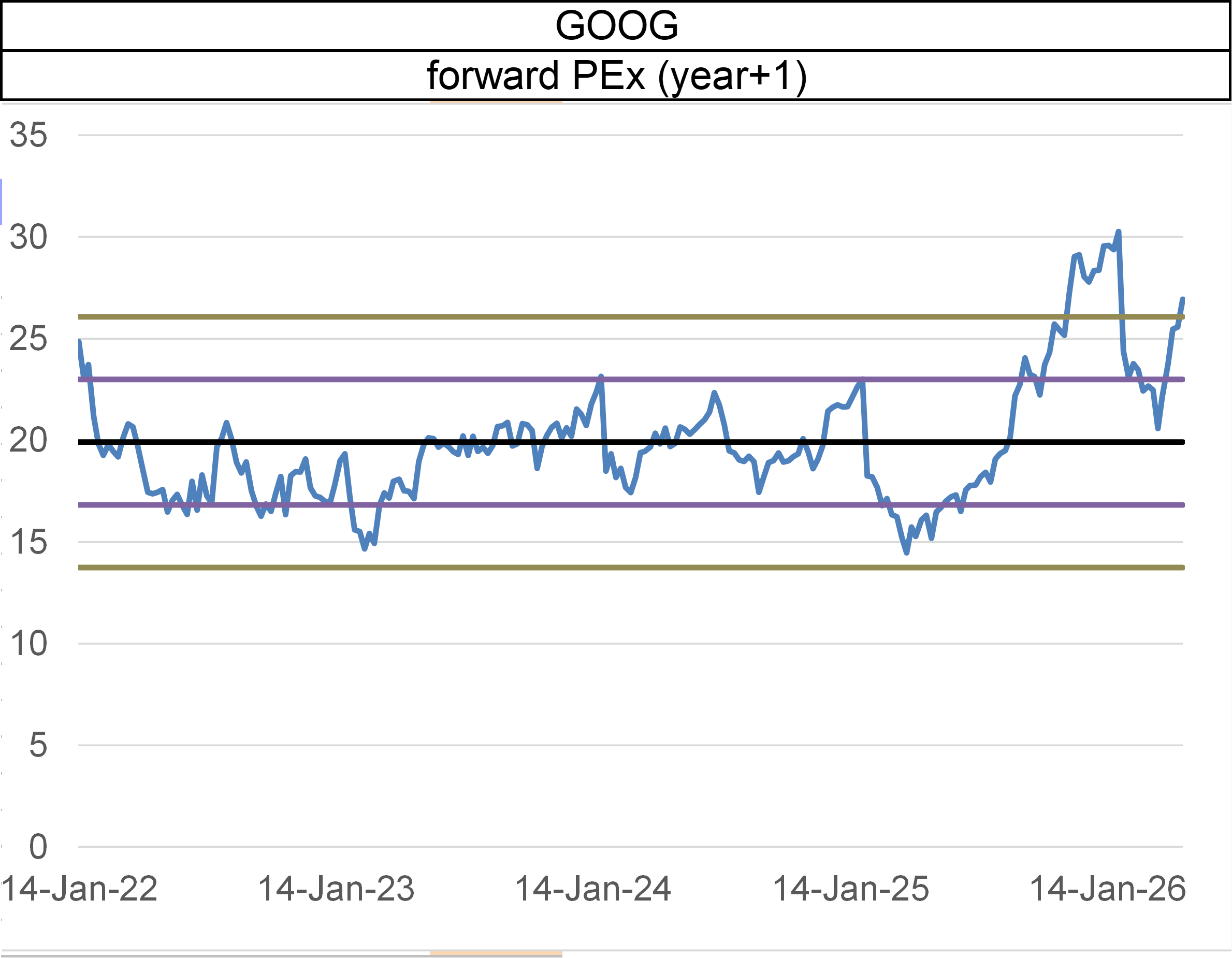

Valuations

GOOG used to be trading on the lowest PE multiple (same for META). The narrative was: search-based advertising is sort of saturated, it’s vulnerable to AI doing Search easily (ie 2 years ago OpenAI was supposed to become your search engine), GOOG was the very small 3rd Cloud provider with revenue half that of AWS, a third that of MSFT.

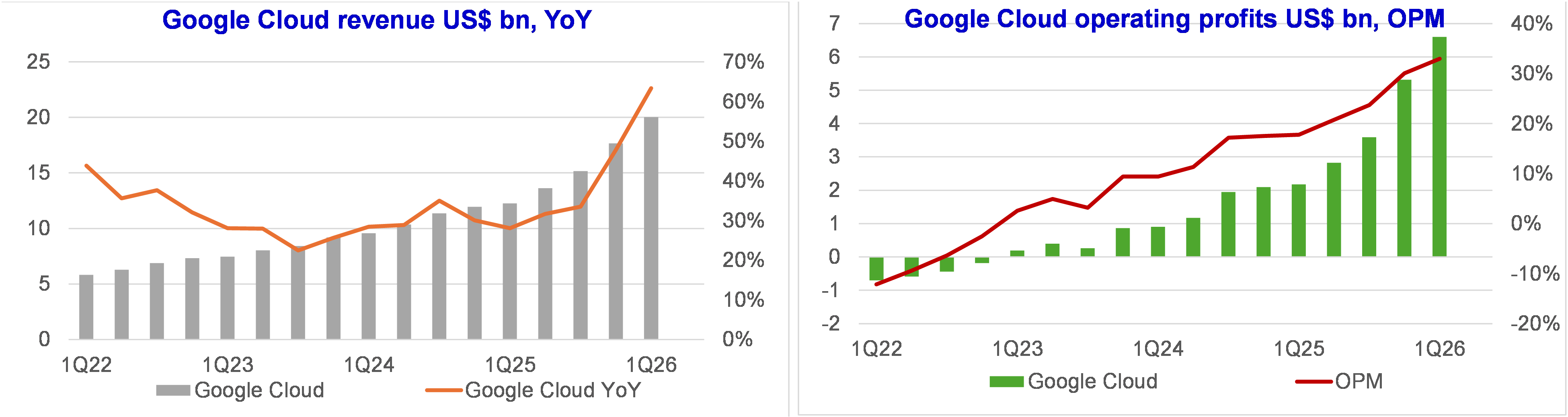

Honestly, I think that GOOG is still today the stock that has the best potential for re-rating:

(referring to the 1st table in this report): forecast growth is lower than for AMZN but I think too low given the charts just above: Google Cloud growth is stunning at ~60%, operating margins is “only” at 33% versus AWS 38%, MSFT Cloud 40%

If you’re an Enterprise user of Google Cloud and related products, the breadth and quality of the offerings is improving regularly, the integration of AI tools works a lot better than Microsoft (CoPilot), the management tools (from security, access, data flow controls) are very simple to use – and it’s cheap. That’s probably not relevant for a multinational firm with 100k employees but I think appealing for SME. This means that Google Cloud is building a smart niche with small overlap against Microsoft.

PAYWALL BELOW