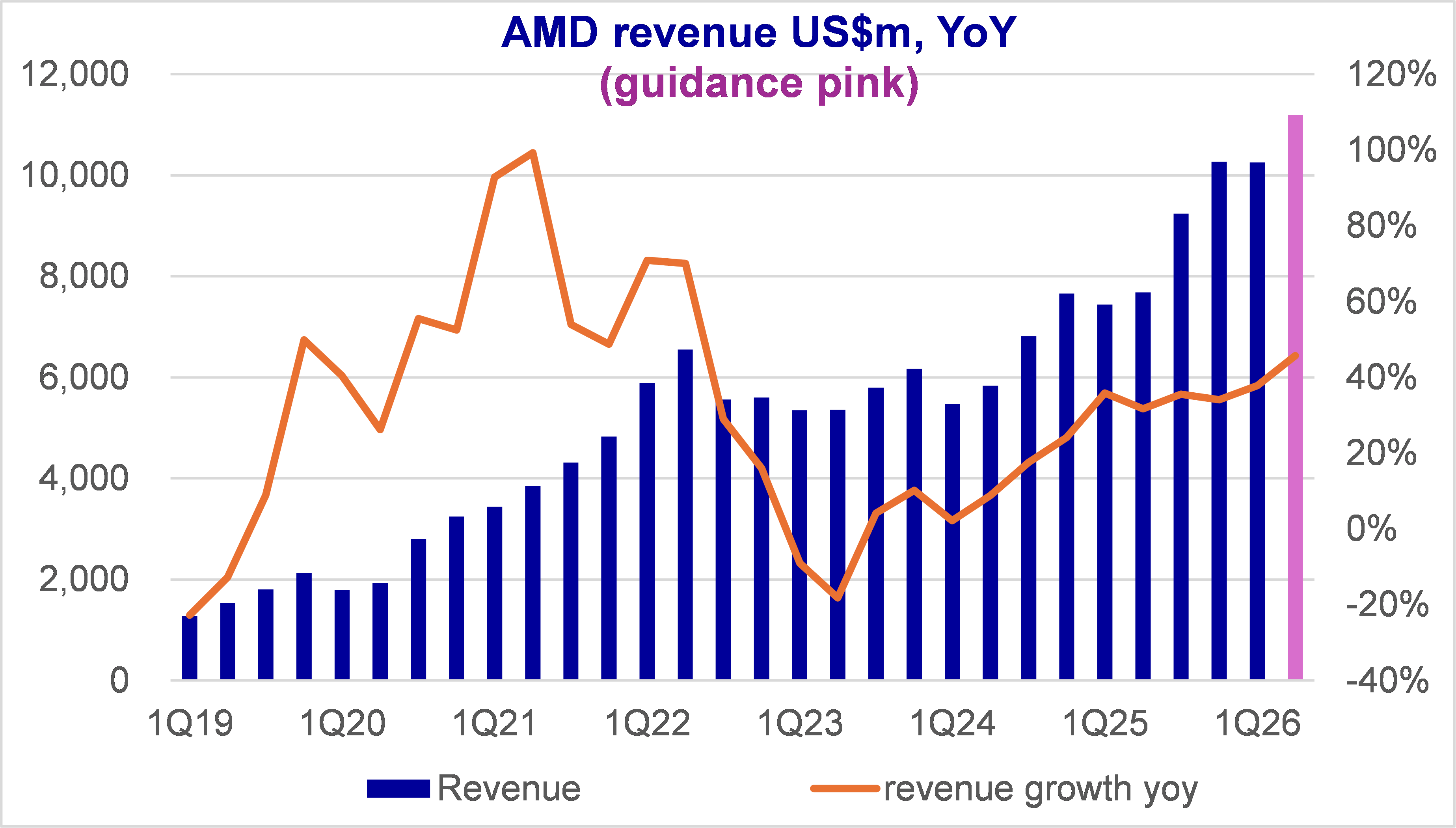

AMD: beyond a strong quarter, higher growth for next 3-4 years

Consensus will revise up 15-20%, stock trades at 23-25x ‘27EPS and ~18-20x ’28 EPS.

