Demand Destruction – when Massive Memory Price Hikes Kill Demand

Last episode on Thursday: HBM demand, let’s try to quantify.

End-demand destruction rarely happens in Consumer Tech. Consumers addiction level and wallet size find a way to justify buying yet another smartphone, a bigger TV, a small speaker, whatever guarantees your happiness. Demand destruction happens thru margins compression. Smartphone makers can’t make a phone below $250 any longer. It cannot be profitable, so this price-category is gone.

Affordability is almost never a problem for Enterprise spending, which think in terms of capex vs productivity, capex vs headcount, etc. Yet, if you’re the CFO / CTO you can decide to wait – these 10 years old Windows 10 computers can certainly run another 12 months.

Most demand is replacement demand – which means that you already have an older thing that still works – and buying the new thing can wait 6 months.

That’s very different when you want to buy 1) a new technology 2) that will lower production costs, or 3) increase revenues, or 4) could hurt you if you don’t have it – you just don’t know but you must have an answer to the question “what’s your AI strategy, dude?”

Demand Destruction is mostly a consumer electronics problem

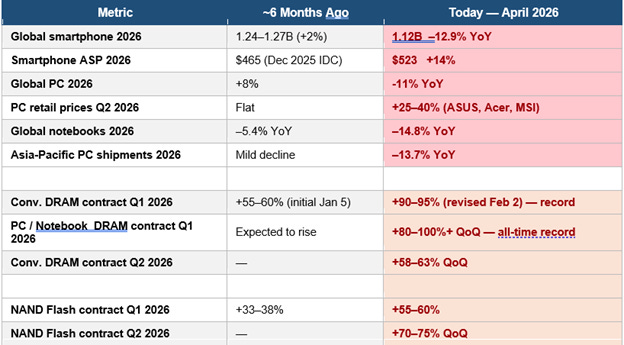

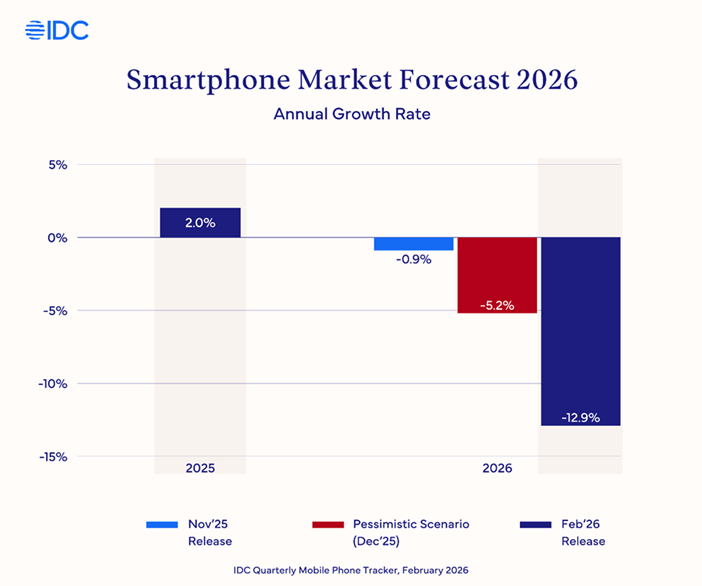

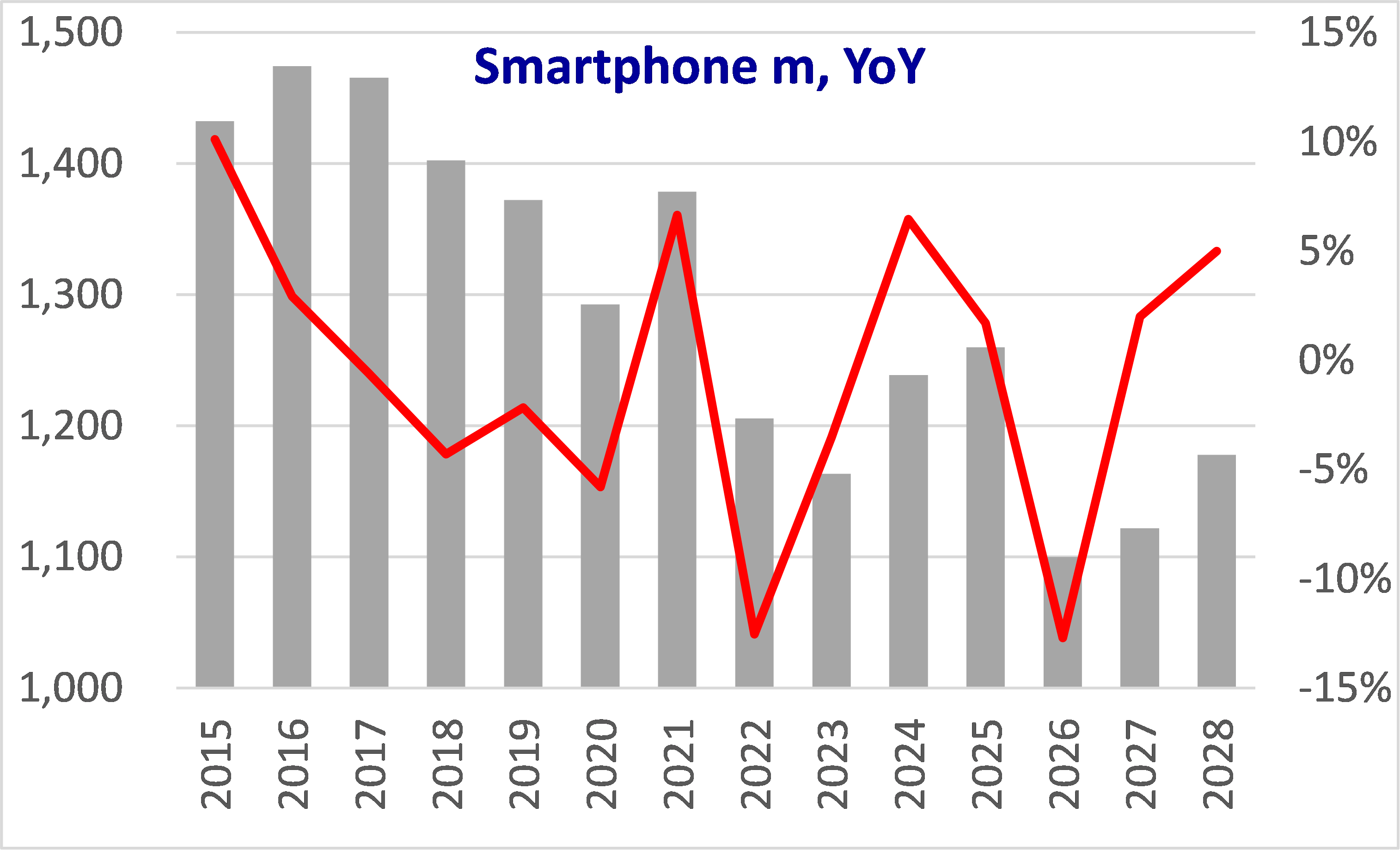

Smartphones. 6 months ago, most forecasts were expecting +2% unit growth in 2026. Now -13% YoY. Memory’s share of component costs (BOM) has surged from ~15% to ~35%.

