Broadcom: the stock is falling -14% ! how bad was it? Not really bad but…

TPU financing

I don’t think that Broadcom guidance is the reason for the huge decline in stock price. It’s a few % away from expectations.

Rather, the financial engineering with Apollo and Blackstone to guarantee leasing TPU to Anthropic and OpenAI looks very large. At least $200bn. Could be $400bn. Not clear what guarantees Broadcom will provide on these loans.

Or we’re having a little correction for the Semi sector, after a mad rally since early April.

What’s wrong with the outlook?

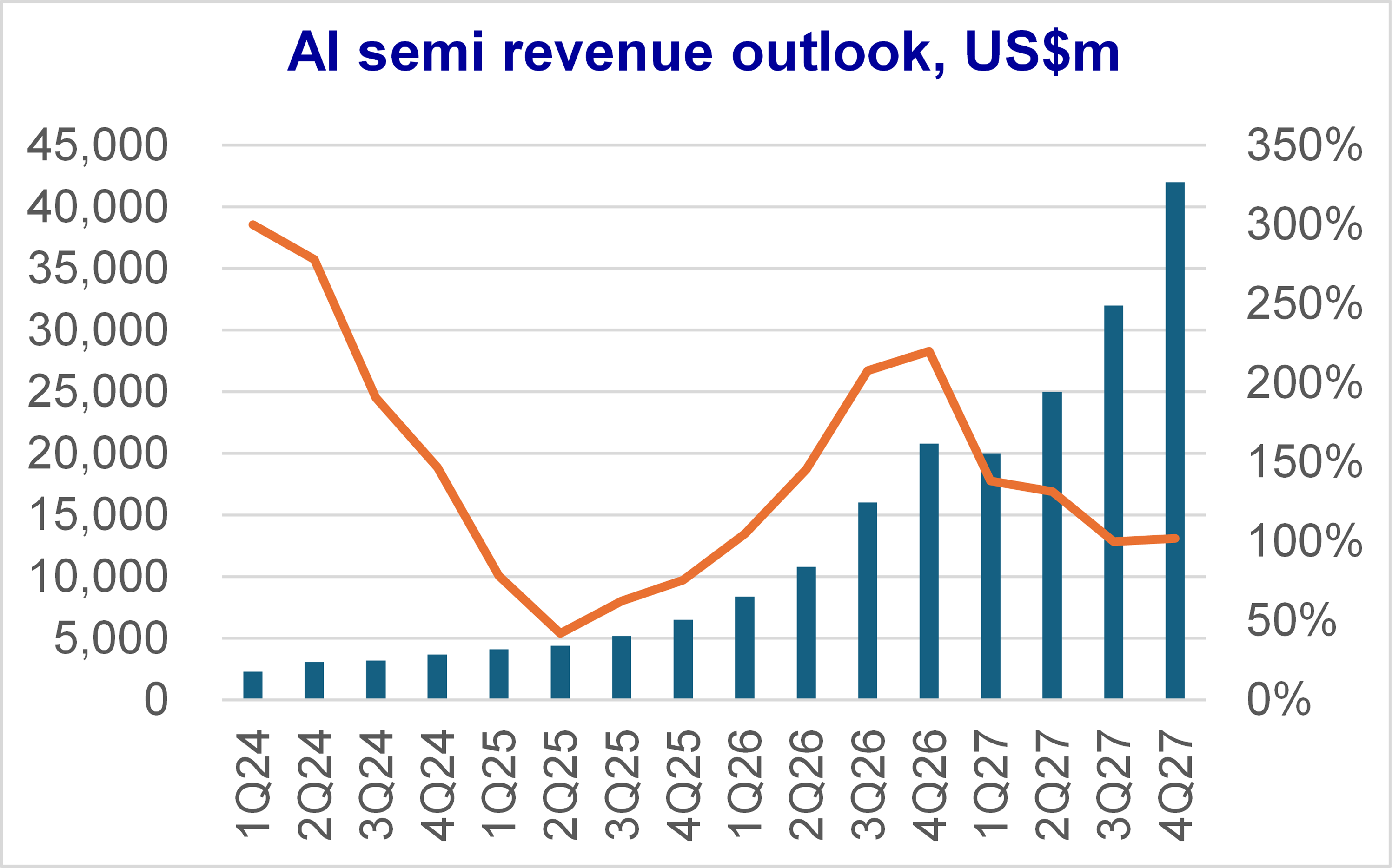

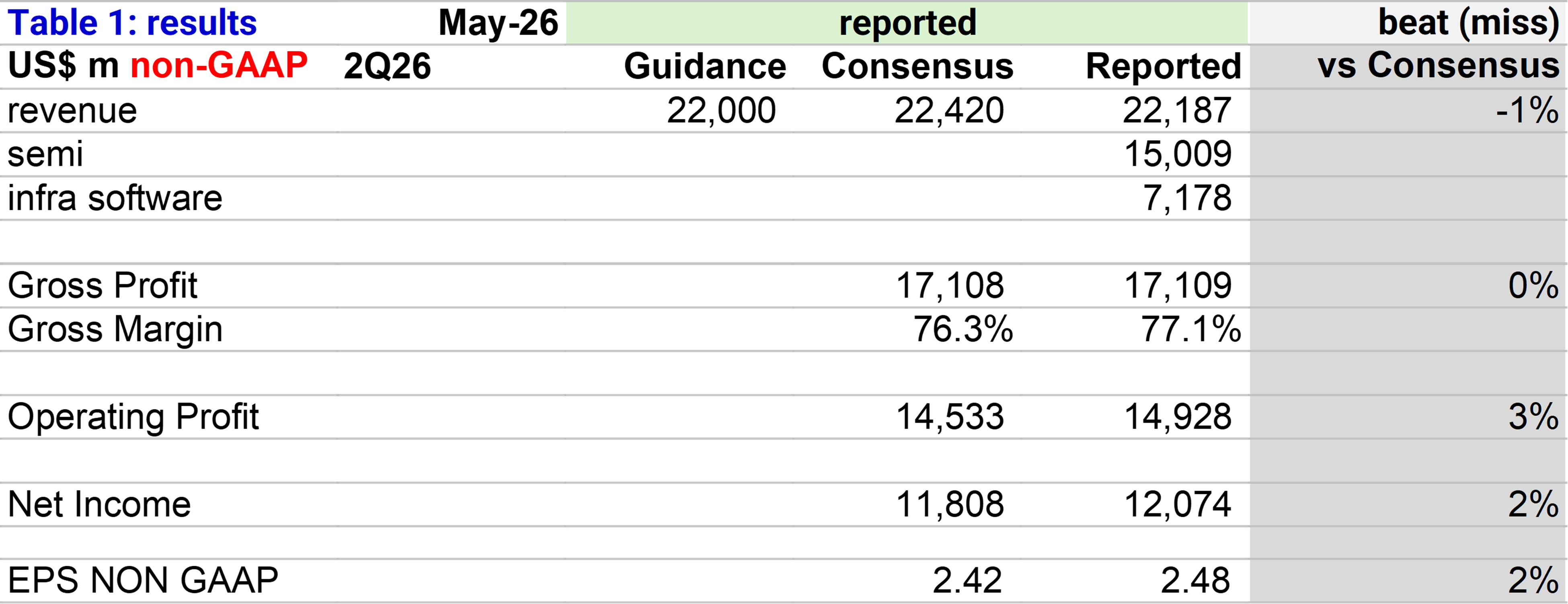

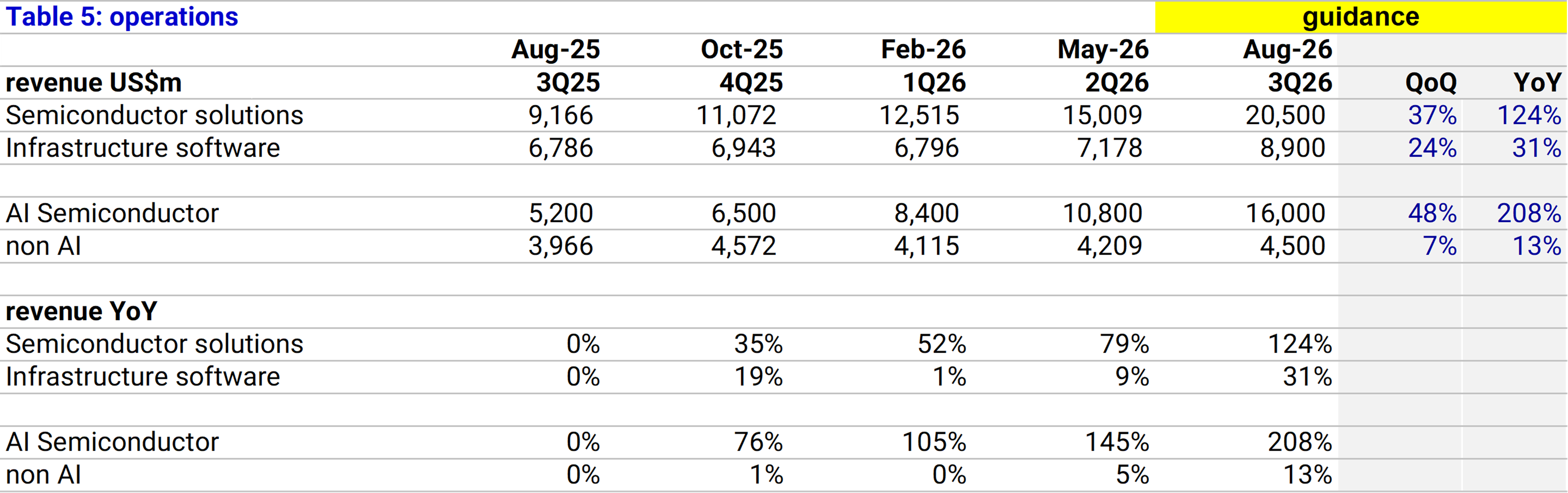

News says that Broadcom results were poor because ’26 AI chips revenues are guided at $56bn, but Consensus is at $57.6bn: 3% below! Or 3Q revenue guidance was also 3% below… I don’t think there’s a panic over this.

the firm maintained its ’27 AI revenue forecast “in excess of $100bn”, while pointing out in a convoluted way that if growth continues at 100% (2x)… you get $120bn.

“on the second half (of ’26), we keep the momentum going as we expect to see in 2027. What we will see in 2027 is continued growth of the level we’re talking about. And if you drive on that basis of what we’re seeing here, in the range of 2x what 2026 will be, I think you will easily see that 2027 will exceed very easily $100 billion in 2027”.

warning, again, that AI chip growth will dilute gross margins, and again in a convoluted way but it could be accretive to operating margin. You got to hear it to believe it:

“semiconductor business grows, just to reiterate, on a consolidated basis, relative to our software business, you’re going to have a decline in margins, right, a bit. You’ll have compression, but remember that it’s accretive because we have strong operating leverage, right? So our operating margins will stand up a bit over time to that”

Seriously, I am not sure that there’s bad news here. ’27 AI revenue between 100-120bn with a bias toward $120bn. Operating Margin won’t decline:

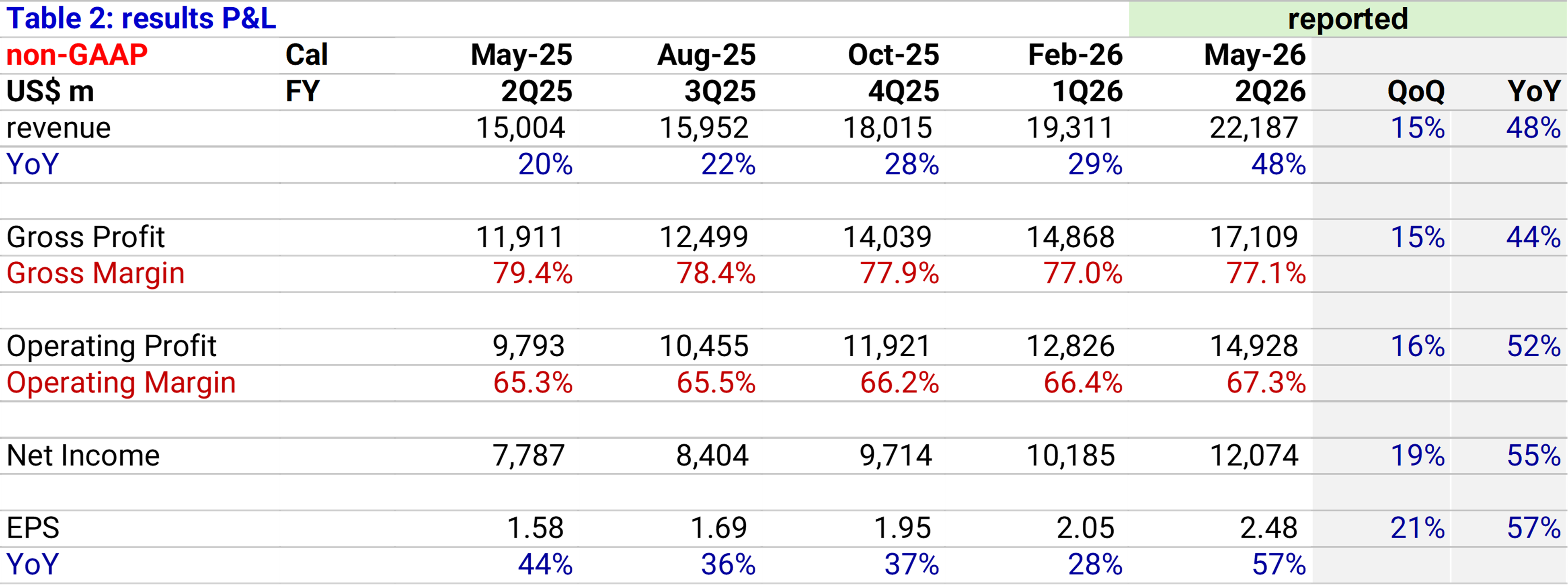

in ’25 65.7%

it’s up in ’26 so far at 66.9%

More important: TPU financing

CEO hinted that the TPU leasing business will become very large. That’s called the “AI XPV platform”. Details aren’t clear to me, i.e. little disclosure but refer to Bloomberg, another Bloomberg and Reuters. The idea is that Google agreed to “sell” TPU to Anthropic and OpenAI. Broadcom creates an “AI XPV platform” together with Apollo and Blackstone. These 2 provide the financing for the chips (i.e. they pay Google). Anthropic and OpenAI rent the chips, i.e. pay back Apollo and Blackstone – it’s a loan. And apparently Broadcom provides a “backstop”, i.e. guarantees the loans to Anthropic and OpenAI.

Ahhh another circular financing thingy like Nvidia with CoreWeave. You are financing your customers! Not exactly as Apollo and Blackstone are providing the loans, but there’s an unknown Broadcom guarantee in there.

The size looks very large:

“we are creating the AI XPV platform with Apollo and Blackstone and other leading investors to deploy more than 20 gigawatts of compute capacity through 2028. The first tranche of this platform valued at $35 billion is in fact currently being launched by Apollo.

Anthropic: we are providing access to Broadcom TPU-based compute of over 1 gigawatt. we entered into an agreement to access another 5 gigawatts of next generation TPU in 2027

OpenAI: production late 2026. contractual commitment to deploy 1.3 gigawatts in 2027, as part of the larger 10 gigawatts by 2029”

You can pick up from the conf call that ’27 AI chips revenue ($100bn) is equivalent to 10 Gigawatt, then.. 1GW = $10bn in AI chip revenue, and 20 GW means $200bn? That’s a minimum estimate!