Same story as Intel: Server CPU demand is accelerating on AI inference and agents. AMD is in a better position than Intel: AMD is gaining share and has a hyperscale / inference specific roadmap.

That’s a dramatic change in narrative: the market was focused on GPU share gains – now we have a Server CPU story. We actually have both. The past few quarters of AMD GPU sales were unimpressive but growth is anchored to MI450 GPU and Helio racks from 4Q26 or early 2027.

With higher Server CPU growth (2026 could be 60-70% YoY, 2027 ~50%), Consensus is going to be 15-20% too low, implying that the stock trades at 23-25x ‘27EPS and ~18-20x ’28 EPS. Paradoxically, AMD appeared very expensive 6 months ago, and now it’s cheap – and a lot more attractive than Intel given its Foundry black box.

Main messages

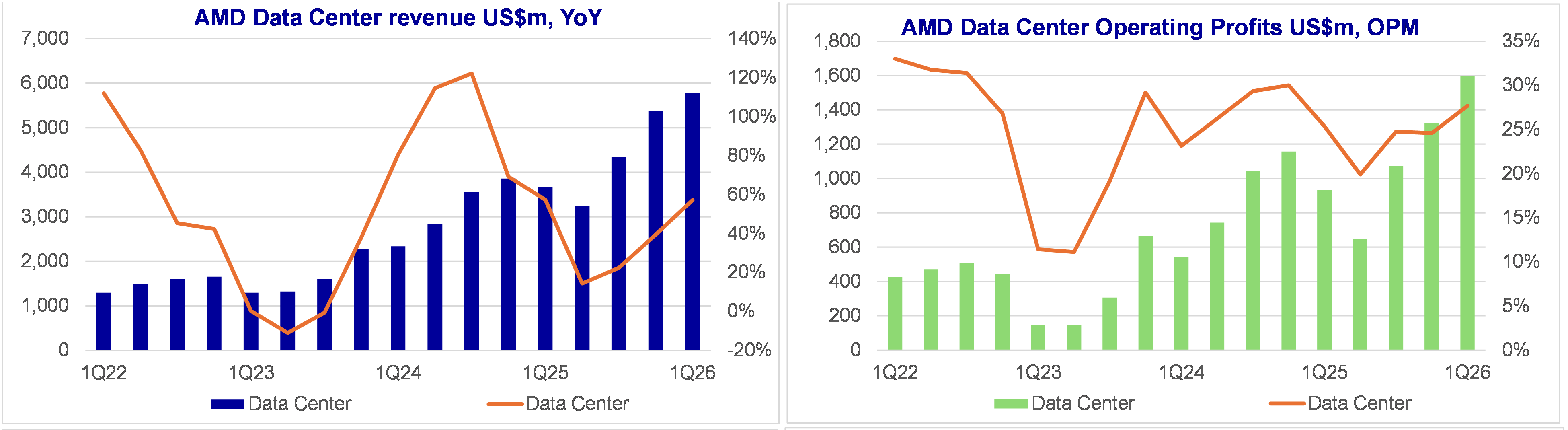

Server CPU

CEO Lisa Su doubled the 2030 server CPU Total Addressable Market (TAM) forecast from $60 billion to $120 billion. In other words, AMD was expecting server CPU TAM growing ~18% annually 2030. Now revised up to >35% CAGR

