Google: very impressive. Higher Capex, higher growth & margins

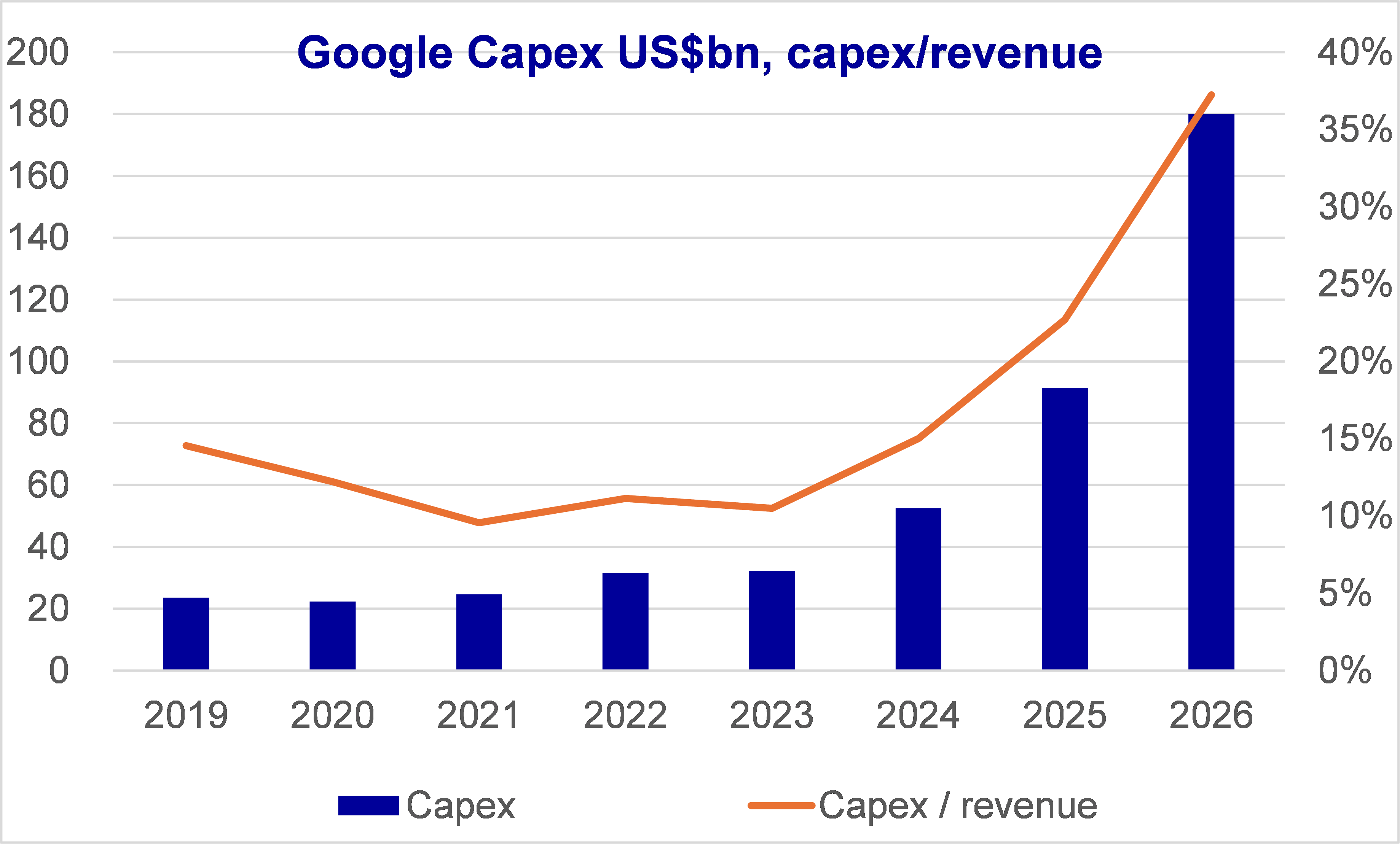

Sharp increase in 2026 Capex suggests accelerating