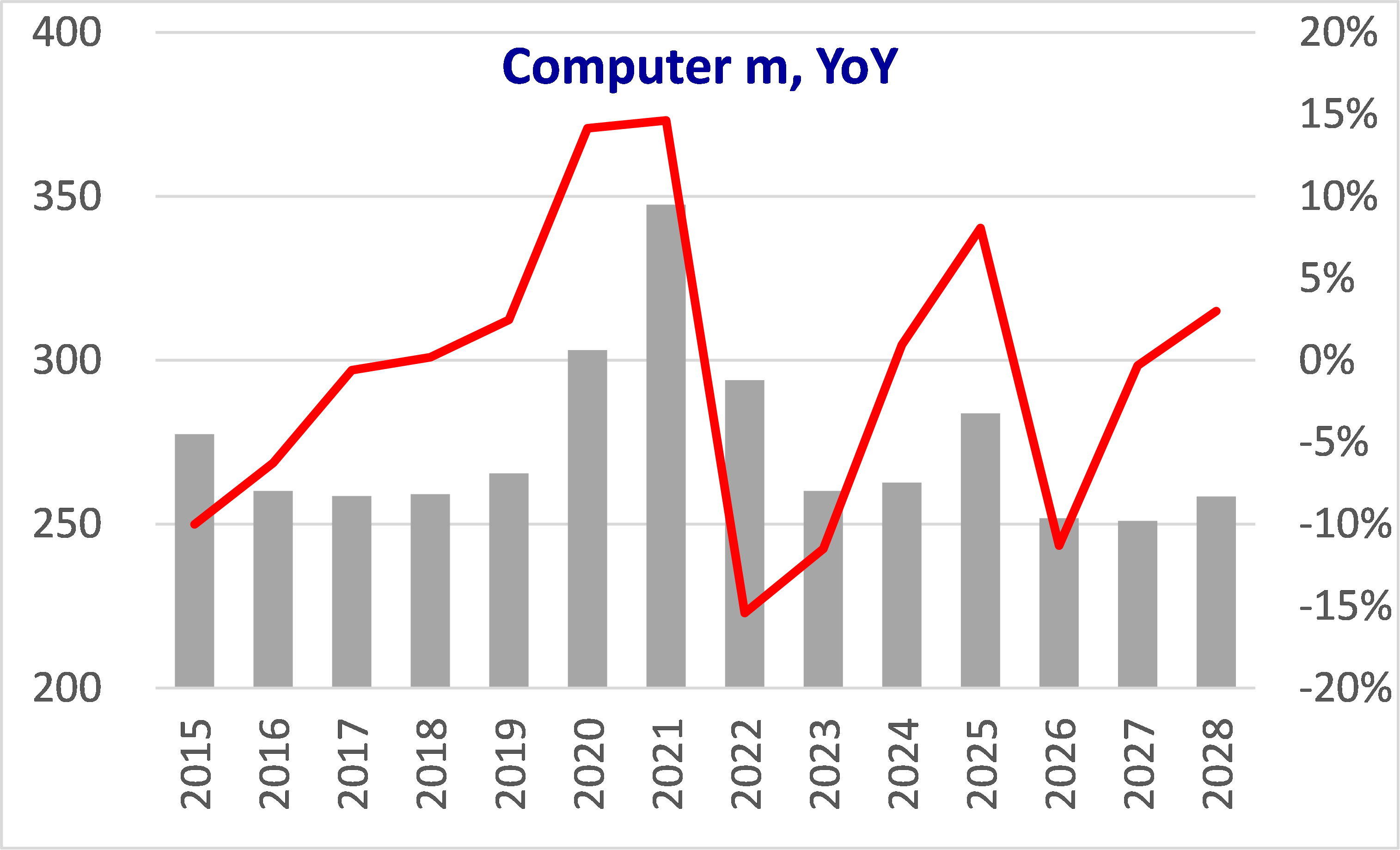

Computers. 6 months ago, very rosy forecasts expecting +8% unit growth in 2026 because Win10 end-of-life. Now -11% YoY. Memory share of notebook BOM up from below 10% to above 20%.

Game consoles. 6 months ago flat. Now -4% YoY.

Quantifying the $-impact on specific firms is not simple.

Most firms start by moving your product / price mix. You lower DRAM content from 12GB to 8GB. You lower NAND or SSD from 1TB to 1/2TB. You de-spec, mitigate the cost / price increase. That works well when cost increase by 20% – not when it doubles.

For many firms (ie phone, computers), say volumes decline -10%, ASP increase 10%, net-net revenues haven’t changed. Volume decline should hurt margins (there are a lot of per unit fixed costs in manufacturing, logistics), but maybe you can increase retail price by more than cost increase – BOM up 10%, retail price up 11%.