I am hearing much bigger numbers. For example Nvidia GB200-based data center. 1GW = $38B total CapEx, of which:

servers ~$23B

of which

~70% is compute silicon or ~$16-18B in GB200

~25% is networking

Storage $10bn

The building, power, air con, etc $5bn

My estimates for Amazon and Google’s Data Center is $33-35bn per GW

You can find lower numbers, looking at Nebius, Iren, CoreWeave but these firms aren’t clear about exactly what their Capex covers (ie land, building, only chips, etc). The range is $15-21bn / GW.

Conclusion: if Broadcom CEO is correct on “deploy more than 20 gigawatts of compute capacity through 2028”, the cost of that is at a minimum $200bn. Could be as high as $400bn.

Another possibility is simply:

Semi correction is starting – after a mad rally since early April. Amplified by news that are seen as bad news.

TSMC Warns Chip Supply Won’t Meet AI-Fueled Demand for Years. Yes, we know that.

Microsoft’s AI Chief Says Anthropic Models Are Too Expensive. Trashing your competitor?

From the conference call:

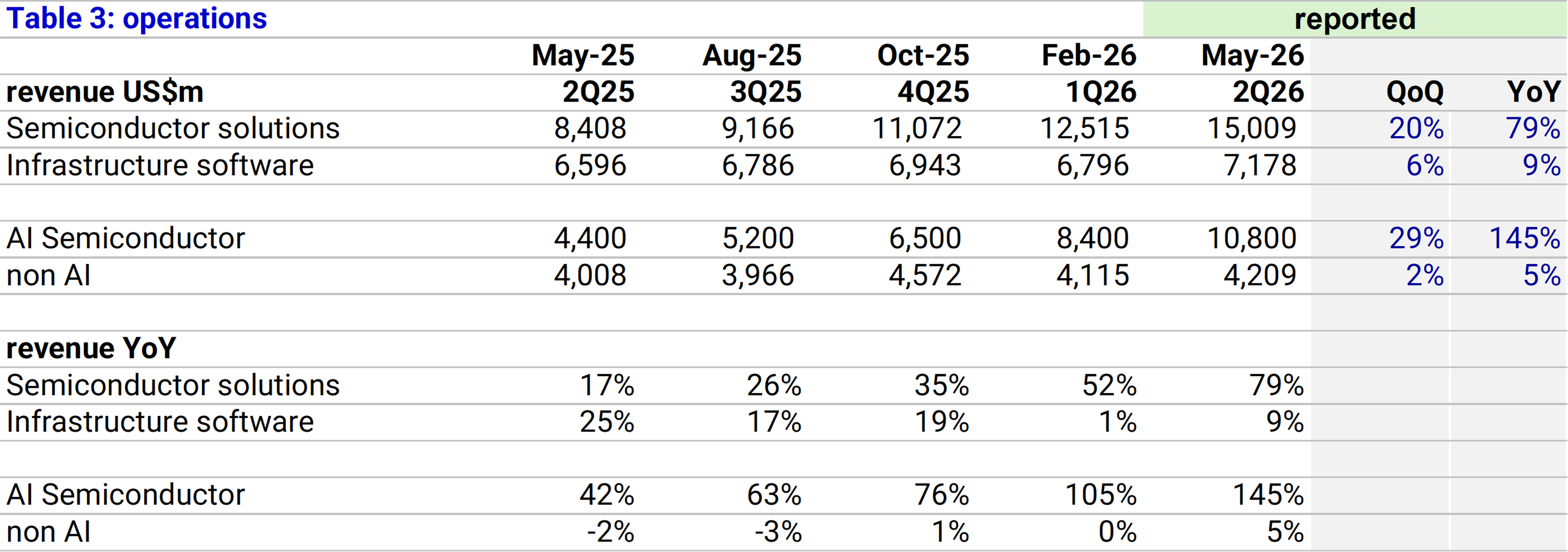

semiconductors. Q2 revenue was a record $15 billion, up 79% year on year. Driving this growth was AI semiconductor revenue and a record $10.8 billion, up 143% year on year and above our outlook. Networking represented almost 40% of our Q2 AI revenue. Demand for XPUs and networking is simply insatiable

During the quarter, bookings for AI semiconductors were over $30 billion, against the $10.8 billion we shipped.