growth & margins in 2026-27

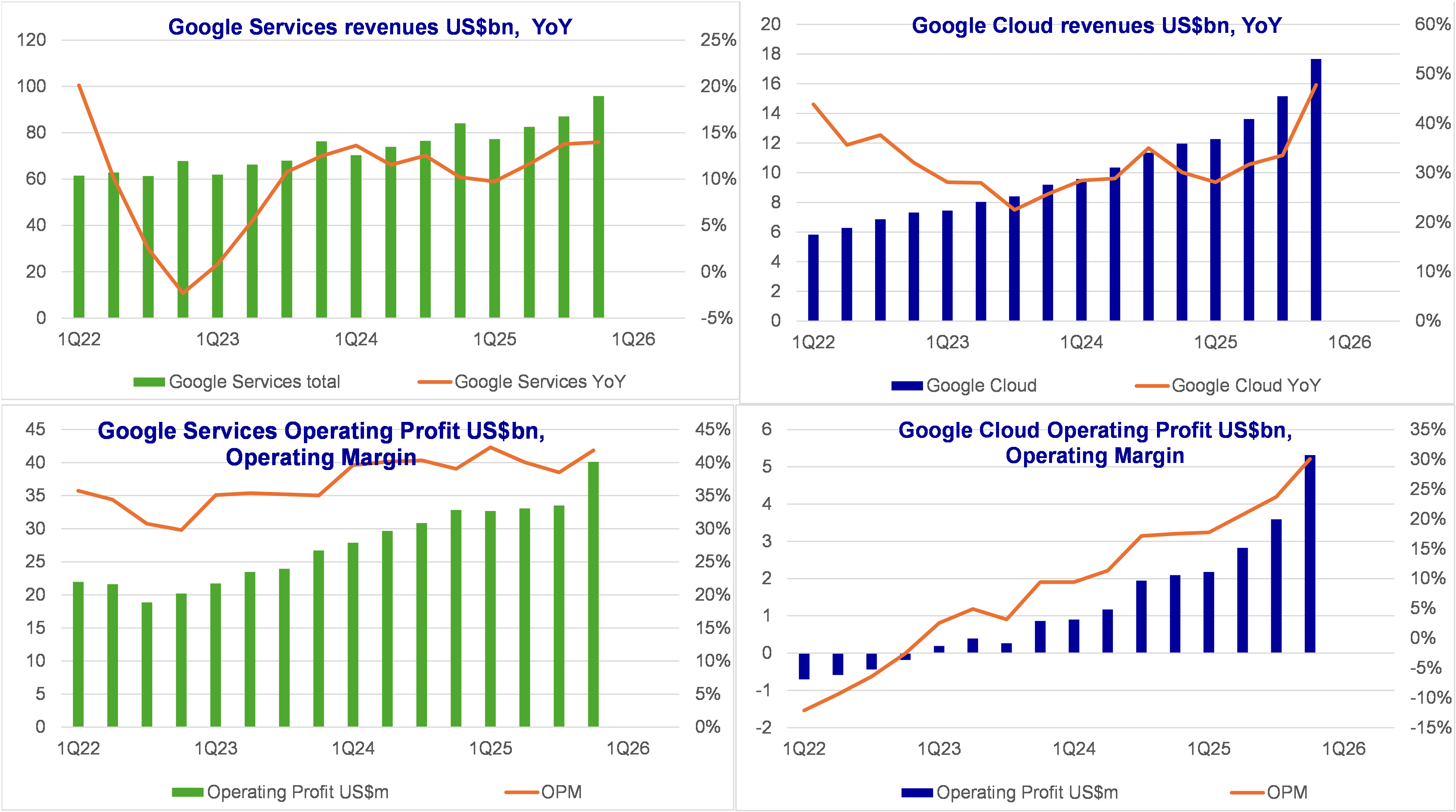

AI investments are bearing fruits. Revenue growth is accelerating, margins moving up.