Mediatek and Qualcomm have cut down orders at TSMC by 15% (specifically for 4nm)

Apple is buying all the DRAM and NAND it can find – and absorbing the costs into itsa fat margins

Hey Intel, what about making fewer PC CPU and more Server CPU?

Memory makers: Samsung, SK Hynix, Micron, Kioxia, Sandisk

Smartphone: Apple Samsung Xiaomi Mediatek Qualcomm TSMC

Computers: AMD Intel Lenovo HPQ Dell

Charts and tables below.

Summary data

I paste the table below because it’s sort of pretty. Made by Claude. Claude can do that. Find news on “impact of memory price increase”, make a pretty table. Beyond that… you really have to check and recheck everything Claude does.

Smartphone

Quotes from IDC, TrendForce, etc etc.

IDC: “… smartphone market looks dire… currently forecasting the worldwide market to decline by 12.9% in 2026, with revenues declining slightly by 0.5%. We expect 2027 to see a modest 1.9% growth for smartphones, with a stronger 5.2% rebound in 2028”

Me: part of that forecast is that IDC does not expect costs / prices to decline in 2027, so there is not much pent-up demand. But that’s also what happens in a replacement market: demand doesn’t come back later, the replacement cycle just gets longer.

Smartphone volume decline starts in 1Q26, volumes to decline 6.8% YoY “as memory prices climb and some vendors, particularly smaller ones, struggle to secure and/or pay for adequate supply”

“unit volumes to fall off dramatically beginning in the second quarter”

“the 2026 revenue picture will look deceptively stable due to inflated ASPs”

Chinese news mentions that Apple has mopped up mobile DRAM and LP-DDR at premium prices for iPhone supply.

MediaTek and Qualcomm cut wafer orders. Memory costs make mid-range and entry smartphones economically unviable. MediaTek and Qualcomm cut 4nm wafer starts by ~15%

Low-range Android smartphones are de-speced from 8GB to 4GB (ex. Oppo and Honor 2026 entry-level models).

Computers

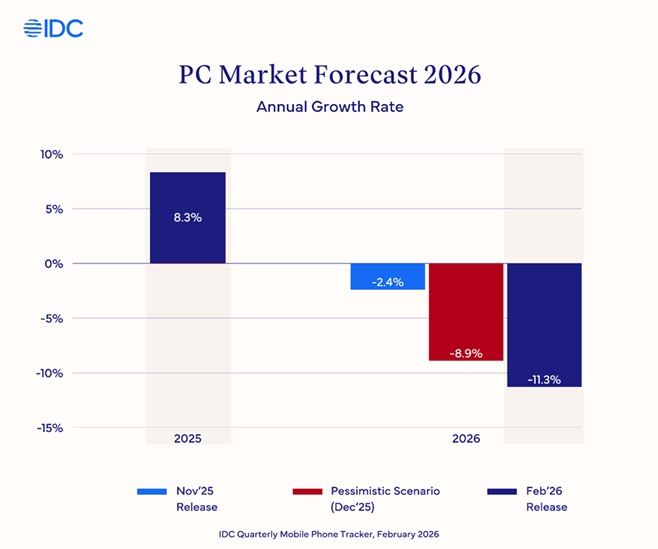

IDC: “For PCs, we are now forecasting the worldwide market to decline by 11.3% in 2026, while revenues grow 1.6% due to increased ASPs. Our current forecast shows the market flattening in 2027, with a rebound now pushed out to 2028”

Me: same as for smartphones. Component cost does not decline in 2027, so no pent-up demand. Volumes just stabilize at a level 10% lower. Maybe better luck in 2028 if costs have declined.

“Shipments ramped significantly in the fourth quarter of 2025. These elevated levels have continued into 1Q26, as OEMs rush to ship products before memory price increases take full effect”

This will continue into Q1 2026: shipment levels will look pretty good – before they collapse from 2Q26.

OEMs raise prices and cut entry-level lineups. ASUS warns +25–30% price increase in Q2. MSI has cut one-third of entry-level lineup.

The price of CPU, PCBs batteries, PMIC is also rising.