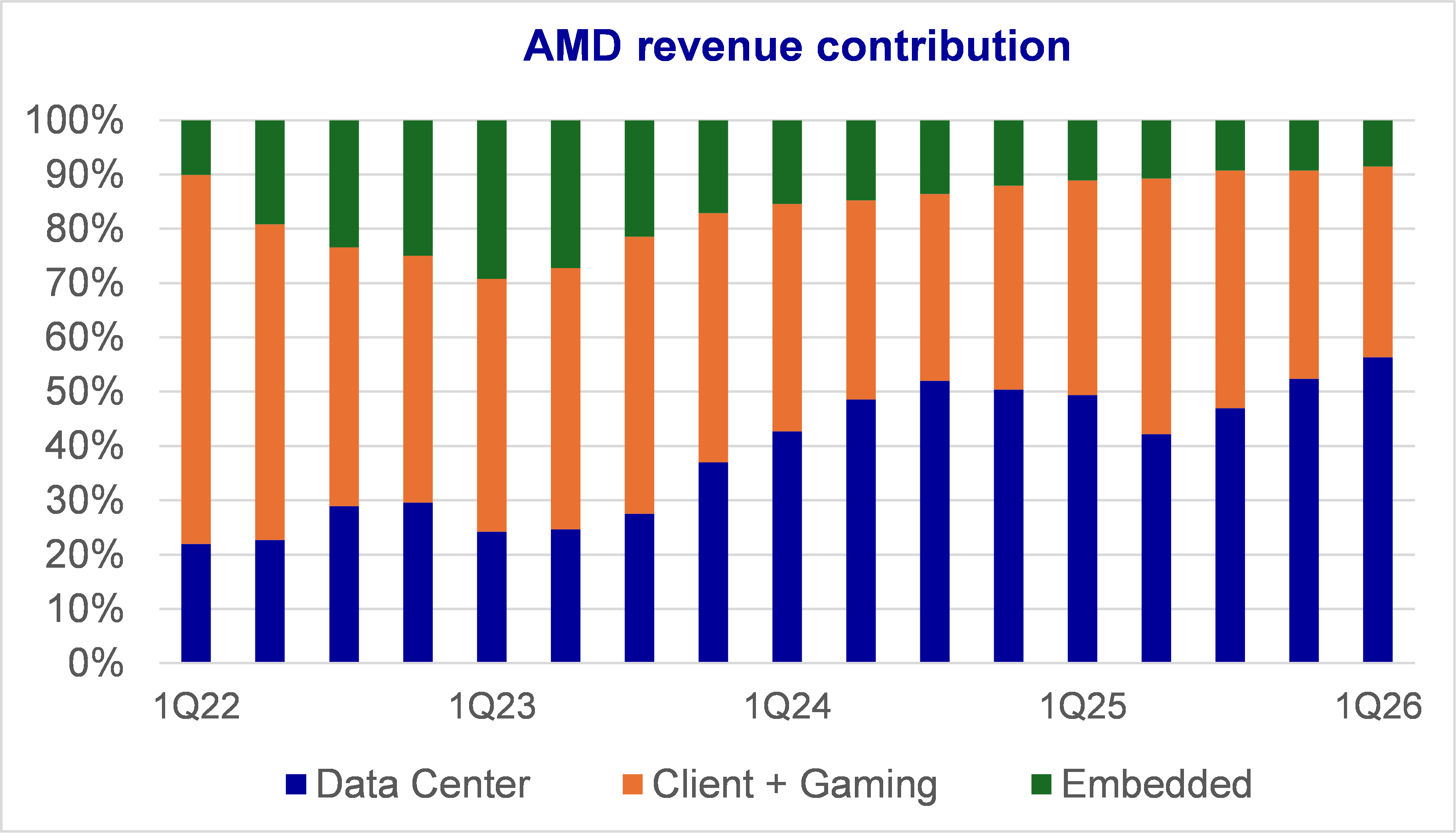

Given the stagnant state of the PC market, this means that AMD is a Data Center company from 2026 (ie majority of revenues from Data Center).

AMD believes it is on a path to exceed 50% market share in Server CPUs

6th-gen EPYC “Venice” (Zen 6, 2nm): on track to launch later in 2026. Includes “Verano,” AMD’s first EPYC CPU purpose-built for AI infrastructure.