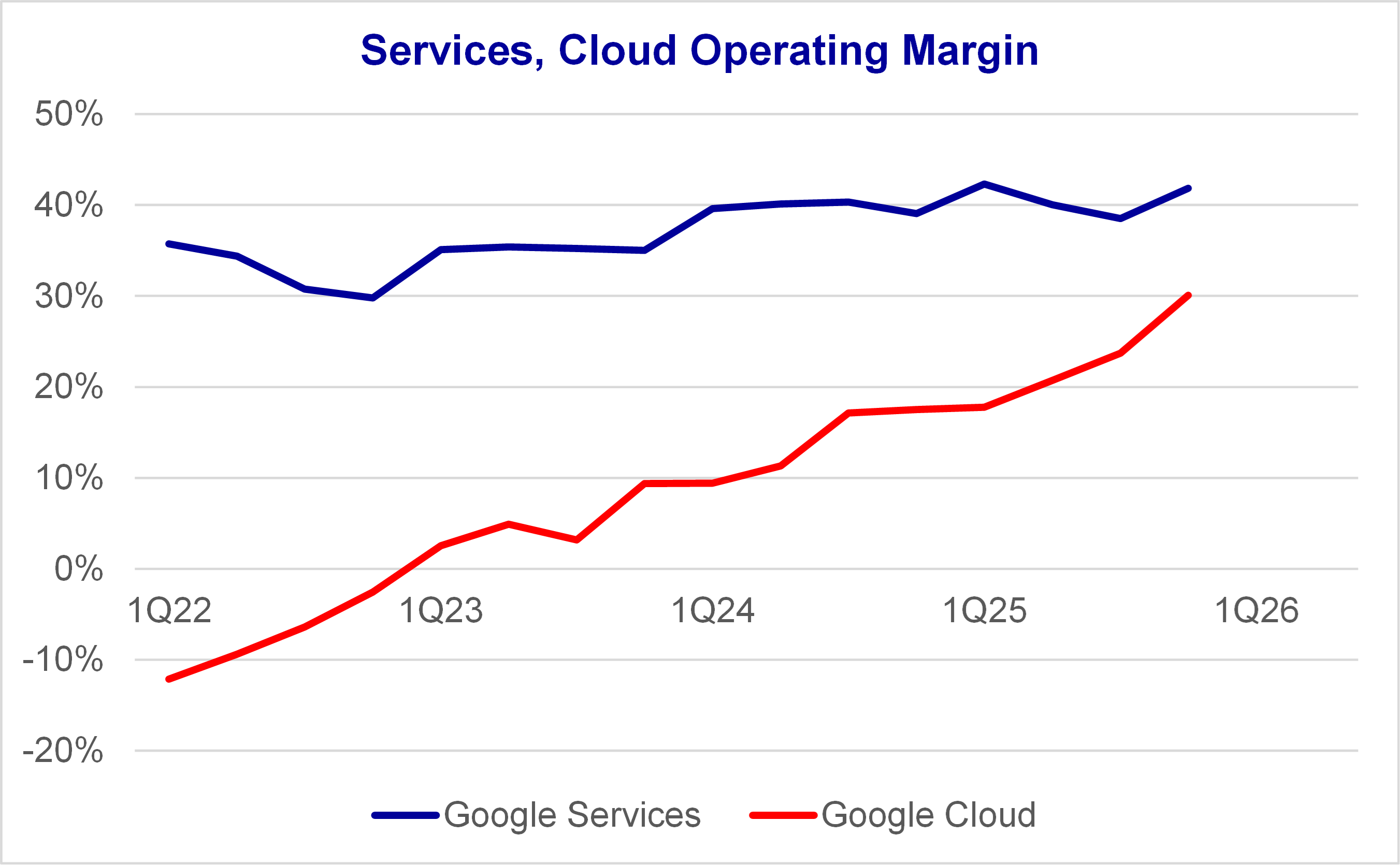

Google Services: higher revenue growth (year-ago 10%, 4Q25: 14% YoY) and Operating Margins upside (year-ago 39%, 4Q25: now 42%).

Cloud: accelerated revenue growth (year-ago 30%, 4Q25: 48% YoY) and Operating Margins expansion (year-ago 18%, 4Q25: now 30%).

As usual, no guidance. Capex will double in 2026 to $180bn. That’s a record high ~37% of revenues, hence a very major bet on accelerating growth / margins.