In the second half of 2026, we expect AI semiconductor revenue to double from the first half. Consistent with this trend in Q3, we expect AI semiconductor revenue to accelerate to $16 billion, up over 200% year on year.

full-year 2026, AI semiconductor revenue $56 bn, up 180% YoY.

fiscal year 2027 reiterate AI semiconductor revenue guidance in excess of $100 billion

on the same trajectory as we are seeing in the back half of ‘26.

you will easily see that 2027 will exceed very easily $100 billion in 2027, we are continuing to say that it will be over $100 billion in 2027.

fiscal 2028 revenue growth to continue. We expect, in fact, ‘28 to be a substantial growth

for ‘27, we indicated about 10 gigawatts shipment in ‘27. That’s still very much intact. They will be shipping 10 -- we’re planning to ship 10 gigawatts in ‘27 and that nothing has changed, back-half loaded to that extent, yes, which really provides an interesting trajectory into ‘28 with this back-half trajectory. So ‘28, we expect a lot more gigawatts.

we have been able to secure supply for our needs, ‘26, ‘27. Working on ‘28 and ‘29 right now

Our visibility runs all the way to 2028 right now

Google: long-term agreement to develop and supply multiple generations of TPUs and AI networking

long-term agreement with Google: it’s a commitment that is very substantial in dollars, very, very substantial amount of dollars. Now, we also accept the fact that given the growth of AI compute by our partner Google, we fully expect that there’ll be some diversity of sources for them

Anthropic: we are providing access to Broadcom TPU-based compute of over 1 gigawatt. we entered into an agreement to access another 5 gigawatts of next generation TPU in 2027

OpenAI: production late 2026. contractual commitment to deploy 1.3 gigawatts in 2027, as part of the larger 10 gigawatts by 2029

Meta: partnership for multiple generations of MITA XPUs. we expect to deploy 3 gigawatts through the end of 2028. Initial order for 1 gigawatt, includes XPUs and networking, will start in the second half of 2027.

other two customers: expect shipments late 2026, accelerate in 2027. purchase orders for $6 billion.

For scale up within racks, we enable direct attached copper based on an industry-leading 200G and 400GB SerDes, driving co-packaged copper with Ethernet and PC Express switches.

For scale out between the racks, we have been shipping the industry’s only 100-terabit Ethernet switch, the Tomahawk 6, for over a year. We will now be taping out our next-generation 200-terabit switch this quarter.

CPO, Co-Packaged Optics, 1.6-terabit DSPs, CW, and EML lasers, we are the de facto standard in the industry.

Our strategic vision is to bring together Broadcom’s leading technology and investor partners with the strongest balance sheets to deliver at scale sufficient compute capacity at the lowest cost and power for the leading AI frontier labs, including Anthropic and OpenAI. To deliver this vision, we are creating the AI XPV platform with Apollo and Blackstone and other leading investors to deploy more than 20 gigawatts of compute capacity through 2028. The first tranche of this platform valued at $35 billion is being launched by Apollo.

infrastructure software

Q2 revenue $7.2 billion up 9% YoY

Q3 revenue $8.9 billion up 31% YoY

released VMware Cloud Foundation 9.1, focused on improving infrastructure efficiency, security, and support for enterprise, AI inferencing workloads. VCF 9.1 for on-prem cloud computing release heterogeneous compute support across GPUs and CPU architectures, including AMD, Intel, and NVIDIA platforms, enabling enterprise cloud customers to run AI Kubernetes and traditional virtualized workloads on a common private cloud environment.

As the proportion of AI revenue significantly grows in Q3, we expect Q3 consolidated gross margin to be down to approximately 74%. This decline in gross margin does not represent a structural change in semiconductor margin, rather it reflects product mix between semiconductors and infrastructure software.

Timely and well written piece. Would love to get your views / expectations vs the street.