AMD claims that “Venice” (Zen 6) delivers 2x+ more throughput per socket vs. leading ARM-based AI solutions.

CEO Su expressed confidence in delivering tens of billions in annual data center AI revenue by 2027.

Unfortunately, this number does not help us as it adds CPU and GPU together. It would be nice to have a GPU revenue indication.

However, Consensus probably has $25-30bn in Data Center revenues in ’26. If the AI component alone is 10s of bn, add non-AI and Enterprise: Consensus could be too low by 10bn.

GPU: no new information – because it’s a 2027 story

“We talked about our large partnerships with OpenAI and Meta “ “our expanded strategic partnership with Meta to deploy up to 6 gigawatts of AMD Instinct GPUs spanning several product generations”

“a growing number of new customers engaging on large-scale deployments, including additional multi-gigawatt opportunities”

forecasts are coming in with all of our customers, we’re actually seeing it above our initial plans that we had planned for 2027. a breadth of customers interested in deploying at significant scale MI450 series for both training and inference workloads, although the largest deployments are for inference”

based on all of that and the scale of new customer interest, we see a path to really get to exceed our original targets of greater than 80% CAGR. And these are really 2027 time frame”

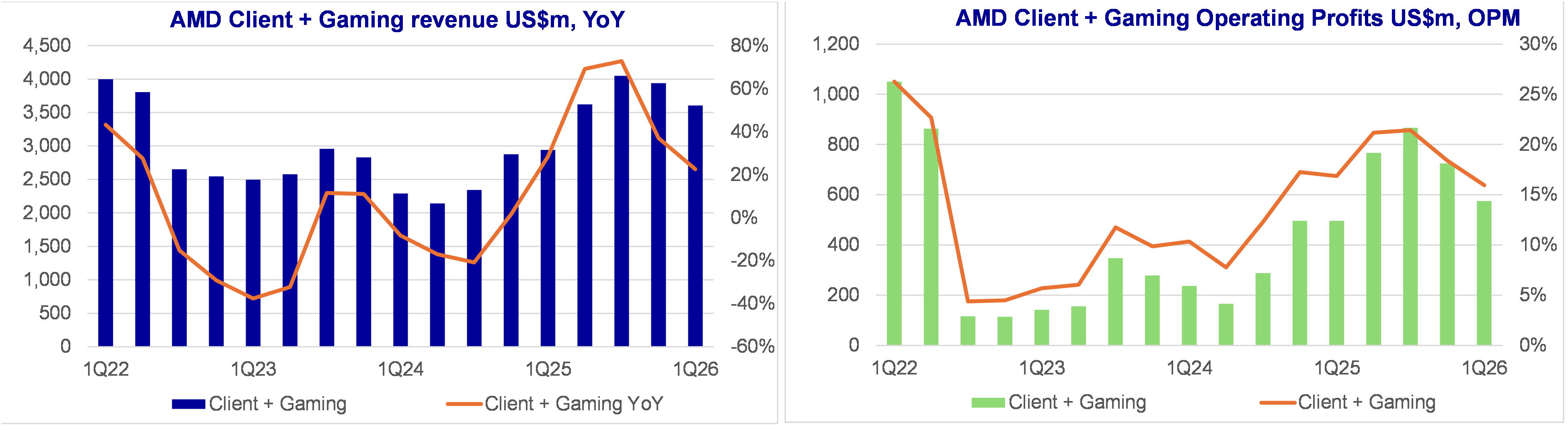

Client and Gaming

Management said that Gaming revenues will decline due to component cost inflation (ie Memory). Less Gaming leads to declining margins (chart below)

Nothing much to say about PC + Gaming, it doesn’t matter either way. No positive driver coming in 2026-27 (ie the problem of cost inflation and declining volumes). Not negative enough to mitigate Data center growth.

Below the paywall:

1Q25: a 7% beat versus Consensus

2Q25: guidance net income 13% above Consensus

Why Consensus will go up 15-20%

Valuations