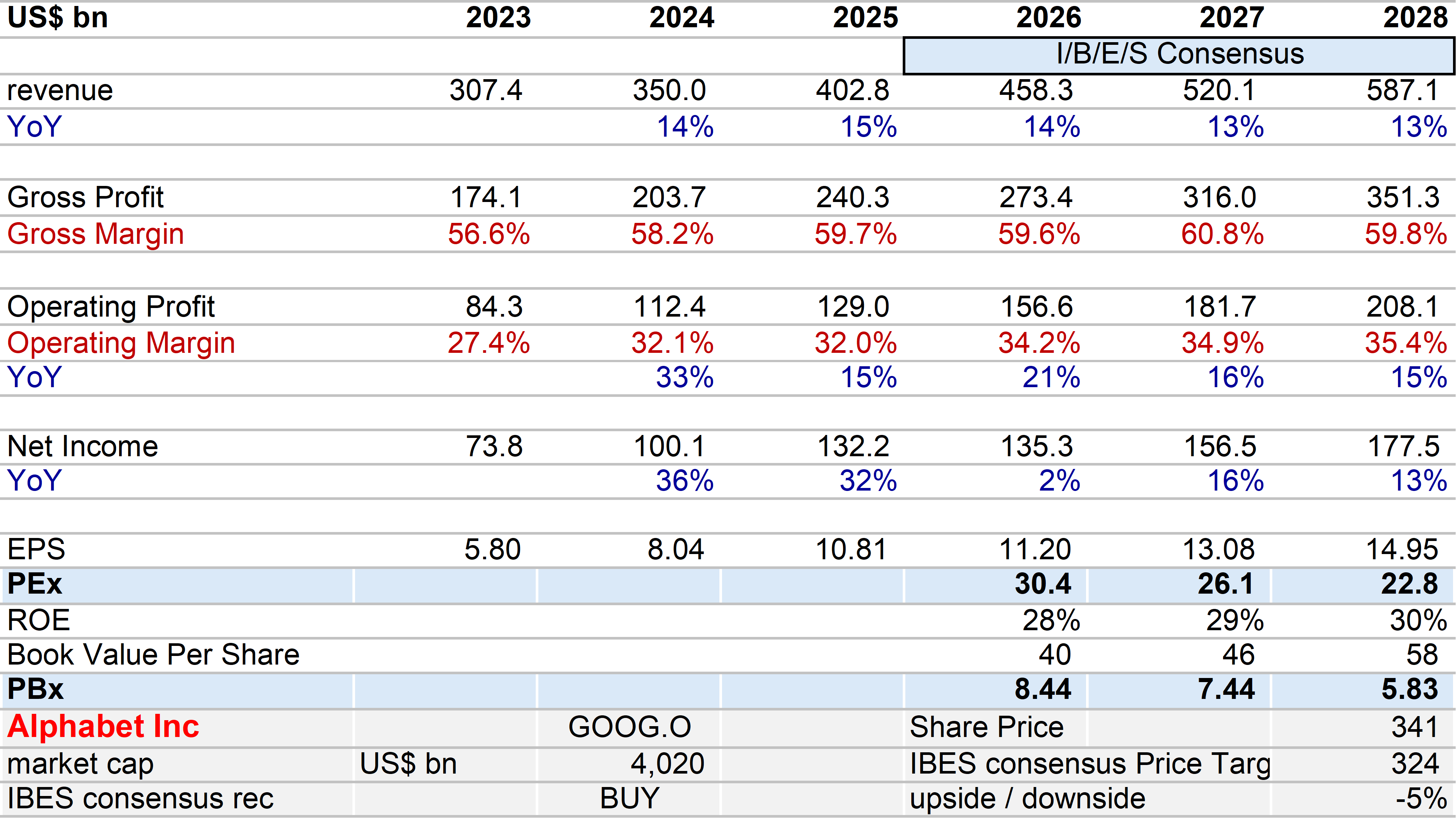

Consensus is reasonable-to-low with 14% revenue growth and 21% Operating Profit growth in 2026, 13% and 16% in 2027. I expect upward revisions. Valuations are high but growth is accelerating.

Management messages (and my comments)

CEO: We are seeing our AI investments and infrastructure drive revenue and growth across the board to meet customer demand and capitalize on the growing opportunities ahead of us. Search saw more usage in Q4 than ever before as AI continues to drive an expansionary moment.

Comment: management style is “a cautious tone”. They never over-promise, they don’t guide. During calls, they never provide explanations that could be viewed as “a guide”. That’s, imo, the significance of worlds like “growing” and “expansionary”.

AI in Search

These new AI experiences are proving to be more helpful and are driving greater usage.

First, once people start using these new experiences, they use them more. In the US, we saw daily AI mode queries per user double since launch.

Second, people are engaging in longer, more complex sessions. Queries in AI mode are 3 times longer than traditional searches.

Third, people are searching in new ways beyond text. Nearly 1 in 6 AI mode queries are now non-text using voice or images.

Comment: beyond the network effect, AI shows compounding platform effect.

A bunch of product announcements around AI Agents, Gemini, but this one: we laid the groundwork for shopping in the AI era by introducing a new open standard for ecommerce, the Universal Commerce Protocol, built alongside many retail industry leaders.

Comment: this doesn’t mean that Alphabet wants to get into eCommerce (ie logistics is too costly / complex) but help vendors outside of Amazon.

AI in Cloud

One, we are winning more new customers faster. We exited the year with double the new customer velocity compared to Q1.

Two, we are signing larger customer commitments. The number of deals in 2025, over a billion dollars, surpassed the previous three years combined.

AI investments drives better growth

We are seeing our AI investments and infrastructure drive revenue and growth across the board to meet customer demand and capitalize on the growing opportunities ahead of us.

Our unrivaled infrastructure serves as the bedrock of our AI stack. We have the industry’s widest variety of computer options that includes GPUs from our partner Nvidia who announced at CES that we’ll be among the first to offer the latest Vera Rubin GPU platform plus our own TPUs that we have been developing for a decade

As we scale, we are getting dramatically more efficient. We were able to lower Gemini serving unit costs by 78% over 2025 through model optimizations, efficiency, and utilization improvements.

Our first party models, like Gemini, now process over 10 billion tokens per minute via direct API use by our customers, and the Gemini App has grown to over 750 million monthly active users. Search saw more usage than ever before, with AI continuing to drive an expansionary moment.

AI Capex

To meet customer demand and capitalize on the growing opportunities we have ahead of us, our 2026 CapEx investments are anticipated to be in the range of $175 to $185 billion.

The investment we have been making in AI are already translating into strong performance across the business. Our successful execution coupled with strong performance reinforces our conviction to make the investments required to further capitalize on the AI opportunity.

Comment: Alphabet’s Capex can’t stay at 35% of revenues for a long time. Maybe 2-3 years. Then either Capex declines, or revenue growth accelerates above 20-25%. I guess that GOOG’s management is expecting the later. Chart below assuming 20% revenue growth in 2026:

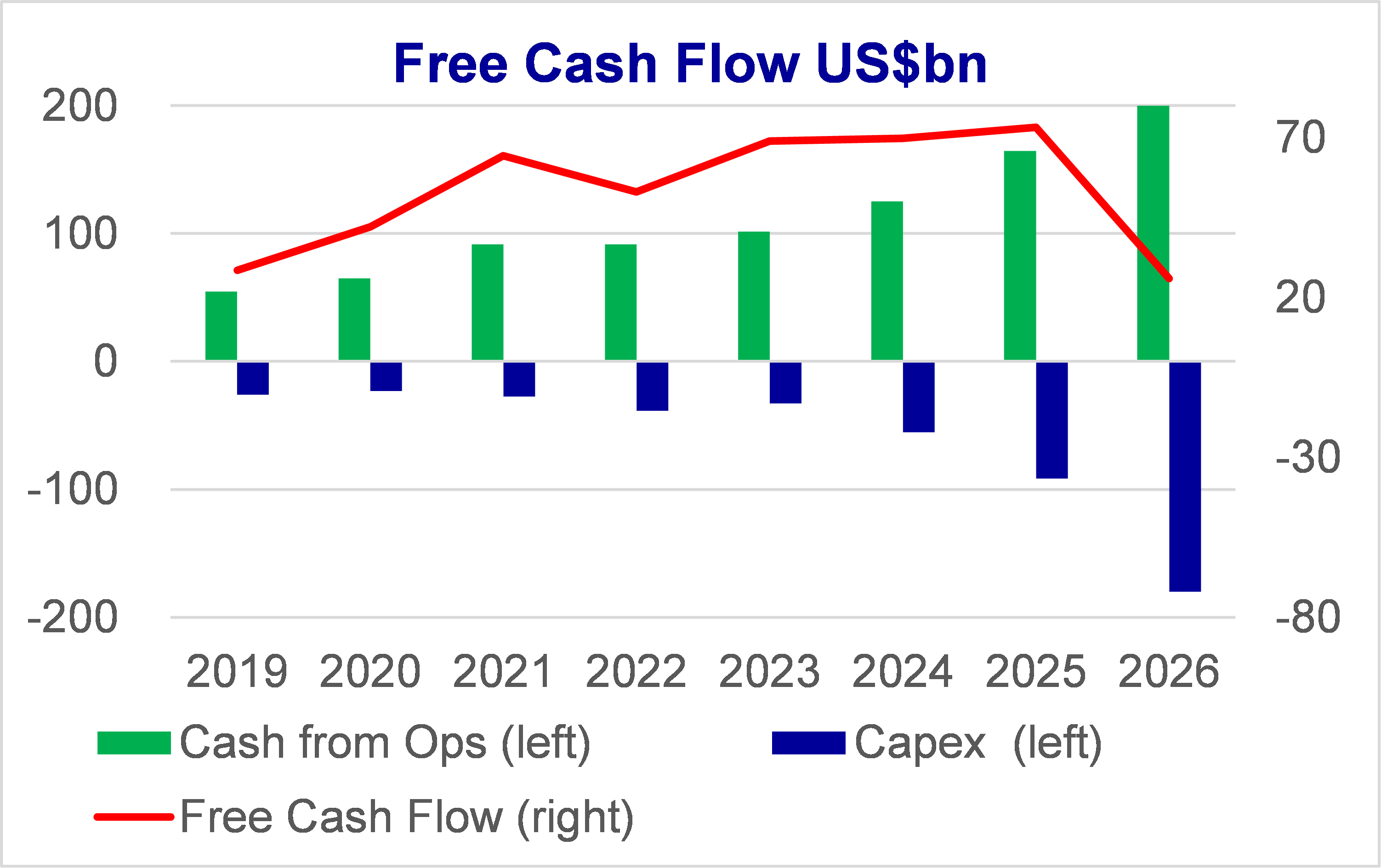

Comment: Alphabet can afford $180bn Capex, but that will squeeze free cash flow a bit:

Capex: 2025 $91bn, 2026 $180bn.

Cash from Ops: 2025 $165bn and up 31% YoY, 2026 assuming $206bn or +25% YoY.

This implies a sharp drop in Free Cash Flow but still a nice $26bn, maybe implying less share buybacks. But GOOG has $127bn in cash and eq.

The point is: if GOOG believes that AI investments support higher revenue growth, higher margins, they certainly can spend $180bn in Capex.

Supply constrained

We’ve been supply constrained even as we’ve been ramping up our capacity. Obviously, our CapEx spend this year is an eye towards the future, and you have to keep in mind some of the time horizons are increasing in the supply chain… (later in the call) supply chain pressures we’re seeing externally… specifically at this moment, maybe the top question is definitely around compute capacity, all the constraints, be it power, land, supply chain constraints, how do you ramp up to meet this extraordinary demand

(comment on Q26 revenue) we expect growth to be driven by ongoing innovation in the user experience, as well as improved ROI for advertisers. In Google Cloud, we’re seeing significant demand for products and services and continue to drive strong growth despite the tight supply environment we’re operating in.

AI Capex = increasing D&A

significant increase in our investments in technical infrastructure will continue to put pressure on the P&L in the form of higher depreciation expense and related data centers operations costs such as energy. In 2025, depreciation increased by nearly $6 billion or 38%, from $15.3 billion in 2024 to $21.1 billion in 2025.

Given the increase in our CapEx investments in recent years, we expect the growth rate in 2026 depreciation to accelerate in Q1 and meaningfully increase for the full year.

Comment:

D&A increased YoY by 28% in 2024, 38% in 2025, I assume +50% in 2026. And revenues up 20%. So D&A is definitely increasing faster than revenues and putting a bit of pressure on margins. But:

Its not dramatic: D&A is increasing by ~100bps of revenue per year.

2. Despite increasing D&A, margins are increasing. What’s the problem?

Consensus

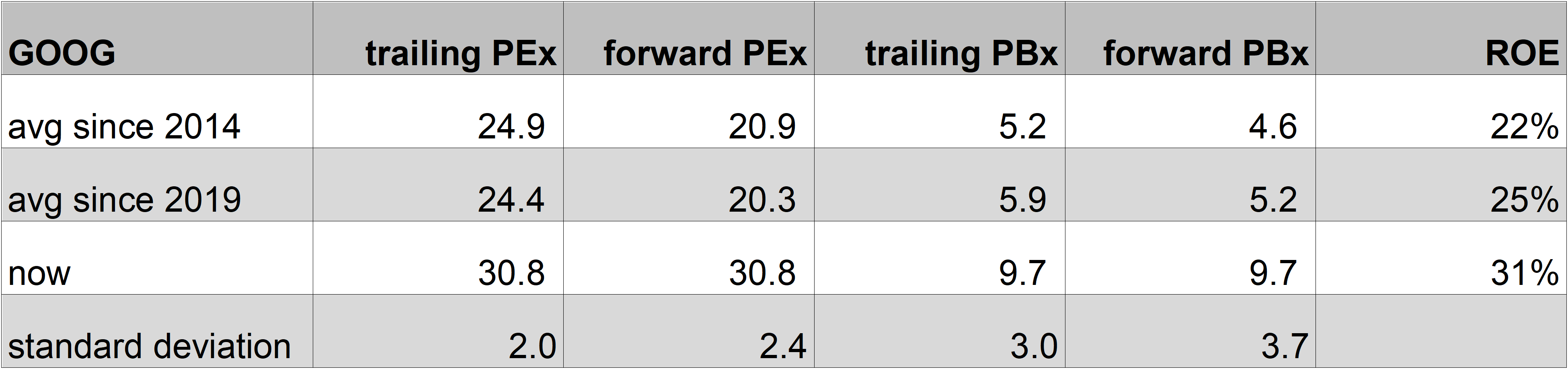

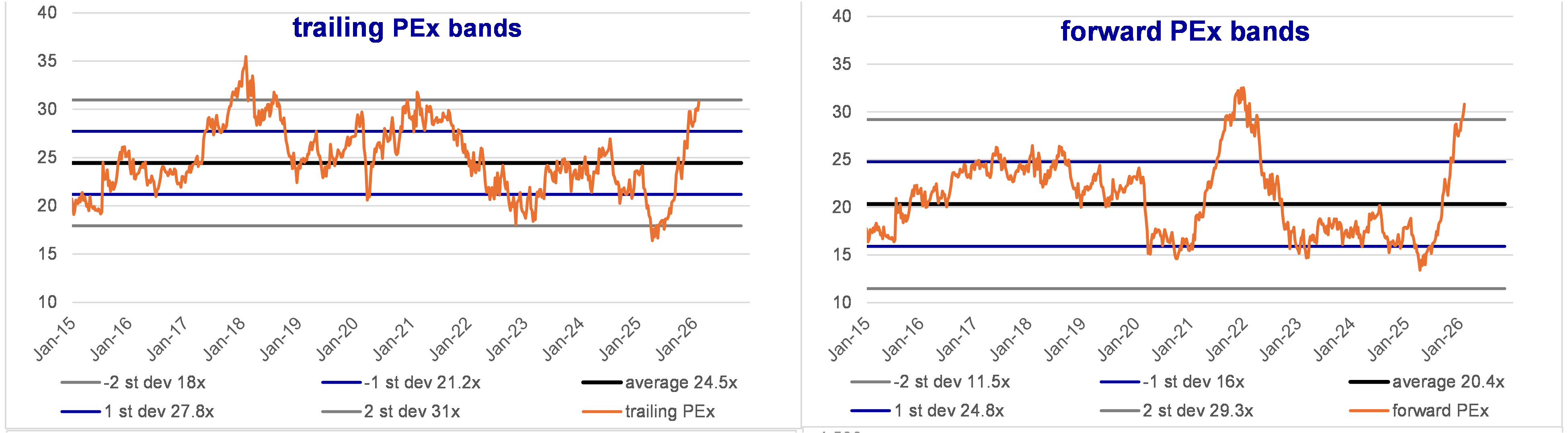

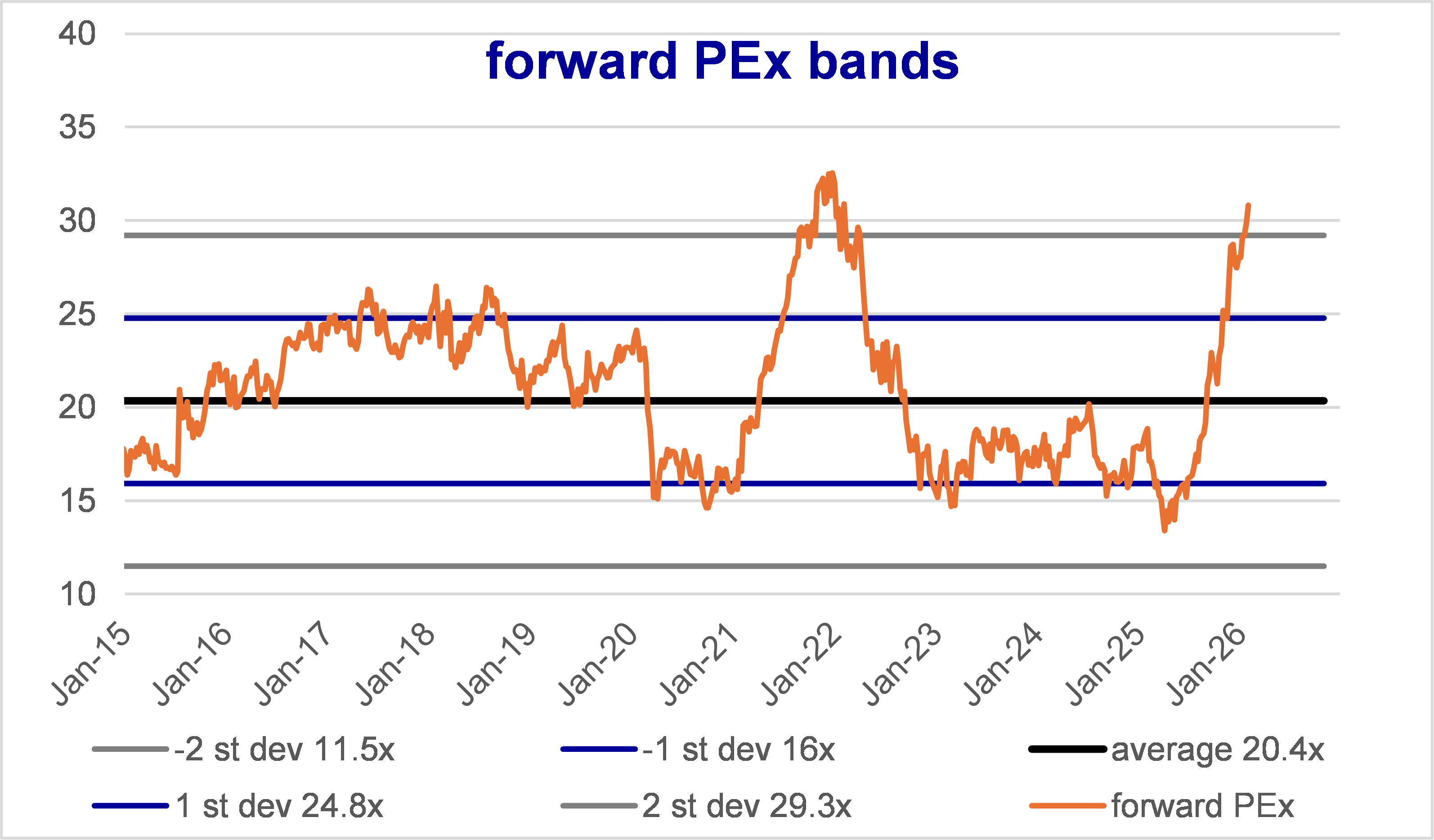

Valuations

Valuations are high and reflect funds flow: sell Microsoft (maybe NVDA, AMD) and buy more GOOG. Reverse flows is the risk.